In the United States, having no or low credit scores can be a substantial barrier to obtaining affordable credit at mainstream rates. Some consumers with low or no credit scores may be creditworthy but lack the credit data from which credit scores are traditionally derived. In recent years, reporting rent payments to credit bureaus has emerged as a way to expand the data available for credit scoring, with newer credit scoring models incorporating reported rent data. However, the ultimate effect of rent reporting on credit access is unknown.

Ying Lei Toh finds that rent reporting could affect the credit scores of around 60 percent of U.S renters: Roughly 43 percent could see relatively large improvements in their credit scores, while the remaining 17 percent could see only modest improvements or even declines. Toh also finds that rent reporting may especially affect the credit scores of renters with unmet credit needs, though the share of these renters who would see only modest improvements or even declines in their credit scores with rent reporting is also greater than for renters without unmet credit needs. The ultimate effect will likely depend not only on the type of rent reporting but also on renters’ preexisting credit files.

Article Citation

Toh, Ying Lei. 2026. “Building Credit with Rent Data: The Potential Effects of Rent Reporting on the Credit Scores of U.S. Renters.” Federal Reserve Bank of Kansas City, Economic Review, vol. 111, no. 5. Available at External Linkhttps://doi.org/10.18651/ER/v111n5Toh

Introduction

In the United States, having no or low credit scores (specifically, FICO or VantageScore credit scores) can be a substantial barrier to obtaining affordable credit at mainstream rates. Mainstream lenders rely heavily on credit scores to assess consumers’ creditworthiness and often deem consumers with low (especially subprime) or no credit scores to be uncreditworthy. However, some of these consumers may in fact be creditworthy but simply lack the credit data from which credit scores are traditionally derived.

In recent years, rent reporting—that is, landlords or tenants reporting rent payments to credit bureaus—has emerged as a way to expand the data available for credit scoring. Newer FICO and VantageScore credit scoring models incorporate reported rent data in addition to traditional credit data when generating renters’ credit scores, which may enable renters with limited to no traditional credit data to establish or increase their credit scores. A TransUnion survey found that 13 percent of renters had their rent reported to credit bureaus in 2025. This share is likely to grow as rent reporting continues to gain popularity among renters (to build credit) and landlords (to motivate tenants to pay rent on time). However, the ultimate effect of rent reporting on credit access is an open question. While rent reporting could aid credit scores for some consumers with otherwise limited credit histories, it could also damage credit scores for tenants with rent delinquencies.

In this article, I assess how rent reporting could affect the credit scores of U.S. renters. I find that rent reporting could lead to changes in the credit scores of around 60 percent of U.S renters: Around 43 percent of U.S. renters could see relatively large improvements in their credit scores, while the remaining 17 percent could see only modest improvements or even declines. Additionally, I find that rent reporting may especially materially affect the credit scores of renters with unmet credit needs in the mainstream credit market, who may arguably benefit more from an improvement in their credit scores. Around 48 percent of renters with unmet credit needs could see relatively large improvements in their credit scores, compared with around 40 percent of renters without unmet credit needs. However, the share of renters with unmet credit needs who would likely either see only modest improvements or could even see declines in their credit scores with rent reporting is also higher than for renters without unmet credit needs (31 percent versus 9 percent). The ultimate effect on the credit scores of U.S. renters will likely depend not only on the type of rent reporting but also the renters’ preexisting credit files.

Section I provides an overview of rent reporting in the United States. Section II discusses the factors that influence how rent reporting affects a renter’s credit scores. Section III examines how rent reporting may affect the credit scores of U.S. renters.

I. Rent Reporting in the United States

Rent payments are one of the largest monthly expenses for renters. A renter’s ability to keep up with rent payments is thus arguably a good indicator of their ability to meet their financial obligations, such as loan repayments. However, because rent is not considered a form of debt, rent payments have historically not been reported to credit bureaus._ Even in the few cases when rent payments were reported to credit bureaus, they were unlikely to have an effect: Until recently, FICO Score and VantageScore—the two most broadly used credit scores—did not factor in alternative data such as rent into their scores.

