Lending at commercial banks associated directly with farm production strengthened in the second quarter. According to the Survey of Terms of Lending to Farmers, the volume of new operating loans increased 20% from a year ago, which followed a year-over-year increase of 12% last quarter. The rise in lending activity was primarily attributed to larger loan sizes at small and mid-sized lenders and was accompanied by a slight increase in average interest rates and slightly longer maturities.

Following several years of subdued activity, demand for farm loans has rebounded alongside elevated production expenses and a moderation in farm sector liquidity. Alongside strong growth in new lending, outstanding non-real estate loan balances at commercial banks have surged.

Despite climbing swiftly from low levels in recent years, outstanding balances and new volumes of operating debt remain below historic averages after adjusting for inflation. Additional contraction in farm incomes and liquidity would likely increase financing needs further and interest costs could become increasingly burdensome for some agricultural producers.

Second Quarter National Survey of Terms of Lending to Farmers

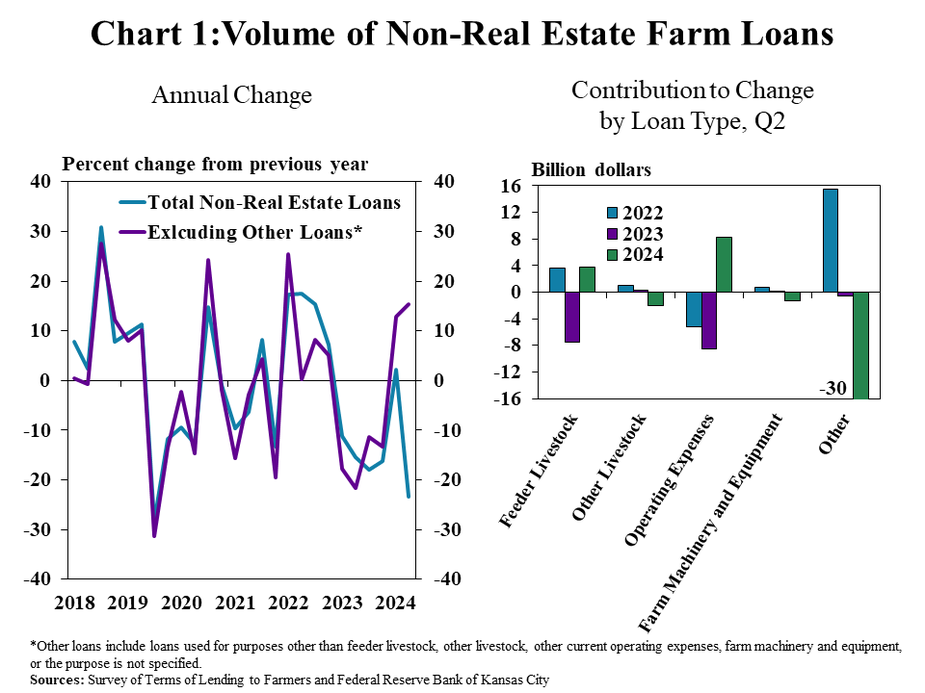

Non-real estate lending at commercial banks tied directly to farm production grew considerably for the second consecutive quarter. The volume of loans for key types of farm debt increased by more than 15% from a year ago, primarily attributed to growth in feeder livestock and operating expenses (Chart 1). Loan demand attributed to primary activities was strong while lending for other loans that typically fund non-specified and miscellaneous purchases slowed significantly, which could indicate that producers have perhaps cut back on more discretionary purchases.

