Energy policies that promote shifts toward renewable fuels have important implications for the agricultural sector. Policies in the Inflation Reduction Act (IRA) in particular are likely to increase connections between the U.S. row crop sector and the energy industry. The IRA, which Congress passed in August 2022, created policies to help further transition the U.S. economy away from hydrocarbons and toward more domestic renewable fuel production. Previous shifts in renewable fuel policy, such as the implementation of the Renewal Fuel Standard (RFS) in 2006, may help shed light on the IRA’s potential effects. For example, prices for corn became more correlated with energy prices after the RFS due in part to a dramatic shift in demand for corn as an energy input.

Cortney Cowley examines the RFS as a case study for the potential effects of policy-led renewable energy transitions such as the IRA. She finds that following the implementation of the RFS, the broader transition in the U.S. economy from conventional motor fuels to more renewable biofuels increased demand for and production of corn in the U.S. agricultural industry and likely contributed to higher but more volatile prices for crop producers. Outcomes from the RFS suggest that increased linkages between the crop and energy sector may boost farm income on balance but lead to more income variation and uncertainty for crop producers.

Introduction

Energy policies that promote shifts toward renewable fuels have important implications for the agricultural sector. Previous renewable fuel policies have spurred greater ethanol production, and more recent policies could similarly promote production of biodiesel, renewable diesel, and plant-based aviation fuel in the United States—prompting, in turn, shifts in the agricultural production of crops used as feedstock. Soybeans are a particularly important input in biofuels, and increased demand for and production of ethanol has already increased demand for corn.

In particular, policies in the Inflation Reduction Act (IRA) are likely to increase connections between the U.S. row crop sector and the energy industry. The IRA, which Congress passed in August 2022, created policies such as the Section 45Z Clean Fuel Production Credit to help further transition the U.S. economy away from hydrocarbons and toward more domestic renewable fuel production. Closer connections between the energy and agriculture sectors could increase demand and thus raise prices for major row cops. However, closer connections between the two sectors could also make crop prices and farm income more vulnerable to wide swings in energy prices, creating greater uncertainty for farm borrowers and agricultural lenders.

Previous shifts in renewable fuel policy may help shed light on the IRA’s potential effects. Following the implementation of the Renewable Fuel Standard (RFS) in 2006, prices for corn became more correlated with energy prices due in part to a dramatic shift in demand for corn as an energy input. In particular, the percentage of corn used for industrial purposes (including ethanol production) grew from less than 30 percent of total domestic corn consumption in 2000 to almost 60 percent by 2010.

In this article, I examine the RFS as a case study for the potential effects of policy-led renewable energy transitions such as the IRA. I find that following the implementation of the RFS, the broader transition in the U.S. economy from conventional motor fuels to more renewable biofuels increased demand for and production of corn in the U.S. agricultural industry and likely contributed to higher but more volatile prices for crop producers. Outcomes from the RFS suggest that increased linkages between the crop and energy sector may boost farm income on balance but lead to more income variation and uncertainty for crop producers.

Section I reviews historical connections between agriculture and energy industries and describes how the RFS contributed to changes in corn markets. Section II discusses more recent developments in the energy sector, including the IRA, and the potential future implications of further transitions toward renewable biofuels on major U.S. row crops—in particular, soybeans.

I. The Renewable Fuel Standard Spurs a U.S. Corn Renaissance

Historically, connections between the energy and agricultural sectors emerged due to energy’s use as an input for agricultural production—for example, from the diesel, gasoline, electricity, or natural gas used to dry grain, fuel trucks and tractors, and provide climate control for barns and houses. In addition to these direct inputs, other inputs into agricultural production are derived from energy products. Nitrogen fertilizer, for example, is derived from natural gas.

Although energy inputs account for an important share of production expenses in the agricultural sector, this share has declined in recent decades. In the early twentieth century, direct energy inputs accounted for almost 15 percent of total production expenses. Over time, however, energy-use efficiency in agricultural sectors has increased. In 2023, energy accounted for about 5 percent of production expenses in the agricultural sector.

