Despite a prolonged slump in the price of many agricultural commodities globally, long-term economic prospects in the agricultural sector often have been viewed as positive. Optimism about agriculture’s long-term future and growth is based on expectations of steady growth in global populations and incomes. However, agricultural production in recent years has increased significantly, even as commodity prices have remained suppressed, costs have remained elevated and profit opportunities have remained limited or fleeting. Across the world, agricultural producers and businesses have sought to adapt to the prolonged downturn in agricultural prices, while at the same time position themselves for longer-term opportunities that might warrant further investment.

The 2019 Agricultural Symposium, titled “Exploring Agriculture’s Path to the Long Term,” was July 16-17 at the Federal Reserve Bank of Kansas City. Participants discussed the linkage between current conditions in agricultural markets and longer-term prospects. On the first day, speakers highlighted factors that are driving or constraining growth in agriculture’s current economic environment and how those factors may differ from the long term. On the second day, speakers discussed how the agricultural sector might transition toward a more profitable long-term future and the threats and opportunities that might emerge.

Near-Term Developments

The agricultural sector has remained in a prolonged slump as prices and profits have continued to limit the potential for growth. In 2019, U.S. farm income is expected

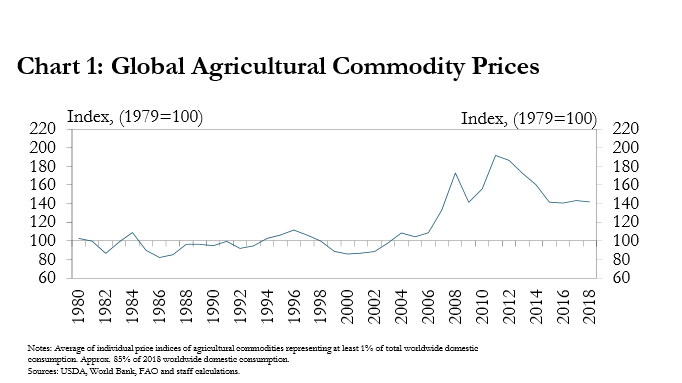

to remain about 44 percent less than in 2013 as agricultural commodity prices have remained relatively low. Despite a recent increase in the price of corn, global agricultural commodity prices have, on average, remained flat for the past four years (Chart 1).

Financial stress has continued to build for many U.S. agricultural producers, and while conditions may not mirror those of the 1980s, the effect on younger producers may be similar. U.S. farm income dropped 48 percent between 1979 and 1983, similar to the decline of recent years. Unlike the 1980s, the recent downturn has not led to a sharp increase in farm bankruptcies. However, Stephanie Liska of Beck Ag Inc. noted that current conditions are causing many younger producers to experience a crisis just as real as that of the 1980s.