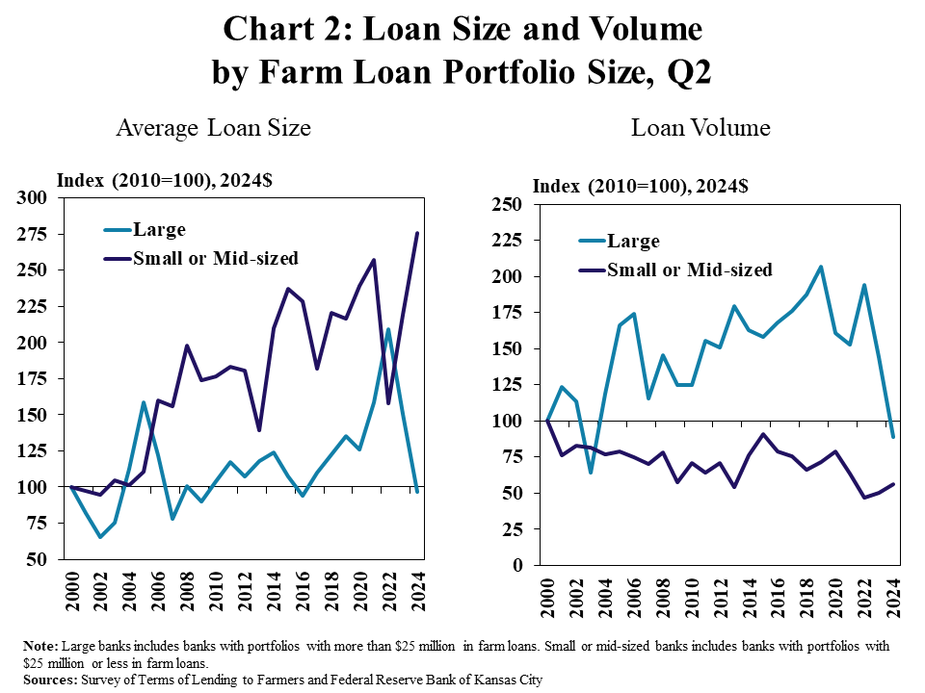

The strong growth in lending activity associated with production was spurred by larger sized loans at small and mid-sized lenders. The average size of loans reported by small or mid-sized banks increased to a record high for the second quarter and the size of loans at large banks dropped considerably (Chart 2). The drop in loan size cut lending volumes at large banks to a 20-year low. Meanwhile, volumes at smaller lenders grew from historically low levels last year but remained less than previous decades.

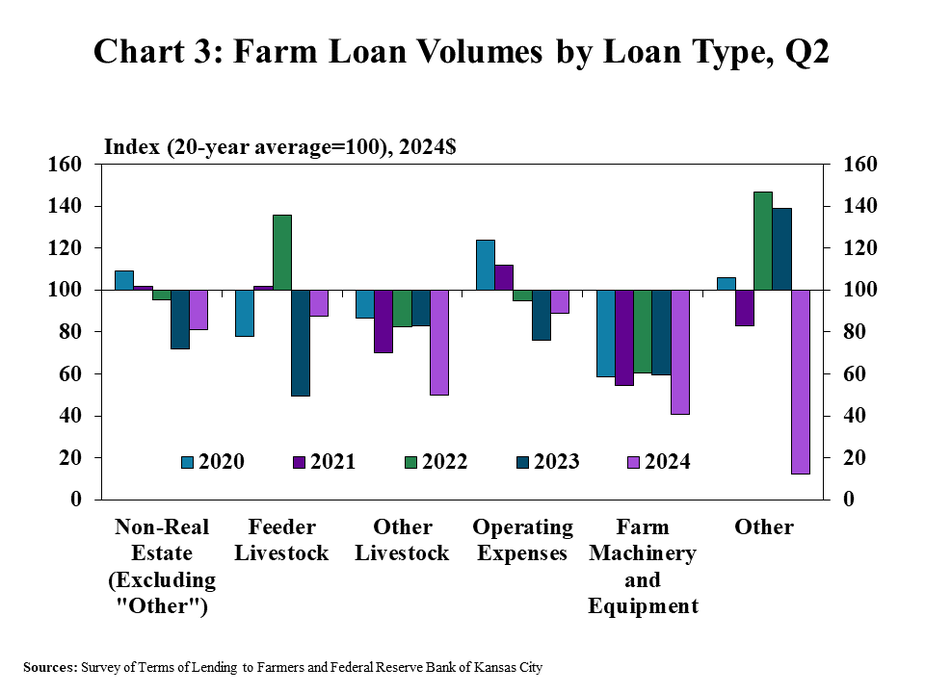

Despite the notable pace of growth, lending volumes for most major loan types also remained subdued on an inflation-adjusted basis. The volume of non-real estate loans was still 20% less than the average of the second quarter over the past two decades (Chart 3). Farm machinery lending was particularly subdued, dropping to a level 40% below the recent historic average.