Although energy’s overall share of input costs for U.S. farms has declined over time, fertilizer expenses have continued to increase. Chart 1 shows that while costs for fuel, lube, and electricity (purple line) have been relatively stable in recent years, fertilizer expenses per acre (light blue line) more than doubled from 2020 to 2022, following dramatic increases in natural gas prices (green line). As the cost of fertilizer has moved higher, its share of production costs has also moved up, from 4 percent nearly a century ago to about 7 to 9 percent by 2022.

Chart 1: Energy-Related Inputs for Corn, 1996–2022

Source: U.S. Department of Agriculture (USDA).

In addition to these inputs, connections between the agricultural and energy sectors have emerged more recently due to the growing role of energy as an agricultural output. Corn, for example, is a key input in ethanol, which has become a much more important biofuel since the implementation of the Renewable Fuel Standard (RFS) in 2006._ The RFS specifies volumetric mandates, called renewable volume obligations (RVOs), for renewable fuels to replace or reduce the quantity of petroleum-based transportation fuel, heating oil, or jet fuel. The RFS has three primary policy goals: enhancing energy security through additional domestic production of biofuels, expanding the development and production of renewable transportation fuels such as ethanol, and supporting rural economies by expanding demand for agricultural products, particularly corn.

Around the same time as the implementation of the RFS, California implemented additional policies that boosted demand for biofuels, with several other states following close behind. The Low Carbon Fuel Standard (LCFS) legislation in California and other states introduced policies to reduce carbon emissions, decrease petroleum dependence in the transportation sector, and encourage the use and production of cleaner low-carbon transportation fuels.

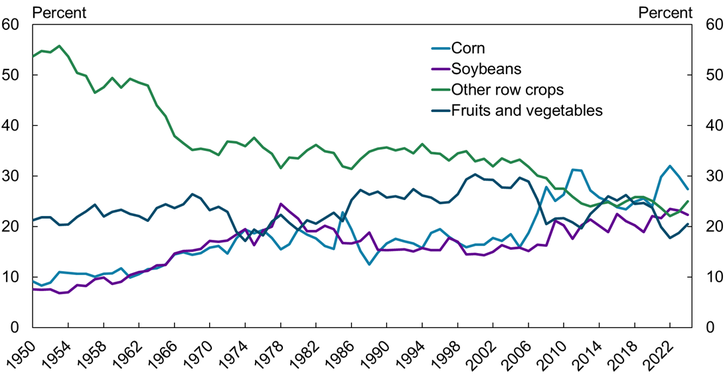

Together, the RFS and other renewable fuel policies led to a dramatic shift in demand for corn. Domestic demand for corn arises from four main sources: its use in animal feed, food for human consumption, seed, and ethanol. Chart 2 shows the evolving share devoted to the major sources of demand for corn (due to data limitations, ethanol, food, and seed are combined into “industrial use”). Prior to the RFS, as much as 55 percent of the corn produced in the United States was used to feed animals, while 20 percent was used in the industrial production of food, seed, ethanol, and other products. However, since the implementation of the RFS, industrial use has expanded, accounting for over 40 percent of U.S. corn in 2023. This expansion has led overall demand for corn to increase despite a decline in the share of corn used as an input in animal feed.

Chart 2: Redistribution of U.S. Corn Demand

Note: Alongside domestic uses shown in the chart, international exports typically account for about 11 to 17 percent of U.S. corn demand, with the remaining corn carried over to the next year (ending stocks).

Source: USDA.

In response to increased demand for corn, farmers increased acreage devoted to growing it. Chart 3 shows that acres planted in corn grew sharply from 2006 to 2007. In the 1990s and early 2000s, farmers in the United States typically harvested around 78 million acres of corn a year. Since 2006, U.S. farmers have harvested closer to 91 million acres each year. This increased acreage devoted to corn production was likely accomplished both by converting land to agricultural use and by switching agricultural land to corn from other crops.

Chart 3: Expansions in U.S. Area Planted in Corn

Source: USDA.

Prior to the RFS, corn accounted for about 18 percent of total U.S. crop acres. Since the RFS, corn has accounted for about 23 percent of total cropland. In the process, the geographic scope of corn planting has also spread out. Panel A of Map 1 shows that prior to the RFS, corn production was fairly concentrated in the upper Midwest, in an area typically referred to as the Corn Belt. Panel B shows that as of 2017 (the most recent year for which data are available), corn acreage has expanded in every direction.

Map 1: Geographic Expansions of U.S. Area Planted in Corn from 2002 to 2017

Panel A: Corn Acreage in 2002

Panel B: Corn Acreage in 2017

Crop prices have also become higher and more volatile since the RFS. Chart 4 shows that since the implementation of the RFS, prices for corn have been, on average, about 25 percent higher than average prices from 1990 to 2005. The variation in crop prices has also increased considerably (excepting a short period of volatility in the mid-1990s). From 1990 to 2005, the average negative deviation from the mean price was −14 percent, and the average positive deviation was 19 percent. From 2006 to 2023, both negative and positive deviations jumped to −23 percent and 40 percent, respectively. Outside of severe weather shocks, the quantity of a commodity produced is typically stable and predictable. Therefore, volatility in a producer’s revenues tends to stem from volatility in prices. Larger variations in prices can create more uncertainty for farmers, make financial planning more difficult, and increase the necessity for risk management and financing.

Chart 4: U.S. Corn Prices, 1990–2023

Note: Deviations from mean are calculated by taking the difference between the daily price of corn and the average price for the time period shown, dividing the difference by the average price, and multiplying by 100.

Sources: Wall Street Journal (Haver Analytics), Bloomberg, and author’s calculations.

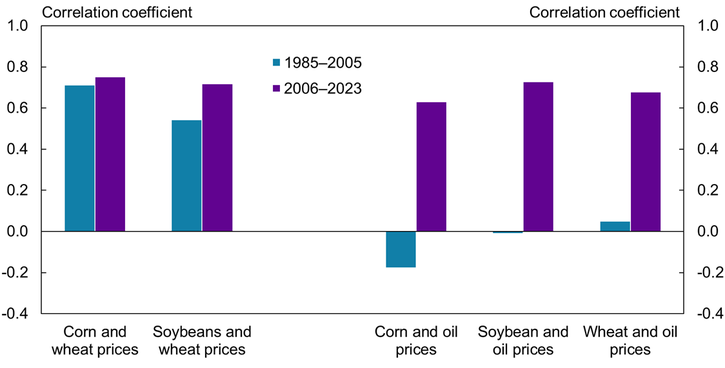

One reason crop prices have become more volatile is that prices for corn and other row crops have become more highly correlated with energy prices. Prior to the implementation of the RFS, energy prices had been nearly two times as variable as crop prices. Chart 5 shows that prices for corn, wheat, and soybeans have been historically correlated with each other, both before and after the RFS. In contrast, prices of corn and oil were not correlated until after the RFS. For example, the correlation coefficient between corn and oil prices grew from −0.18 from 1985 to 2005 to 0.63 from 2006 to 2023. In other words, since the RFS was enacted, a 1 percent change in oil prices has typically been associated with a 0.63 percent change in corn prices.

Wheat and soybean prices have also became more strongly and positively correlated with the price of oil. In fact, the correlation coefficients between oil and each row crop are now roughly similar to the correlation coefficients among the crops. Notably, the RFS increased energy use demand almost exclusively for corn. Therefore, the tightening correlation between oil prices and wheat and soybean prices likely reflects wheat and soybeans’ strong correlations with corn. Alongside the RFS, however, other factors have contributed to higher volatility and correlations in commodity markets. Common explanations include the increased financialization of commodities and low interest rates (Gruber and Vigfusson 2018).

Chart 5: Correlations between Prices for Oil and Agricultural Commodities

Sources: USDA, U.S. Energy Information Administration, and author’s calculations.

In summary, the transition from conventional energy to renewable energy prompted by the RFS and other renewable fuel policies spurred increased demand for biofuels, supported corn prices, and in turn boosted U.S. corn production. Consequently, corn prices have been higher but also more volatile, as they have become more closely tied to energy prices. Additional policies that boost biofuel demand could further support prices and make the correlation between energy and crop prices even stronger.

II. The Inflation Reduction Act and Implications for U.S. Soybeans

Similar to the RFS, the Inflation Reduction Act (IRA) and its emphasis on biodiesel and plant-based aviation fuel could again expand domestic demand for row crops. Unlike the RFS, however, the IRA is likely to boost demand not for corn but for soybeans. Although the IRA and RFS share goals of cutting carbon emissions and promoting the use of biofuels, they differ substantially in approach. Whereas the RFS imposed market requirements to push demand for renewable fuels—specifically, volumetric mandates for ethanol blended into gasoline—the IRA instead provides market incentives in the form of tax incentives, direct payments, and low-interest loans to promote increased production and use of biofuels for transportation. For example, the Clean Fuel Production Credit (Section 45Z) provides a tax credit for the domestic production of clean transportation fuels, including biodiesel and renewable diesel, to registered producers in the United States. In addition, the Sustainable Aviation Fuel Credit (Section 40B) provides a credit for each gallon of sustainable aviation fuel produced.

In particular, the IRA seeks to considerably boost the production of biodiesel, renewable diesel, and plant-based aviation fuel (also known as “sustainable aviation fuel” or SAF). Soybeans, which have an especially high oil content, can be used as an input in the production of all three. Biodiesel and renewable diesel are typically used in land- and sea-based commercial trucking and shipping as well as other industrial and agricultural uses. Although biodiesel and renewable diesel have similar uses, they differ in several ways, including how they are produced. Biodiesel is produced from vegetable oils and animal fats, while renewable diesel can be produced from nearly any biomass feedstock. In addition, renewable diesel can be used as a “drop-in” fuel for petroleum-based diesel (EIA 2024). According to data from the U.S. Energy Information Administration (EIA), renewable diesel and biodiesel are the second and third most consumed biofuels, respectively, after ethanol. In contrast, plant-based aviation fuel, which is used in place of traditional jet fuel for airline transportation, is less common. Currently, plant-based aviation fuel accounts for less than 1 percent of total aviation fuel use.

Any expansion of biodiesel, renewable diesel, and plant-based aviation fuel production in the United States will require a ramp-up in the production of oilseed crops used to make vegetable oil, especially soybeans. Currently, soybean production accounts for about 11 percent of U.S. farm revenues, and all other oilseeds combined, including canola, sunflower seeds, and flaxseed, make up only about 0.6 percent of farm revenues. Soybeans and other oilseeds are typically processed into two products: meal, which is used exclusively in the production of animal feed, and vegetable oil, which is used both in food production and in the production of U.S. biodiesel and plant-based aviation fuel.

Like the RFS, the IRA could spur a rapid redistribution in demand for row crops (here, soybeans). In particular, the IRA could increase domestic demand for soybean oil. The green line in Chart 6 shows that in the early 2000s, very little, if any, soybean oil was used for industrial biofuels. Instead, as much as 98 percent of the soybean oil produced in the United States was used in food for human consumption. However, industrial use of soybean oil has steadily increased since the early 2000s, largely due to a rise in biofuels. Following the implementation of the RFS, biodiesel production began to expand in the United States, though not as dramatically as ethanol. According to the EIA, biodiesel production grew from 0.009 billion gallons in 2001 to 2.65 billion gallons in 2021. Production of renewable diesel started in 2011, with production of other biofuels, including plant-based aviation fuel beginning in 2014. Production of biodiesel and renewable diesel combined has grown exponentially leading up to and since the passing of the IRA, reaching more than 4 billion gallons by 2023. The use of soybean oil in industrial production has grown concurrently. By 2023, almost 50 percent of soybean oil was used for the industrial production of biofuels, while the remaining half was used for food production.

Chart 6: Growing Domestic Demand for Soybeans

Sources: USDA and author’s calculations.

As demand for industrial biofuels increases, the share of soybeans consumed domestically could also increase. The blue line in Chart 6 shows that the share of U.S. soybean production consumed domestically fell throughout previous decades. For most of the 2000s and 2010s, only 50 percent of the soybeans produced in the United States were consumed there, partly due to a ramp-up in soybeans produced for export to other countries (purple line) (Cowley 2020). However, since 2021, domestic consumption of soybeans has displaced exports, likely due, in part, to greater industrial demand. In 2023, domestic consumption of soybeans was almost 60 percent of production, the second-highest share in more than 15 years._

As the production of renewable transportation fuel expands, U.S. domestic consumption of soybeans will likely continue to displace international exports. The United States typically exports half of the soybeans it produces, with the largest share going to China (Cowley 2020). Indeed, recent articles have explored the United States losing market share of corn and soybean exports to Brazil (Hirtzer and Carey 2023, Veloso 2023). However, one key reason U.S. exports have declined is because they have been displaced by expanding domestic use of crops for the industrial production of renewable fuels. In other words, the decline in exports could reflect growing domestic demand rather than a lack of foreign demand for U.S. crops.

Supply constraints may lead domestic demand to continue to displace exports, as demand from biofuels seems likely to soon outstrip soybean production capacity in the United States. At the beginning of 2023, the total U.S. production capacity for biodiesel and renewable diesel was about 9 percent of average daily U.S. consumption of diesel fuel. More biodiesel and renewable diesel plants are either under construction or proposed for the future, so demand for soybeans from these domestic plants will likely increase. According to the EIA, the production capacity of 59 U.S. biodiesel plants was a cumulative 136,000 barrels per day (as of January 2023). Demand for soybeans from these plants alone could outstrip supply by the equivalent of 28 million acres of soybeans._ However, biodiesel is more costly to produce than petroleum-based and renewable diesel. Biodiesel also has a higher carbon intensity score and generates fewer renewable credits than renewable diesel. In fact, in early 2024, two major biodiesel plants closed indefinitely due in large part to a decline in prices for biodiesel that challenged profitability (Sanicola 2024).

Even so, higher demand for domestic biofuels may further tighten the correlation between crop prices and energy prices, increasing both the level and volatility of soybean prices. This correlation is especially likely to tighten over the next few years, reflecting historically low levels of U.S. soybean inventories at the end of 2023. In 2023, U.S. ending stocks for soybeans were 6 percent of total domestic use, down dramatically from 23 percent in 2018 amid a trade dispute with China. Tight inventories can make prices especially sensitive to increases in demand due to limited supply buffers. Pressure on U.S. soybean supplies could be compounded by limited suppliers of soybeans globally. Unlike crops such as corn and wheat, which are grown all over the world, soybeans are primarily grown in just three countries: the United States, Brazil, and Argentina.

Increased domestic biofuel production could also considerably increase demand for other oilseed crops such as canola and sunflower seeds, which are more efficient sources for producing biofuel. While soybeans yield about 50 gallons of oil per acre for biodiesel production, sunflower seeds produce about 82 gallons of oil per acre, and canola seeds yield about 95 gallons of oil per acre (Isom and Booker 2008). Despite their better yields, canola and sunflower—along with other oilseeds grown in the United States, such as flaxseed, cottonseed, mustard seed, rapeseed, and safflower—currently make up less than 2 percent of total farm revenues and less than 15 percent of all acreage planted in oilseed crops._

Although the production of other oilseeds has expanded slightly, soybeans remain the dominant oilseed crop. For example, the share of harvested crop acres that are other oilseeds (not soybeans) has inched toward 1.5 percent over the last few years, and the share of crop revenues for other oilseeds has slowly moved toward 2 percent. However, despite some growth in other oilseeds, soybeans still dominate. Chart 7 shows that in 2022, soybeans (purple line) became the second largest revenue-grossing crop behind corn (blue line). Despite a slight retraction in 2023, the overall growth of soybeans represents a major shift from 50 years ago, when the crop sector was much more diversified.

Chart 7: The Growing Prominence of U.S. Soybeans as a Share of Total Crop Revenues

Sources: USDA and author’s calculations.

Higher concentrations of revenues into individual crops could signal greater risks to individual farmers and the crop sector, as producers lose the protection that diversification provides against shocks to any particular product.

Conclusion

Renewable fuel policies have spurred growth in biofuels, positioned the energy industry as a key demand source for agriculture, and contributed to increased domestic consumption and production of corn and oilseeds. In particular, the RFS spurred demand for corn in the mid-2000s, and the recently enacted IRA is likely to spur similar demand for soybeans and other oilseed crops.

The implementation of the RFS may shed light on how the IRA will affect crop producers. I show that following the implementation of the RFS, prices for corn and other row crops increased and became more volatile and more highly correlated with energy prices. Price correlations and volatility could increase further with the implementation of the IRA, contributing to greater uncertainty surrounding revenues and income for farmers and agricultural lenders, even as higher prices are likely to increase incomes.

As a case study, the RFS suggests that developments in energy markets will continue to have important effects on agricultural credit conditions, particularly in areas concentrated in both agricultural and energy production. Previous research has shown significant effects on local agricultural economies due to ethanol infrastructure (see, for example, Anderson, Anderson, and Sawyer 2008; Katchova and Sant’Anna 2019; and Kropp and Peckham 2015). The expansion of biodiesel production could have similar effects. More broadly, although higher average prices could support stronger revenues, greater price volatility could lead to elevated risks for producers—particularly when production costs increase, such as in the post-pandemic period.

Endnotes

-

1 The RFS was one piece of legislation in two larger acts: the Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007.

-

2 Domestic consumption of soybeans was slightly higher in 2019 following a sharp drop in exports amid the trade dispute with China.

-

3 As an input for biofuels, soybeans contain roughly 20 percent oil and yield about 50 gallons of biodiesel per acre. To meet current demand for biodiesel, U.S. farmers would need to harvest about 1.4 billion bushels of soybeans per year. At current average yields, that would be equivalent to about 28 million acres of soybeans, or one-third of the 83 million acres harvested in 2023. This estimate is likely a lower bound. The IRA was not signed into law until August 16, 2022, and many of the provisions related to renewable fuel production did not take effect until later in 2023. Oilseed production requirements could expand moving forward.

-

4 The largest vegetable oil crop in the world is palm oil, which makes up about 40 percent of global vegetable oil production. Although palm oil is not produced in the United States, U.S. imports of palm oil have grown rapidly in recent years. Since 2006, palm oil imports have grown about 8 percent each year.

Publication information: Vol. 109, no. 6

DOI: 10.18651/ER/v109n6Cowley

References

Anderson, David, John D. Anderson, and Jason Sawyer. 2008. “Impact of the Ethanol Boom on Livestock and Dairy Industries: What Are They Going to Eat?” Journal of Agricultural and Applied Economics, vol. 40, no. 2, pp. 573–579. Available at External Linkhttps://doi.org/10.1017/S1074070800023853

Cowley, Cortney. 2020. “Reshuffling in Soybean Markets following Chinese Tariffs.” Federal Reserve Bank of Kansas City, Economic Review, vol. 105, no. 1, pp. 5–30. Available at External Linkhttps://doi.org/10.18651/ER/v105n1Cowley

EIA (U.S. Energy Information Administration). 2024. “Biofuels Explained: Biodiesel, Renewable Diesel, and Other Biofuels.” February 26.

Gruber, Joseph W., and Robert J. Vigfusson. 2018. “Interest Rates and the Volatility and Correlation of Commodity Prices.” Macroeconomic Dynamics, vol. 22, no. 3, pp. 600–619. Available at External Linkhttps://doi.org/10.1017/S1365100516000389

Hirtzer, Michael, and Dominic Carey. 2023. “The U.S. Is Losing the Corn-Exporting Crown.” Bloomberg, August 31.

Isom, Loren, and William L. Booker. 2008. “Growing Crops for Better Biodiesel.” University of Nebraska-Lincoln, Agricultural Economics Department, Presentations, Working Papers, and Gray Literature: Agricultural Economics, February.

Katchova, Ani L., and Ana Claudia Sant’Anna. 2019. “Impact of Ethanol Plant Location on Corn Revenues for U.S. Farmers.” Sustainability, vol. 11, no. 6512. Available at External Linkhttps://doi.org/10.3390/su11226512

Kropp, Jaclyn, and Janet G. Peckham. 2015. “U.S. Agricultural Support Programs and Ethanol Policies Effects on Farmland Values and Rental Rates.” Agricultural Finance Review, vol. 75, no. 2, pp. 169–193. Available at External Linkhttps://doi.org/10.1108/AFR-06-2014-0015

Sanicola, Laura. 2024. “Chevron Idles Two U.S. Midwest Biodiesel Plants as Profits Slip.” Reuters, March 1.

Veloso, Tarso. 2023. “The U.S. Is Losing the Race with Brazil for Soybean Dominance.” Bloomberg, October 19.

White House. 2023. “Remarks by President Biden on Helping Workers and Innovators Invent and Make More in America.” Speech delivered at Auburn Manufacturing, Inc., Auburn, ME, July 28.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author