The rent reporting landscape started to evolve in the mid-2010s, after VantageScore and FICO began incorporating reported rent data into their credit scoring models._ This inclusion provided renters and landlords with new incentives to report rent. For renters, rent reporting provided a way to establish credit scores or improve their existing credit scores. For landlords, rent reporting provided additional motivation for renters to pay rent on time. In line with these incentives, the change to VantageScore and FICO’s scoring models led to a proliferation of rent reporting services, which allow both landlords and renters to easily report rent payments to one or more of the three major credit bureaus (Equifax, Experian, and TransUnion)._ Accordingly, the share of renters whose rent payments are reported to credit bureaus have increased over time.

In recent years, several federal agencies and state governments have also taken steps to promote rent reporting because of its potential to help improve renters’ access to affordable credit. In particular, most of these efforts have focused on “positive-only” rent reporting, in which only on-time payments are reported to credit bureaus. In 2022, the Federal Housing Finance Authority (FHFA) began transitioning to two new credit scoring models that incorporate reported rent data for use by Freddie Mac and Fannie Mae. In January 2025, the U.S. Department of Housing and Urban Development (HUD) published a set of frequently asked questions to provide HUD-assisted housing providers with greater clarity around positive-only rent reporting. At the state level, California passed a law in 2020 requiring landlords of assisted housing properties with 15 or more units to offer their tenants the option of positive-only rent reporting; in 2024, the law was expanded to include many landlords of market-rate properties (Hermans, Theodos, and Teles 2025). As of the end of 2025, Missouri, North Carolina, and Minnesota have proposed similar laws. That said, existing federal regulations and state regulations in most states generally offer limited guidance on rent reporting by landlords._

Previous studies on rent reporting have lent some credence to these efforts. Several researchers have found that rent reporting, particularly positive-only rent reporting, can indeed help renters with nonexistent credit scores establish credit scores and those with subprime credit scores to increase their scores (Theodos, Teles, and Lieberman 2025; VantageScore 2025; Turner and Walker 2019; Office of the New York City Comptroller 2017; Chenven and Schulte 2015). However, these studies also showed that the effects of rent reporting varied across renters. Not all participating renters with subprime credit scores saw their credit scores increase; among those who did, many continued to have subprime scores, suggesting rent reporting may not have materially improved their access to affordable credit. Furthermore, the type of rent reporting influences its effect on credit access. If bureaus receive “full-file” rent reporting—that is, reports of both on-time and delinquent rent payments—renters with delinquencies could see sizeable declines in their credit scores, thereby worsening their access to affordable credit (Turner and Walker 2019).

Although these past studies have shed light on the effects of rent reporting on renters’ credit scores and credit access, the renters participating in these studies were not representative of the U.S. renter population. As rent reporting continues to grow, a better understanding of how it may affect U.S. renters will help inform rent reporting policies.

II. Factors Determining How Rent Reporting Affects Renters’ Credit Scores

Rent reporting provides additional data on a renter’s creditworthiness, which may affect both a renter’s ability to obtain a credit score and the credit score they obtain. Renters who have little to no traditional credit data may not be able to obtain a credit score based on traditional credit data alone, as generating a FICO Score or VantageScore requires some minimum amount of data. For example, generating a FICO Score requires at minimum an account with at least six months of history and activity on an account in the past six months; generating a VantageScore requires an account with at least one month of history. For renters who do not meet these minimums through traditional credit accounts, rent reporting may help provide the data required to generate a credit score. Many of these renters are likely to have sufficiently long rental histories that would meet the minimum data requirements of at least one credit scoring model._

For renters who do have enough data to generate a credit score, the additional data provided by rent reporting may help paint a more accurate picture of their creditworthiness, thereby altering the credit scores they obtain. A key factor in determining the extent to which rent reporting may alter these renters’ credit scores is the amount of traditional credit data they have. In general, smaller quantities of data tend to be noisier and provide less accurate signals of renters’ creditworthiness, which can result in lower and less predictive credit scores (Blattner and Nelson 2024)._ Including reported rent data in credit scoring may thus especially improve predictiveness and lead to more sizeable changes in the credit scores of renters with smaller amounts of traditional credit data, such as those with relatively young or few credit accounts. The improvement additional data offers to the predictiveness of a renter’s credit score diminishes with the amount of data used in credit scoring._ For renters with older and more substantial credit histories, rent reporting may thus have a more limited effect.

Although rent reporting is likely to have greater effects on the credit scores of renters with limited to no traditional credit data, these effects could be positive or negative depending on whether the reported rent data signal higher or lower creditworthiness. Credit scoring models assess consumers’ creditworthiness based on several factors—payment history, amounts owed, age of accounts, credit mix, and recent credit (see Box in Toh 2023 for a more detailed discussion of these factors). Among these factors, payment history is the most influential, accounting for 35 to 40 percent of a consumer’s credit score. Thus, rent payment history is likely to be a key determinant of the credit scores of renters with limited to no traditional credit data.

Reported on-time rent payments can help a renter establish a good payment history or improve their existing payment history, whereas reported delinquent rent payments can have the opposite effect. In general, for a given renter’s payment history, the effect of rent reporting is likely to be most positive when the renter always pays their rent on time. If the renter has been delinquent on their rent payments, the effect of rent reporting may further depend on whether the reporting is positive only or full file. Full-file reporting, in which delinquent payments are also reported, has a less positive effect than positive-only reporting on a renter’s credit score if the renter has been delinquent on their rent payments. In some cases, particularly those in which a renter’s rent delinquencies are frequent or severe (as measured by the number of days past due), full-file reporting may have a negative effect on the renter’s credit score.

Rent reporting may also influence a renter’s credit mix and age of accounts—two other factors that determine their overall credit score—though these factors are likely to have a relatively small effect compared with payment history, particularly for renters with limited to no credit or debt payment history. Rent reporting is likely to have a positive effect on a renter’s credit mix, as it adds a recurring non-debt payment account to the renter’s existing account types, increasing their account diversity. In contrast, rent reporting may not always have a positive effect on a renter’s age of accounts. For renters with relatively old credit or debt accounts, their rental tradeline is likely to be younger than their other accounts, which could lower their credit score. For renters who are new to the credit market, however, their rental tradeline may be older than their other accounts, which could increase their credit score._

In summary, the effect of rent reporting on credit scores is likely to vary from renter to renter, with this variation largely determined by the amount of traditional credit data a renter has and their rent payment history. Rent reporting is more likely to have a sizeable effect on the credit scores of renters with limited to no traditional credit data. For these renters, rent reporting is likely to lead to higher newly established credit scores or larger improvements in existing credit scores if they pay their rent on time or if any delinquent payments are not reported (as through positive-only reporting)._ However, if these renters have delinquent payments—and if these payments are reported (as through full-file reporting)—rent reporting could lead to a material decline in their credit scores. In contrast, renters with large quantities of traditional credit data are likely to see little to no change in their credit scores with rent reporting.

III. The Potential Effects of Rent Reporting on the Credit Scores and Credit Access of U.S. Renters

To assess how rent reporting—both positive only and full file—may affect the credit scores of the U.S. renter population, I use data from the 2024 Survey of Household Economics and Decisionmaking (SHED). The SHED is an annual survey conducted by the Board of Governors of the Federal Reserve to assess the economic well-being of U.S. households and contains information on renter status, rent delinquencies, and self-assessed credit scores. The SHED also includes survey weights, which can be used to create a representative sample of the U.S. renter population. According to the 2024 SHED, 28 percent of U.S. consumers are renters and may potentially be affected by rent reporting.

As discussed in the previous section, two key factors determining how rent reporting may affect a renter’s credit scores are the amount of traditional credit data they have and their rent payment history. I first divide the renters into two groups depending on whether they are likely to have thin/no credit files or thick credit files, which determines whether they are likely to experience material changes in their credit scores with rent reporting. I then divide renters by whether they were delinquent on their rent payments, which determines the potential direction of the change in their credit scores.

The 2024 SHED does not contain information about consumers’ traditional credit data; however, it does provide information on consumers’ self-assessed credit score tier (excellent, good, fair, poor, very poor, don’t know, or missing). Renters with high credit scores generally have relatively thick credit files, whereas renters with low or nonexistent credit scores tend to have thin or no credit files. Thus, to the extent that consumers’ self-assessed credit scores are accurate, having a high self-assessed credit score may serve as proxy for having thick credit files._ Accordingly, I use renters’ self-reported credit score tiers to divide them into two groups: those who likely have thin or no credit files and those who likely have thick credit files.

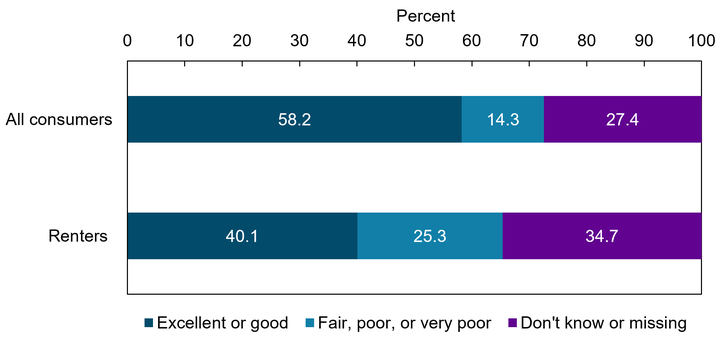

Chart 1 shows the breakdown of all U.S. consumers and U.S. renters only by their self-assessed credit score tier. The top bar shows that the share of U.S. consumers who self-assessed their credit scores to be good or excellent (dark blue segment) is 58.2 percent. This share is close to the estimated shares of consumers with prime or near-prime credit scores reported in Hepinstall and others (2022) and Board of Governors of the Federal Reserve System (2025), suggesting that consumers who self-assessed their credit scores to be good or excellent may indeed have relatively high (near prime or better) credit scores.

Chart 1: Around 60 Percent of U.S. Renters Likely Have Low or Nonexistent Credit Scores

Note: The shares in each bar may not sum to 100 due to rounding.

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

The bottom bar in Chart 1 shows that the share of renters whose self-assessed credit score was excellent or good (dark blue segment) is around 40 percent, and the share of renters whose self-assessed credit score was fair, poor, very poor, don’t know, or missing (light blue and purple segments) is around 60 percent (25.3 + 34.7 percent). This finding implies that around 60 percent of renters could establish or see improvements in their credit scores through rent reporting. This share is likely to be an upper bound, as some renters with low credit scores may have thick credit files (meaning their low credit score accurately signals low creditworthiness rather than a lack of data) and a small share of renters with low scores may already be participating in rent reporting (meaning their credit score already factors in their rent payments). For simplicity going forward, I refer to renters whose self-assessed credit score was excellent or good as renters who likely have high credit scores, and those whose self-assessed score was fair, poor, very poor, don’t know or missing as renters who likely have low or nonexistent credit scores.

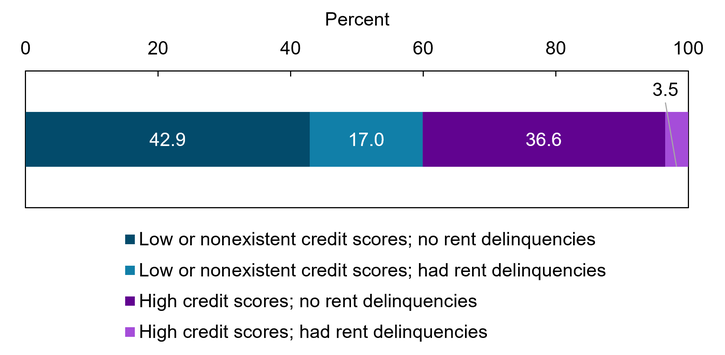

Next, to determine the direction of the effect that rent reporting may have on the credit scores of U.S. renters, I examine whether renters in both credit score categories were delinquent on their rent payments. All else equal, renters who had no rent delinquencies (79.9 percent of all renters) would establish higher credit scores or experience larger improvements in their credit scores than renters who had rent delinquencies, regardless of the type of rent reporting. Additionally, some renters with rent delinquencies may see their credit scores decline with full-file reporting. According to the 2024 SHED, 71.6 percent of renters who likely have low or nonexistent credit scores and 91.2 percent of renters who likely have high credit scores had no rent delinquencies.