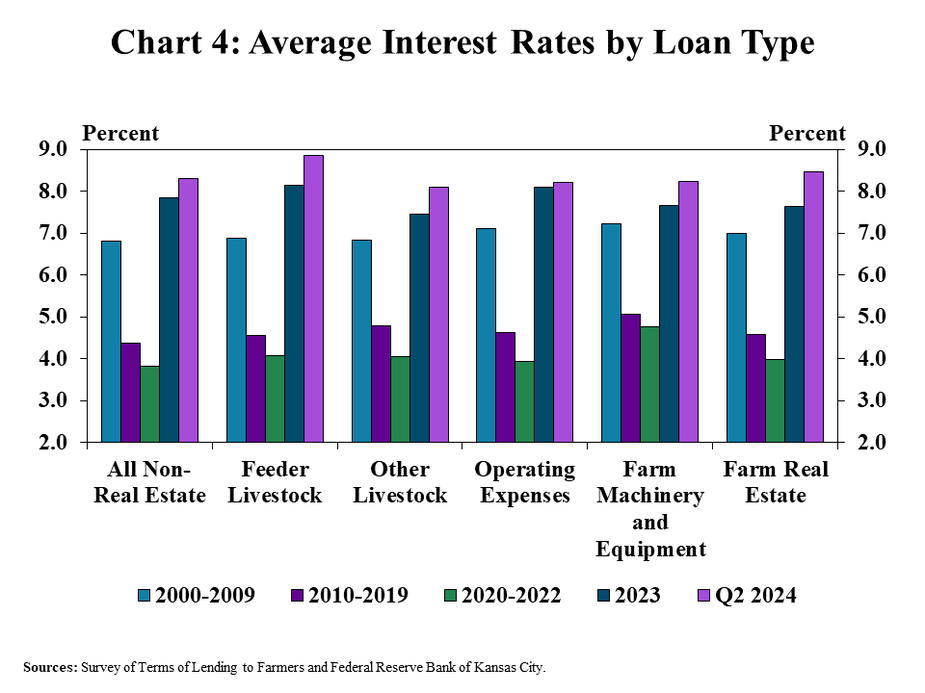

Lending activity picked up despite interest rates on farm loans hovering at multi-decade highs. The average interest rates charged on all types of agricultural loans notched up slightly from the previous quarter and have been above the average of recent decades since early 2023 (Chart 4). The combination of higher lending volumes and elevated interest rates is likely to be particularly burdensome for highly leveraged borrowers.

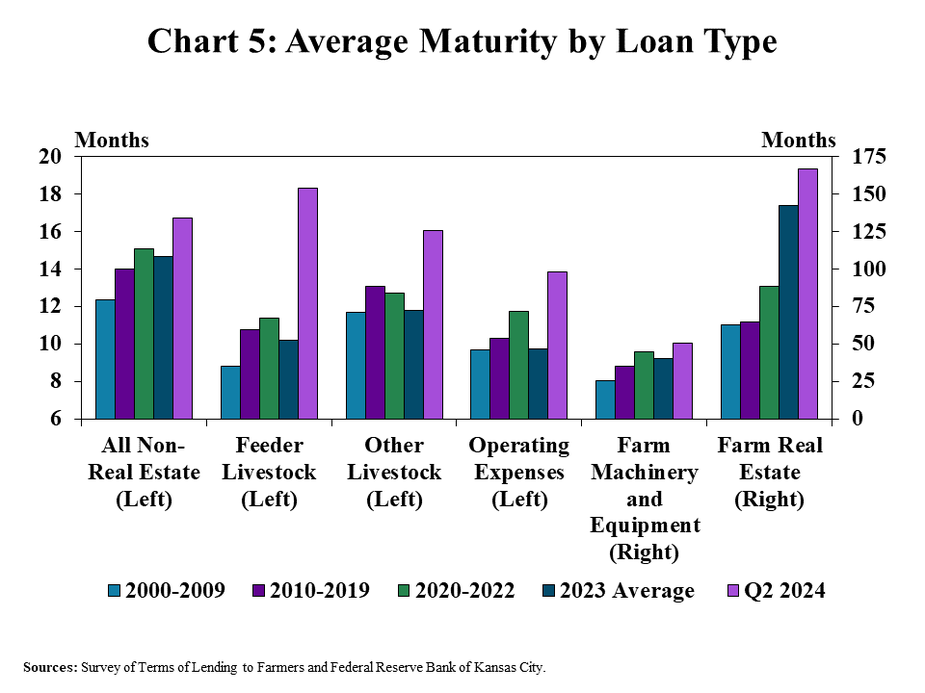

As interest rates have risen, average loan maturities have also grown. The average duration of non-real estate loans was about two months longer than the average of recent years (Chart 5). The expansion of loan length was even notable for livestock and operating loans, which have historically been booked on terms of one year or less.

Data and Information

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Tables

About the National Survey of Terms of Lending to Farmers

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy