Pay-by-Bank, also known as account-to-account (A2A) or bank-based payment, is an emerging payment method for retail transactions around the world. In a Pay-by-Bank transaction, the consumer makes a payment by directly transferring funds from their bank account to the merchant’s bank account via an electronic fund transfer network, such as Automated Clearing House (ACH), or an instant payment network, such as FedNow or Real-Time Payments (RTP). Pay-by-Bank may provide consumers with greater clarity over their spending and potentially improve budget control and cashflow management (Glaser 2024). For merchants, Pay-by-Bank can be a substantially less costly method of payment acceptance than card payments, especially credit card payments (Hwang 2025).

In the United States, Pay-by-Bank is gaining traction as a payment method for online transactions, especially online bill payments, but has yet to penetrate physical points of sale (POS). However, merchants are increasingly interested in offering Pay-by-Bank for in-store transactions. This Payments System Research Briefing uses recent data from the Survey and Diary of Consumer Payment Choice (SDCPC) to assess the readiness of U.S. consumers to adopt Pay-by-Bank at the POS.

How Pay-by-Bank works at the POS

The two most common types of Pay-by-Bank at the POS are “scan to pay,” which uses Quick Response (QR) codes, and “tap to pay,” which uses near-field communication (NFC) technology. Both methods require the use of a mobile device to make payments, meaning that POS Pay-by-Bank payments will be a form of mobile payments for U.S. consumers.

In a scan-to-pay Pay-by-Bank transaction, the merchant presents a QR code at checkout at the customer’s request. The QR code encodes the merchant’s bank account details and may either be static—that is, the same for every transaction—or dynamic, which is transaction-specific and embeds the transaction amount. On their mobile device, the consumer opens their banking app or payment app linked to their bank account, selects the Pay-by-Bank option, and scans the merchant’s QR code with their device’s camera. The app decodes the QR code and automatically fills in the merchant’s payment details. If the QR code is static, the consumer must enter the transaction amount. The consumer then verifies that the transaction details are correct and authorizes the payment. Before initiating the payment, the app may perform additional authentication._

A tap-to-pay Pay-by-Bank transaction follows similar steps; however, instead of scanning the merchant’s QR code, the consumer holds their mobile device near or taps it on the merchant’s payment terminal. The merchant’s bank account details and the transaction amount are then transmitted from the payment terminal to the consumer’s mobile device via NFC.

The most likely Pay-by-Bank method to be implemented in the United States could differ from the most common method in other parts of the world. Globally, scan to pay is the more common Pay-by-Bank method, likely because in many countries it costs less to deploy than tap to pay. When static QR codes are used, scan to pay does not require merchants to have any specialized POS equipment, whereas tap to pay requires merchants to have NFC-capable POS terminals. Many countries that have implemented Pay-by-Bank have relatively few merchants that have adopted NFC-capable POS equipment. In the United States, however, most merchants already have NFC-Capable POS terminals (Mordor Intelligence 2026). Accordingly, scan to pay is unlikely to have a substantial cost advantage. Moreover, because U.S. consumers particularly value speed and convenience at checkout, implementing tap to pay may be more advantageous (NCR Voyix 2025). U.S. consumers who already make mobile payments (funded by credit or debit cards) at the POS are also likely more familiar with tap to pay._ According the 2025 SDCPC, around 70 percent of all mobile payments that U.S. consumers made at the POS were tap to pay, while only 5.2 percent were scan to pay._

Readiness of U.S. consumers to adopt Pay-by-Bank at the POS

Regardless of the Pay-by-Bank method implemented at the POS in the United States, consumers will need a mobile banking or mobile payment app installed on their device—and knowledge of how it works—before they can use it. I assess U.S. consumers’ readiness to adopt Pay-by-Bank at the POS using recent data from the SDCPC to examine the extent to which consumers currently possess the technology and savviness to make these payments.

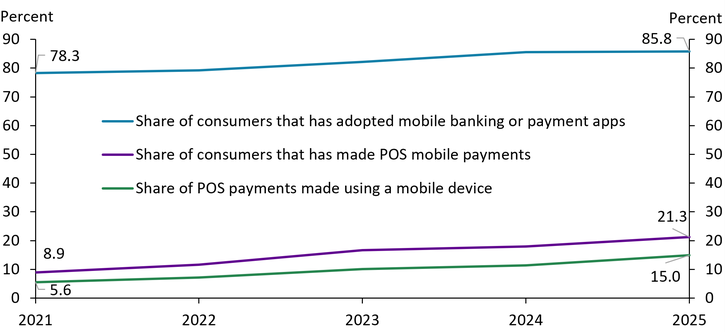

Consumers who have adopted mobile banking or mobile payment apps are conceivably more likely to have the technology needed to use Pay-by-Bank at the POS when it is implemented. Chart 1 shows that the share of U.S. consumers that has adopted mobile banking or payment apps (blue line) has been growing: From 2021 to 2025, this share increased from 78.3 percent to 85.8 percent. This finding indicates that, as of 2025, most U.S. consumers likely have the technological capability to use Pay-by-Bank at the POS. The share of consumers who are technologically capable of using Pay-by-Bank at the POS is likely to continue to increase in the coming years.

Chart 1: U.S. consumers have increasingly adopted mobile banking or payment apps and used mobile payments at the POS

Sources: Federal Reserve Bank of Atlanta and author’s calculations.

To assess whether U.S. consumers have the practical knowledge to use Pay-by-Bank at the POS, I examine their existing use of mobile payments at the POS. The purple line in Chart 1 shows the share of U.S. consumers that made mobile payments at the POS, which captures the breadth of consumers’ exposure to POS mobile payments, while the green line shows the share of POS payments that U.S. consumers made using a mobile device, which captures the depth of their exposure. Both shares have grown steadily over the past five years. From 2021 to 2025, the share of U.S. consumers that made mobile payments at the POS more than doubled (from 8.9 percent to 21.3 percent) and the share of POS transactions that consumers made using a mobile device nearly tripled (from 5.6 percent to 15 percent). Although these shares are still relatively small, suggesting that the share of U.S. consumers with the knowledge to use Pay-by-Bank at the POS is currently small, they are likely to continue trending up.

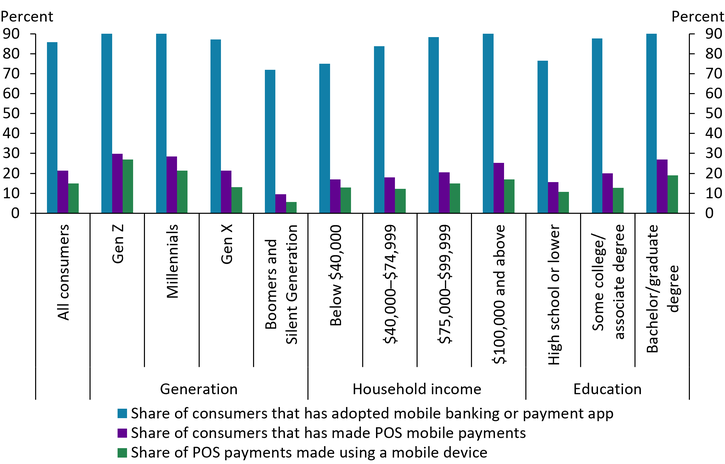

Data from the SDCPC also suggest that some types of consumers are more ready to use Pay-by-Bank at the POS than others. Chart 2 shows that the share of consumers that has adopted mobile banking or payment apps (blue bar), the share of consumers that has made POS mobile payments (purple bar), and the share of POS payments consumers made using a mobile device (green bar) are all higher among younger, higher-income, and more highly educated consumers. Consumers who are millennials or younger, have an income of $100,000 or more, and have a bachelor’s or higher degree lead the way in both the adoption of mobile banking or payment apps and the use of mobile payments at the POS, suggesting they are most likely to have the technical capability and know-how to use Pay-by-Bank at the POS. In contrast, consumers who are baby boomers or older, have an income of less than $40,000, or have a high school or less education, have considerably lower rates of mobile banking or payment app adoption and use of mobile payments at the POS, suggesting these consumers may be the least ready to adopt Pay-by-Bank at the POS. Consumers from the boomer or Silent Generation may especially lack the knowledge to make Pay-by-Bank payments at the POS: In 2025, only 9.6 percent of these consumers made mobile payments at the POS, and mobile payments constituted only 5.7 percent of their POS payments.

Chart 2: Adoption of mobile banking or payment apps and use of mobile payments at the POS are higher among younger, higher-income, and more highly educated consumers

Sources: Federal Reserve Bank of Atlanta and author’s calculations.

Overall, while most U.S. consumers are likely to have the technological capability needed to make Pay-by-Bank payments at the POS, only a relatively small share may currently have the knowledge to do so, suggesting that consumers’ overall readiness to adopt Pay-by-Bank at the POS may still be relatively low. That said, U.S. consumers’ readiness to adopt Pay-by-Bank payments at the POS has grown over the last five years and is likely to continue to grow going forward. Consumers who are younger, higher-income, and more highly educated are the most likely to have both the technological capability and savviness to use Pay-by-Bank at the POS and are most likely to be early adopters. Additionally, I find that U.S. consumers likely have higher readiness to make Pay-by-Bank payments at the POS via tap to pay rather than scan to pay.

Will U.S. consumers choose Pay-by-Bank at the POS?

Although having the technological capability and knowledge to use Pay-by-Bank at the POS is critical to its adoption, whether U.S. consumers ultimately choose this payment option—once it becomes available— may also depend on their perceptions of Pay-by-Bank. If consumers perceive Pay-by-Bank to be less safe or financially less advantageous than their existing payment instruments, they may choose not to switch. At present, U.S. consumers most commonly use credit and debit cards to pay at the POS: According to SDCPC, these two instruments accounted for 75 percent of all POS transactions and 88 percent of funding sources for POS mobile payments in 2025. U.S. consumers receive strong buyer and fraud liability protection for card transactions, especially credit card transactions; they also typically receive financial rewards for paying with their credit cards. U.S. consumers may need to receive similarly strong protection and financial incentives to choose Pay-by-Bank over debit and credit cards at the POS.

Endnotes

-

1 Pay-by-Bank can also work via consumer-presented QR codes. See Bradford, Hayashi, and Toh (2019) for more information on how consumer-presented QR codes can be used to make payments.

-

2 U.S. consumers typically use scan to pay when paying at the POS with a person-to-person payment app, such as PayPal or Cash App, and tap to pay when paying with mobile wallets, such as Apple Pay and Google Pay.

-

3 Tap to pay’s dominance over scan to pay (and other methods for paying with a mobile phone at the POS) may be attributed to the increasing popularity of mobile wallets such as Apple Pay and Google Pay among U.S. consumers. According to data from the SDCPC, from 2021 to 2025, the share of U.S. consumers that adopted Apple Pay increased from 13.2 percent to 25.7 percent, while the share that adopted Google Pay increased from 7.2 percent to 10.9 percent. Market analysts expect tap-to-pay payments via mobile wallets to continue to grow (Consumer Financial Protection Bureau 2023).

Article Citation

Toh, Ying Lei. 2026. “Are U.S. Consumers Ready to Use Pay-by-Bank at the Point of Sale?” Federal Reserve Bank of Kansas City, Payments System Research Briefing, July 15.

References

Bradford, Terri. 2021. “Are Contactless Payments Finally Poised for Adoption?” Federal Reserve Bank of Kansas City, Payments System Research Briefing, April 14.

Bradford, Terri, Fumiko Hayashi, and Ying Lei Toh. 2019. “Developments of QR Code-Based Mobile Payments in East Asia.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, June 18.

Consumer Financial Protection Bureau. 2023. “External LinkBig Tech's Role in Contactless Payments: Analysis of Mobile Device Operating Systems and Tap-to-Pay Practices.” Issue Spotlight, September 7.

Glaser, Dave. 2024. “External LinkWhy Pay by Bank is Safer Than You Think.” Digital Transactions, November 1.

Hwang, Byoung Hwa. 2025. “External LinkPay-by-Bank and the Merchant Payments Use Case: Benefits, Risks and Potential Impacts on Consumer Payment Behaviors in the U.S.” Board of Governors of the Federal Reserve System, FEDS Notes, July 7.

Mordor Intelligence. 2026. “External LinkUnited States POS Terminals Market Report.”

NCR Voyix. 2025. “External Link77% of Shoppers Choose Self-Checkout for Faster Service, According to New Consumer Survey from NCR Voyix.” January 10.

Ying Lei Toh is a senior economist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author