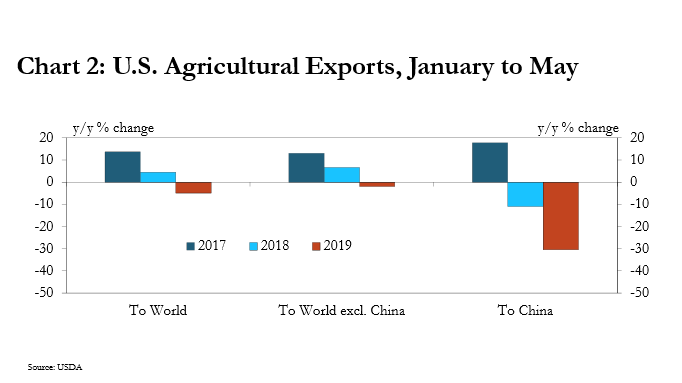

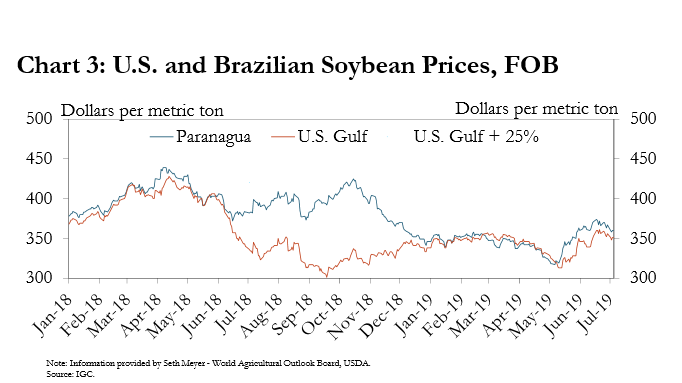

In the near term, uncertainties connected to trade, U.S. production and African swine fever (ASF) are likely to be significant drivers of agricultural commodity prices and profits. U.S. agricultural exports have weakened considerably alongside ongoing trade disputes with China (Chart 2). Although the trade disputes have adversely affected agriculture in the United States, farmers in South America saw that foreign buyers were willing to pay a premium for their product in 2018, according to Seth Meyer, formerly of the USDA’s World Agricultural Outlook Board (Chart 3). Though this gap has narrowed in recent months, the trade disputes remained unresolved through July 2019.

Many symposium participants recognized the potential impact associated with ASF in China. According to recent reports from the Chinese Ministry of Agriculture, over 1 million pigs have been culled since August 2018 because of ASF. Industry experts estimate that Chinese pork production may decline as much as 25 to 35 percent in 2019.__ Although the reduced supply of pork in China is likely to benefit producers unaffected by the epidemic, it also is likely that the reduction in pig herds has limited China’s need for feed imports, particularly soybeans used to produce soybean meal.

Long-Term Economic Factors

In the previous decade, two factors often are cited as the most significant drivers of demand for agricultural products: growth in U.S. biofuels and strong economic growth in China. Several symposium speakers recognized that there does not appear to be an obvious long-term driver of demand that might provide a significant boost to agricultural commodity prices and farm sector profitability.

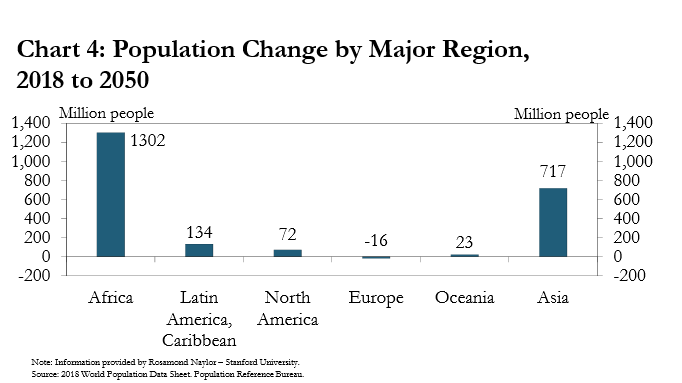

Although growth in global populations and income is expected to continue in coming years—and broadly support demand for agricultural products—much of the increase in population is expected to occur in Africa. Rosamond Naylor of Stanford University said that by 2050, Africa’s population is expected to grow by 1.3 billion, dwarfing the expected increases in most regions other than parts of Asia (Chart 4). While this population increase may contribute to increased demand for agricultural products, it is not clear whether a larger population in Africa will generate the same kind of increase in demand that occurred in the past decade in China.

Ongoing investments elsewhere in the world also are likely to increase production of agricultural commodities, which could weigh more heavily on agricultural prices and profits. Marcelo Duarte Monteiro, formerly of the Mato Grosso (Brazil) Department of Transportation and Logistics, noted that the infamous BR-163—a key agricultural highway—eventually will be fully paved. This improvement is expected to reduce the cost of transporting corn and soybeans grown in Mato Grosso to the large port in Santos, easing access to global markets. Currently, the cost of producing these commodities in Mato Grosso is substantially cheaper than in the Midwest region of the United States, but costs associated with transportation have limited the competitiveness of the Brazilian products. Ray G. Young of Archer Daniels Midland Co., also noted that investments in infrastructure will be a critical component underlying competitiveness in global agricultural markets in the years to come.

Transitioning to the Long Term

The transition to a more economically profitable long-term future for U.S. agricultural producers will require a more business-oriented approach. At the same time, the transition for emerging agricultural production regions such as South America and sub-Saharan Africa will be dependent on the development of infrastructure, research and development connected to production and an overarching supportive policy framework that includes the establishment of key trading partnerships.

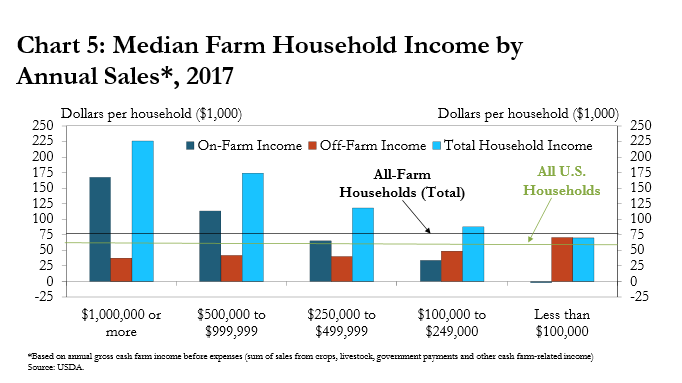

According to Michael Gunderson of Purdue University, two strategies that producers are likely to focus on are improving efficiencies by cutting costs or seeking to differentiate their products. As profit opportunities have remained limited in recent years, many agricultural producers have needed to re-evaluate their long-term strategies. The strategy of improving efficiencies by cutting costs most likely is relevant for large producers that can spread costs over a large number of acres. According to the USDA, farm income has been largest for farm households that have taken advantage of economies of scale and grown their operations most substantially (Chart 5). For smaller operations, a focus on product differentiation and the ability to remain nimble in response to changing consumer demands may be a more viable business strategy.

Improving efficiencies by cutting costs also will be an important pursuit for agricultural producers in developing countries, but much of the success in reducing production costs in these regions may depend on government initiatives. Speakers acknowledged a significant potential for increased agricultural production in regions such as Brazil, Argentina, India and parts of sub-Saharan Africa due to favorable soil and weather conditions. However, there is considerable variation in the extent to which these regions have advanced the competitiveness of the agricultural sector through infrastructure investments, research and development, and sound governance. In India, for example, management of water resources is inefficient, with few incentives for producers to restrict their high levels of usage. In Brazil, transportation delays lead to significant product loss between the farm gate and the port. And in large parts of sub-Saharan Africa, intermittent access to reliable electricity presents significant challenges to improving the competitiveness of agricultural producers on the global market.

In addition to the broad identification of an overarching business strategy such as reduced costs, other factors are reshaping how producers operate their farm business. The increasing usage of digital technologies, along with changing demographics of producers, is redefining what it means to be a farmer. Liska pointed out that the U.S. farmer no longer simply is tending to the land and livestock, but also has skills and knowledge of all areas of business. This emerging generation of producers is looking for all-encompassing business solutions and not just product information that might be useful for production. Similarly, Rory O’Sullivan of Grain Discovery described how using blockchain can help push future technology investment away from a focus of increasing yield and production toward improving supply chain efficiencies, product traceability and overall profitability.

Long-Term Uncertainties

Broad increases in demand for agricultural products and productivity gains made possible by technological advancements represent long-term opportunities in the agricultural sector. However, there also are significant elements of uncertainty that are likely to affect global agricultural prospects. Symposium speakers recognized that, over the next 30 years, uncertainties surrounding climate change, water availability, consumer demand and global trade will have a critical effect on the sector.

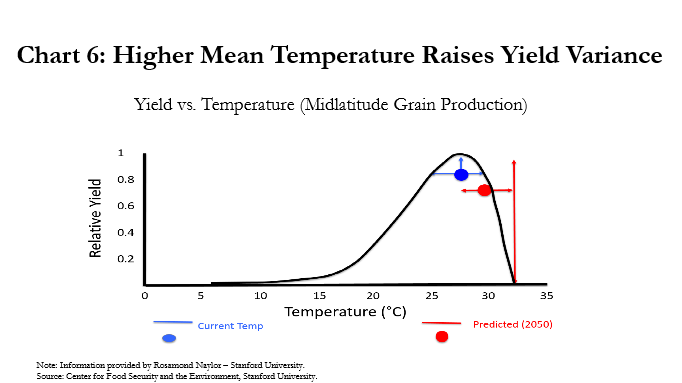

Climate change emerged as a primary source of concern and uncertainty for the long-term future of agriculture among symposium participants. Rising global temperatures over the long term largely will impact agriculture through greater weather variability, leading to increasing uncertainty about crop yields and production. As Naylor pointed out, grain yields are highly sensitive to extreme temperatures. If temperatures rise in the coming decades as currently predicted, the variability of grain production could increase substantially (Chart 6).

Potential shifts in the location and composition of cropping systems due to climate change represents another source of production uncertainty. A higher global frequency of extreme weather events may increase the probability of simultaneous supply shocks in multiple regions, potentially resulting in greater market volatility. Moreover, Naylor indicated that domestic policy aimed at stabilizing prices in the event of greater global market volatility could have the potential to create trade barriers and lead to further market destabilization.

Naylor added that ground and surface water vital for many major areas of agricultural production, particularly India and the U.S. Great Plains, are at risk of depletion and conditions could be further exacerbated by climate change. The primary uncertainties related to water availability surround how depletion in one area of the world such as India would impact global agricultural markets and agricultural production elsewhere in the world.

Changes in consumer preferences for food represent a significant source of uncertainty in demand for agricultural products and likely will affect long-term prospects for agricultural producers. Jane Andrews, formerly of Wegman Food Markets, provided insights on how the retail food industry is adapting to growing preferences for food purchases tied to nutrition. Product traceability also is likely to become an increasing focus as consumers seek more information about the fundamental composition of food products. These developments may create significant opportunities within the agricultural sector for agricultural operations that seek to adapt and create strategic partnerships across the supply chain. However, many aspects of consumer preferences in future centers of population growth such as Africa remain uncertain, which prompted discussion about the importance of creating supply chain efficiencies and establishing trade partnerships that are easily adaptable to shifting demands.

Many participants also raised concerns about the potential for current U.S. trade disputes to have lasting implications. The disruption of U.S. soybean exports to China has created incentives for China to establish new trading partnerships. Daniel Basse of AgResources Co. noted that rearrangements in world trade patterns can take years to reverse, highlighting the uncertainty about how long those effects may linger. As Young suggested, China is becoming less reliant on U.S. agriculture, and the United States may benefit from becoming less reliant on Chinese demand.

Conclusion

For much of this century, long-term prospects in agricultural markets have been resoundingly positive. A significant portion of this optimism stemmed from the extraordinary growth of developing economies, such as China, in addition to the emergence of biofuel policy that stimulated demand for agricultural products. Participants at the 2019 symposium generally recognized that there still are reasons to be optimistic about the long-term potential in agriculture due to growth in global populations and income, but also acknowledged that the sector faces a number of headwinds that will challenge its future path.

As the agricultural sector seeks to position itself for long-term sustainability and growth, it must contend with a variety of economic and policy uncertainties. Ongoing concerns about the future of global trade have clouded the horizon for a sector that has grown to rely heavily on global supply chains. The industry must also seek to adapt to changes in consumer preferences, which may require different production practices or process enhancements. The future potential for agricultural production also is subject to a significant amount of uncertainty related to climate change, water availability and government policies.

In the past, the agricultural sector has proved to be both resilient and innovative. As the sector transitions from a prolonged low-price environment of recent years, it will need to be so once again alongside numerous uncertainties and potential structural changes to ensure a clear path toward long-term growth.

Endnotes

-

1 Source: FAO – United Nations and Ministry of Agriculture of the People’s Republic of China.

-

2 Source: RaboResearch. “Rising African Swine Fever Losses to Lift All Protein.” April 2019. https://research.rabobank.com/far/en/sectors/animal-protein/rising-african-swine-fever-losses-to-lift-all-protein.html

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.