Chart 2 combines the above findings. Around 43 percent (0.716 x 59.9) of U.S. renters likely have low or nonexistent credit scores and were not delinquent on rent (dark blue bar). For these renters, rent reporting is likely to have the highest benefit, yielding relatively high new credit scores or relatively large improvements in existing credit scores. Because these renters had no delinquencies, they would experience the same outcome regardless of whether the rent reporting was positive only or full file. An additional 17 percent of U.S. renters also likely have low or nonexistent credit scores but were delinquent on rent (light blue bar). For these renters, rent reporting is likely to have a greater benefit under positive-only reporting than full-file rent reporting. With positive-only rent reporting, these renters could establish credit scores (though the scores would likely be lower than those of renters with no rent delinquencies) or see moderate improvements in their credit scores._ With full-file rent reporting, however, some of these renters—particularly those with more frequent or severe delinquencies—may see their credit scores worsen. Finally, Chart 2 shows that 40.1 percent of U.S. renters likely have high credit scores—36.6 percent with no rent delinquencies (dark purple bar) and 3.5 percent with rent delinquencies (light purple bar). These renters would be unlikely to see sizeable changes in their credit scores from rent reporting, though the 3.5 percent with rent delinquencies might see some decline in their credit scores.

Chart 2: Breakdown of U.S. Renters by Likely Credit Score Range and Rent Delinquencies

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

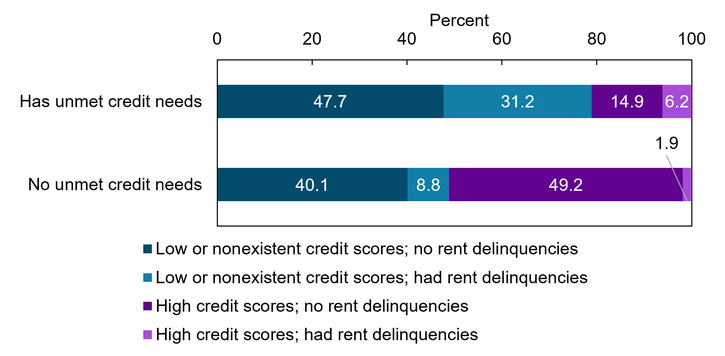

An improvement in credit scores and credit access may arguably benefit renters who have unmet credit needs in the mainstream credit market more than renters who do not have unmet credit needs. To determine a renters’ credit need status, I next review data in the 2024 SHED about consumers’ desire for credit, mainstream credit applications and application outcomes, and use of credit from alternative financial service (AFS) providers. I consider a renter to have unmet credit needs in the mainstream credit market if they applied for mainstream credit but were turned down or granted less credit than requested, desired mainstream credit but did not apply, or used credit from AFS providers. I consider a renter to have no unmet credit needs if they applied for credit and were granted the full amount of credit they had requested or did not desire credit and did not use AFS credit.

Chart 3 shows the shares of renters who likely have low or nonexistent credit scores with and without rent delinquencies as well as the shares of renters who likely have high credit scores with and without rent delinquencies, separated by credit need status. The share of renters who likely have low or nonexistent credit scores (dark blue + light blue segments) is substantially higher among renters with unmet credit needs than among renters with no unmet credit needs. This finding is consistent with low or nonexistent credit scores being a key barrier to accessing mainstream credit. With positive-only rent reporting, up to 78.9 percent of renters with unmet credit needs (dark blue + light blue segments of the top bar) may be able to establish a credit score or see material improvements in their credit scores, compared with only 48.9 percent of renters with no unmet credit needs (dark blue + light blue segments of the bottom bar). However, with full-file reporting, the share of renters with unmet credit needs who may be able to establish a credit score or see relatively large improvements in their credit scores is likely to be considerably smaller, as around 40 percent (0.312 x 78.9 percent) of renters with unmet credit needs who have low or nonexistent credit scores were delinquent on rent. For the same reason, a sizeable share of renters with unmet credit needs could see their credit scores decline with full-file rent reporting.

