Policymakers often look to the health of household balance sheets as a marker of individuals’ ability to navigate an environment of growing economic uncertainty and rising prices. Some households were able to bolster their savings recently due to the combination of declines in spending during the height of the pandemic, direct stimulus payments to households and rapid improvements in labor market conditions as the economy recovered. Personal savings by American households more than doubled in 2020 and remained elevated throughout most of 2021. Another component of household balance sheets – household debt – measures financial obligations households maintain as economic conditions change. As a result, the current composition of household debt can be an indicator of future spending behavior and how consumers will respond to future shocks. In this edition of the Rocky Mountain Economist, we show that growth in mortgage debt accelerated recently in Colorado, New Mexico and Wyoming, yet the relative costs to households of paying these debts fell. Consequently, delinquencies are at a historic low, and mortgages continue to account for a relatively small share of delinquent debt. Households with lower credit scores are also showing a relatively low incidence of past-due payments compared with historical norms.

Although households began 2022 with healthy debt conditions, more households are reporting difficulties meeting their current expenses amid rising food and energy prices. Consumers have begun to shift their spending habits in recent months by pulling back on purchases of large-ticket items or switching to lower-cost options when available. So far, most households have been able to meet their debt obligations. But the slight pickup in past-due payments for credit card balances and auto loans will be crucial to monitor over coming months.

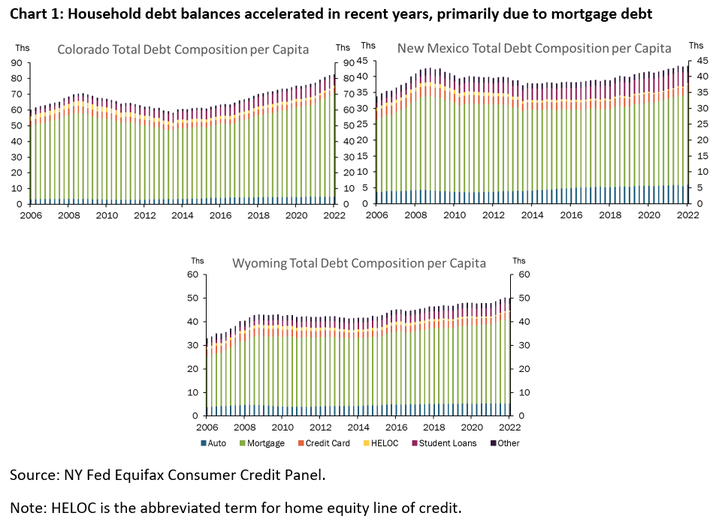

Debt Balances Continued to Rise in Recent Years

Overall debt balances among households in the Rocky Mountain region grew faster over the past two years compared with previous trends, primarily because of growth in mortgage debt. Chart 1 shows total debt per capita for Colorado, New Mexico and Wyoming households using data from the Federal Reserve Bank of New York Consumer Credit Panel/Equifax – data, which are from a nationally representative anonymous random sample from Equifax credit files.i Colorado showed a larger increase in total debt balances, nearly 10% between 2020 and 2022, but debt growth in New Mexico and Wyoming also picked up to nearly 4% over the same period. Most of the increase in total debt balances is attributed to the rise in mortgage debt over that period (green bars). Mortgage debt per capita increased 15.6%, 10.7% and 7.9%, respectively, relative to the first quarter of 2020 for Colorado, New Mexico and Wyoming, respectively. This growth in mortgage debt more than offset the modest declines in other categories such as credit card and home equity lines of credit. During the low-rate environments in 2020 and 2021, the demand for homes increased and homebuyers were able to take on more debt. The combination of high demand and low inventory accelerated home price growth. Also, new entrants into housing markets, due to in-migration from coastal cities, further put upward pressure on regional home prices and increased total mortgage debt overall.

Mortgage balances grew faster than other categories of household debt, but auto debt also increased over the last two years. Auto loans grew in Colorado and New Mexico by 4.5% and 4.8%, respectively, in the first quarter of 2021 compared with a year prior. Growth in auto-loan balances peaked during the second quarter of 2021 and has moderated in recent months as car sales diminished. Conversely, credit card debt declined significantly in 2020, an indication of households’ pullback in spending during that period. On average, credit card balances declined 11% in 2020 throughout the region. However, the ongoing purchases of goods and recovery in demand for travel, leisure and dining since the end of 2021 led to a resurgence in credit card debt balances across the region.

Debt Payments Remain Relatively Low Share of Household Income

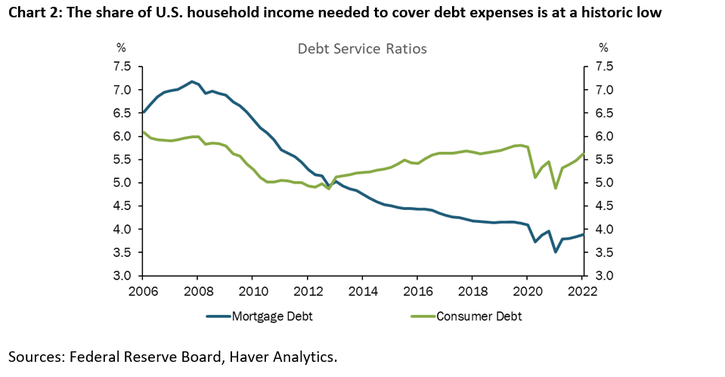

Although debt levels grew in the Rocky Mountain region over the past two years, several indicators point to a lower debt burden. Household debt service ratios, which measure the ratio of debt-service payments relative to household disposable income, remain below 2019 levels, as shown in Chart 2. Moreover, the costs of mortgage debt payments across the U.S. are at historically low levels compared with household income, on average being just below 4% of disposable income. One factor keeping debt-service ratios low, especially for mortgages, is the low interest rate environment of recent years. Mortgage rates reached historic lows. Also, tightening labor market conditions over the past two years led to wage growth. Augmented with economic stimulus payments, household disposable income expanded, reducing the share that was needed to be reserved for debt payments.

In addition to facing lower debt payment obligations at the start of 2022, a record number of households reported they could cover an emergency expense without having to borrow. According to the Federal Reserve’s Survey of Household Economics and Decision Making, in 2021 more than two-thirds of households could cover an unexpected $400 expense using cash or equivalent sources of funding.

Delinquency Rates Remain Subdued for Most Households

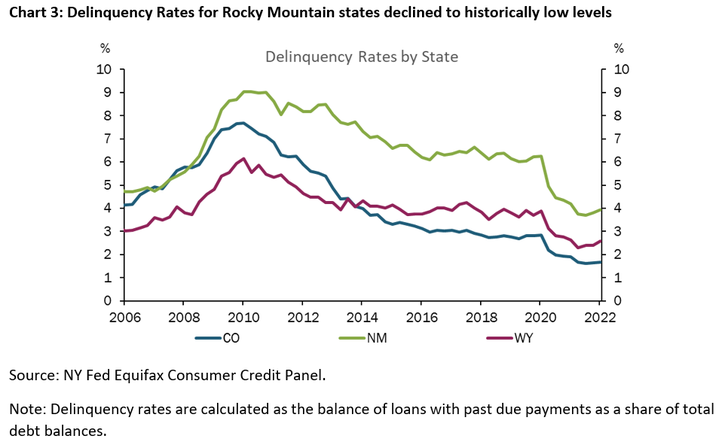

Diminished debt burdens for households reduced delinquency rates in the Rocky Mountain region to historic lows. Chart 3 shows the percentage of total debt balances that are past due for the three Rocky Mountain states. Delinquency rates for Colorado, New Mexico and Wyoming are now 1.6%, 3.9% and 2.9%, respectively. Current delinquency rates are a stark contrast to the 2007-09 recession, where elevated delinquency rates reflected the severe financial distress experienced by many households during that period. While delinquency rates remain subdued, there have been slight pickups in rates for New Mexico and Wyoming, particularly for debt that is less than 90 days past due.

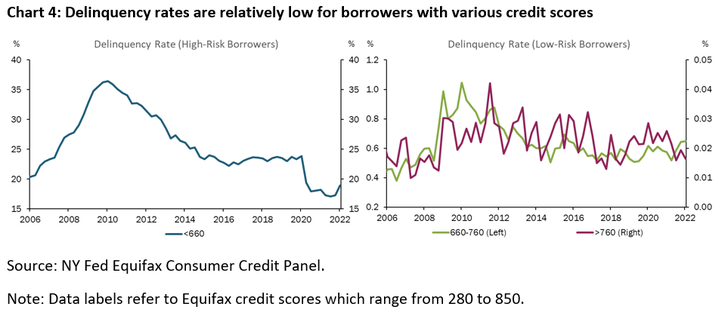

Delinquency rates are low across borrowers regardless of their credit history. Chart 4 shows delinquency rates aggregated across the Rocky Mountain region for three Equifax credit score categories. Borrowers with the highest risk of transitioning into delinquency, i.e., individuals with a credit score below 660, exhibited the most notable improvement in delinquency rates over the past two years. Delinquency rates for this category reached a low of 17% in 2021 (left panel). However, there has been a slight increase in recent months, a development that bears monitoring. Borrowers with stronger credit histories also managed to stay current on their debts over this period. Individuals with credit scores above 660 saw relatively no movement in their delinquency rates over the past two years and are showing little sign of any increase.

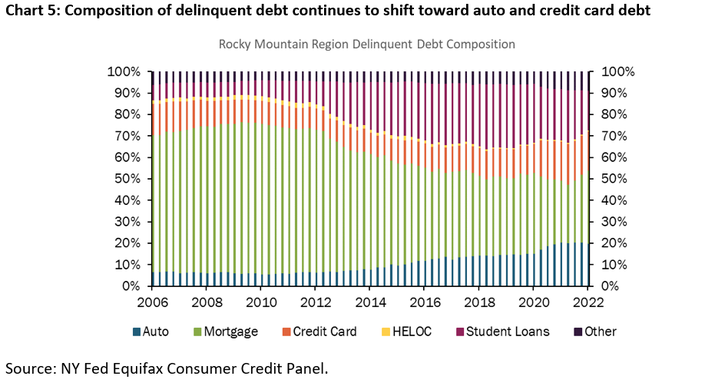

While delinquency rates declined overall, changes in delinquency rates were not uniform across different loan types. In the Rocky Mountain states, the composition of delinquent debt has shifted over time. Mortgage debt has become an increasingly smaller share of delinquent debt, while credit card, auto and student loan debt have each grown in share. This pattern changed slightly over the last two years, as seen in Chart 5. Due to federal student loan moratoriums, the share of delinquent debt attributed to student loans declined. However, auto loans and credit cards increased their share of delinquent debt, which furthered the pre-existing decline in the share of delinquent mortgage debt.

Mortgages tend to have delinquency rates below other categories of debt and have declined in their share of delinquent debt over the past decade. The decline in late payments of mortgages accelerated further over the last two years. Delinquency rates for credit card debt exhibited starkly different trends in recent years. The proportion of delinquent credit card debt increased through the end of 2020 and then decreased, starting in 2021. The timing of the increase in credit card delinquency corresponds with a period of financial distress for some households who suffered employment and earnings losses at the height of the pandemic. In 2021, when businesses began to reopen and rehire workers, the credit card delinquency rate declined, and is currently in line with historic levels.

Looking Ahead

The information above describes household debt conditions through the first quarter of 2022. Since then, price pressures have grown rapidly. Moreover, food and energy have led the rise in prices. Purchases of gasoline tend to be inelastic, changing little as prices rise. And rising grocery prices tend to affect households quickly, especially for perishable items. In other words, consumers may find some difficulty in substituting away from these expenses and must bear the burden of higher prices.

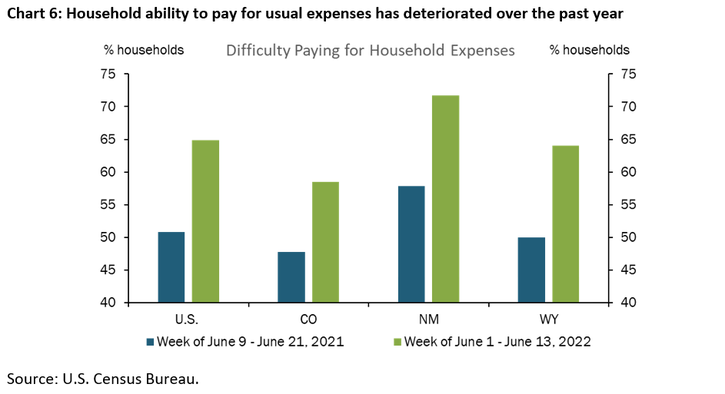

Even though wages and employment continued to grow over the past year, the share of households in Colorado, New Mexico and Wyoming reporting difficulties in meeting their expenses in June was higher than a year ago. Chart 6 shows that the share of households facing difficulty paying for their usual household expenses has increased between 10 and 15 percentage points over the last year for Colorado, New Mexico and Wyoming, respectively. Inflationary pressures continue to erode the purchasing power of households and may jeopardize their ability to pay off debt moving forward.

_________________________

i External Linkhttps://www.newyorkfed.org/research/staff_reports/sr479.html

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nicholas Sly

Vice President, Economist, and Denver Branch Executive