Chart 3: Potential Effects of Rent Reporting on U.S. Renters Vary by Their Credit Needs Status

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

In summary, my findings show that rent reporting could materially affect the credit scores of a large share (up to 60 percent) of U.S. renters. Within this share, those who had no rent delinquencies stand to see relatively large improvements in their credit scores, regardless of the type of rent reporting. In contrast, those who had rent delinquencies may only see modest improvements with positive-only rent reporting. The change in credit scores that these renters experience with full-file rent reporting would likely be less positive or even negative. Renters with unmet credit needs are more likely to be materially affected by rent reporting than renters without unmet credit needs; however, conditional on being materially affected, they are less likely to experience large improvements in their credit scores and are more likely to see their credit scores decline.

Given that a sizeable share of U.S. renters, particularly those with unmet credit needs, have rent delinquencies, positive-only rent reporting has greater potential to improve credit access among U.S. renters than full-file reporting. With positive-only rent reporting, renters who have delinquencies are more likely to see improvements in their credit scores—at the very least, most would not see their credit scores decline.

Conclusion

A sizeable share of U.S. consumers has low or nonexistent credit scores, which can severely limit their access to affordable credit. Many of these consumers may in fact be creditworthy but have limited to no traditional credit data to demonstrate their creditworthiness. I examine rent reporting as a potential means to help improve credit access among renters with low or nonexistent credit scores. Using data from the 2024 SHED, I find that a substantial share of U.S. renters may have thin or no credit files and could see material changes in their credit scores from rent reporting. Many of these renters may be able to establish credit scores or increase their credit scores with rent reporting, though some renters with rent delinquencies could also see their credit scores decline.

Although rent reporting, particularly positive-only rent reporting, may potentially help a substantial share of renters with low or nonexistent credit scores establish or increase their credit scores, it may only lead to significant improvement in credit access for a subset of these renters. Findings from existing studies suggest that even with positive-only rent reporting, many U.S. renters with subprime or nonexistent credit scores are likely to still have subprime credit scores and may continue to face difficulties accessing affordable credit. A likely explanation for these findings is that many renters with subprime or nonexistent credit scores may indeed have low creditworthiness. Rent reporting provides additional data for credit scoring, which can increase the predictiveness of credit scores of renters with thin credit files. But this increase in predictiveness would only raise these renters’ credit scores to the extent that they are creditworthy. Thus, rent reporting is likely to alleviate subprime or nonexistent credit scores as a barrier to credit access only for renters with thin or no credit files who are creditworthy.

In addition to its potential effects on renters’ credit scores, rent reporting may also have implications for housing access (Wu 2024). Many landlords use credit scores and credit reports to screen tenants and may refuse to rent to those with a history of rent delinquencies. With full-file rent reporting, landlords can directly observe a renter’s past rent delinquencies in their credit reports. Although positive-only reporting does not explicitly reveal delinquent rent payments, landlords nevertheless may be able to infer from gaps in reported on-time payments that a renter had been delinquent on rent payments. Thus, the implications of rent reporting for housing access may also be important considerations for policymakers looking to promote credit access through rent reporting.

Endnotes

-

1 Until recently, most landlords could not easily report rent to credit bureaus even if they wanted to do so. Only landlords or rental payment processing companies who were credentialed data furnishers could directly report rent payments to credit bureaus. As a result, only unpaid rent that had been sent to a collections agency was typically reported (by the collections agency) as debt to credit bureaus.

-

2 VantageScore released its first version of credit scores that factored in reported rent payments (VantageScore 3.0) in 2013, while FICO released its first version (FICO Score 9) in 2014.

-

3 Additionally, some property management software also began offering landlords automated rent reporting services within their software.

-

4 Most landlords are by law neither required to offer their tenants the option of rent reporting nor prevented from reporting their tenants’ rent payments without their consent (though landlords are required to inform their tenants if their rent payments are reported).

-

5 In existing rent reporting studies, most participating renters who did not have a credit score pre-rent-reporting obtained a credit score with rent reporting (Theodos, Teles, and Lieberman 2025; VantageScore 2025; Turner and Walker 2019; Office of the New York City Comptroller 2017; Chenven and Schulte 2015).

-

6 Derogatory events such as missed or late payments tend to have outsized negative effects on the credit scores of renters who have limited amounts of traditional credit data, which tends to result in low credit scores that may understate these renters’ true creditworthiness.

-

7 Existing studies have found that rent reporting has little to no effect on the credit scores of participating renters with near-prime or better credit scores (Theodos, Teles, and Lieberman 2025; Chenven and Schulte 2015). Since consumers with high credit scores typically have thicker credit files, these findings are consistent with how the effect of rent reporting diminishes with the amount of traditional credit data a renter has.

-

8 Existing studies suggest that the share of renters who may be negatively affected by rent reporting via the age of accounts factor is likely to be small (Office of the New York City Comptroller 2017; Turner and Walker 2015).

-

9 Turner and Walker (2019) provide evidence that positive-only rent reporting can lead to sizeable improvements in credit scores even for renters with rent delinquencies.

-

10 Note, however, that not all renters with low credit scores have small quantities of traditional credit data; some may have large quantities of traditional credit data that accurately signal their low creditworthiness. Additionally, some renters with high credit scores may have a limited amount of traditional credit data.

-

11 All else equal, the lower a renter’s frequency of rent delinquencies, the larger the number of on-time rent payments that can be reported over any given period, and the larger the potential improvement in the renter’s credit score with positive-only reporting. Even with positive-only rent reporting, Renters who are frequently delinquent on rent payments may see little to no change in their credit scores.

Article Citation

Toh, Ying Lei. 2026. “Building Credit with Rent Data: The Potential Effects of Rent Reporting on the Credit Scores of U.S. Renters.” Federal Reserve Bank of Kansas City, Economic Review, vol. 111, no. 5. Available at External Linkhttps://doi.org/10.18651/ER/v111n5Toh

Publication information: Vol. 111, no. 5

DOI: 10.18651/ER/v111n5Toh

References

Blattner, Laura, and Scott Nelson. 2024. “How Costly Is Noise? Data and Disparities in Consumer Credit.” Working paper.

Board of Governors of the Federal Reserve System. 2025. “Alternative Data: Expanding Access to Credit.” Board of Governors of the Federal Reserve, Consumer & Community Context, October.

Chenven, Sarah, and Carolyn Schulte. 2015. “The Power of Rent Reporting Pilot: A Credit Building Strategy.” Credit Builders Alliance and Citi Foundation.

Hepinstall, Mike, Chaitra Chandrasekhar, Peter Carroll, Nick Dykstra, and Yigit Ulucay. 2022. “Financial Inclusion and Access to Credit.” Oliver Wyman, January.

Hermans, Amanda, Brett Theodos, and Daniel Teles. 2025. “An Overview of the Rent Reporting Landscape for State and Local Policymakers.” Urban Institute, November.

Office of the New York City Comptroller. 2017. “Making Rent Count: How NYC Tenants Can Lift Credit Scores and Save Money.” October.

Theodos, Brett, Daniel Teles, and Samuel Lieberman. 2025. “Evaluating Rent Reporting as a Pathway to Build Credit.” Urban Institute, June.

Toh, Ying Lei. 2023. “Addressing Traditional Credit Scores as a Barrier to Accessing Affordable Credit.” Federal Reserve Bank of Kansas City, Economic Review, vol. 108, no. 3, pp. 21–42. Available at External Linkhttps://doi.org/10.18651/ER/v108n3Toh

Turner, Michael, and Patrick Walker. 2019. “Potential Impacts of Credit Reporting Public Housing Rental Payment Data.” U.S. Department of Housing and Urban Development, October.

VantageScore. 2025. “Expanding Mortgage Access and Credit Score Predictive Power by Reporting Positive-Only Rental Payments.” VantageScore Solutions, November.

Wu, Chi Chi. 2024. “Even the Catch-22s Come with Catch-22s: Potential Harms and Drawbacks of Rent Reporting.” National Consumer Law Center, March.

Ying Lei Toh is an economist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author