Home prices in Nebraska have surged to all-time highs over the past two years alongside strong demand from buyers and a limited supply of homes available for sale. Demand for housing has been supported by sharp increases in household incomes, despite the pandemic, and several factors have limited the construction of new homes throughout the state. While the higher prices may be beneficial for current homeowners, the rapid increase in prices has intensified challenges of affordability for many low-income communities in the region.

Surging Home Prices

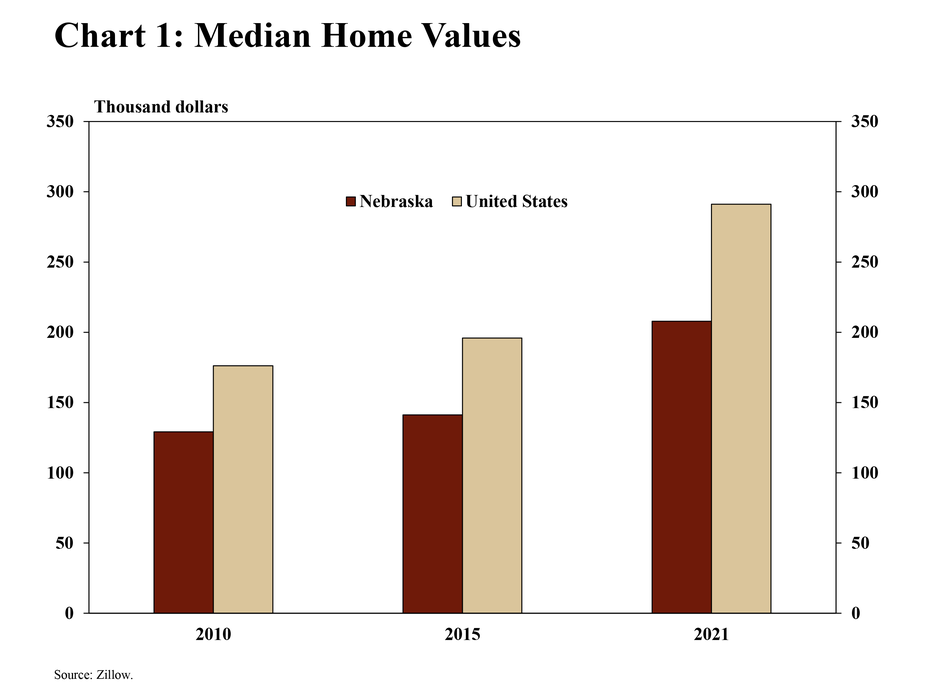

Home prices in both Nebraska and the United States increased sharply in 2021. From the beginning of 2020, through October 2021, the median value of single-family homes in Nebraska increased 26%._ By October 2021, home values in the state were about $67,000 higher than in 2015 and $79,000 higher than in 2010 (Chart 1). In March 2021, the median home value in Nebraska surpassed $200,000 for the first time. The surge in home prices has been similar nationally, although values in Nebraska have remained significantly less than the national average.

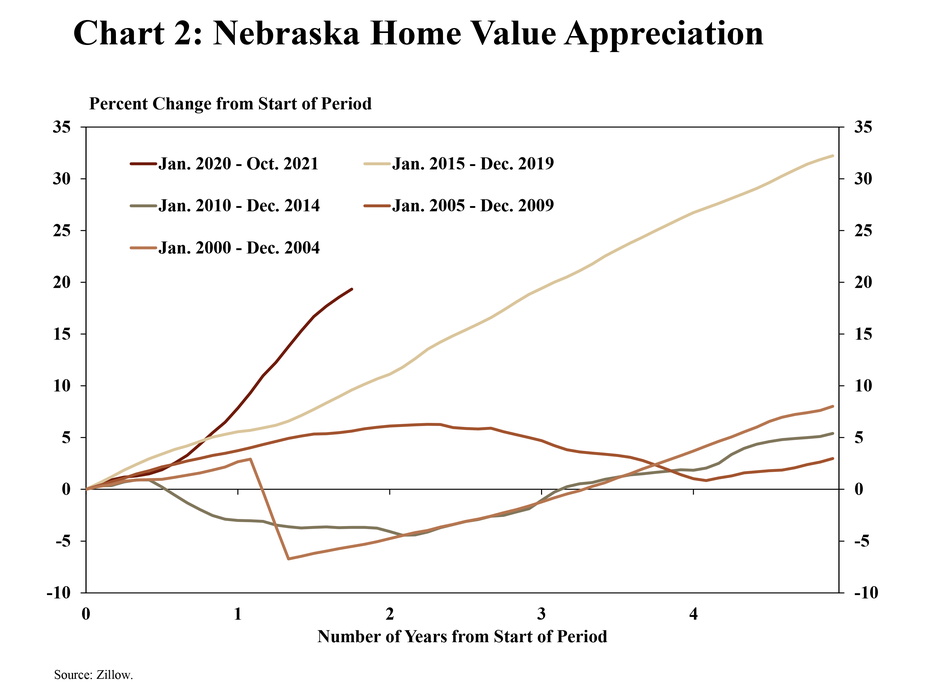

Since the pandemic started, home prices have risen much faster than in recent periods. The increase since the beginning of 2020 has been significantly higher than in any other five-year period since the turn of the century (Chart 2). In the five-year span following the 2007-09 recession, the housing market remained suppressed for several years. As the economic recovery from the Great Recession gained momentum, home prices also strengthened from 2015 to 2019. Even when considering the growth in home prices during the five years leading up to the pandemic, however, the increase from 2020 to the end of 2021 was substantial.

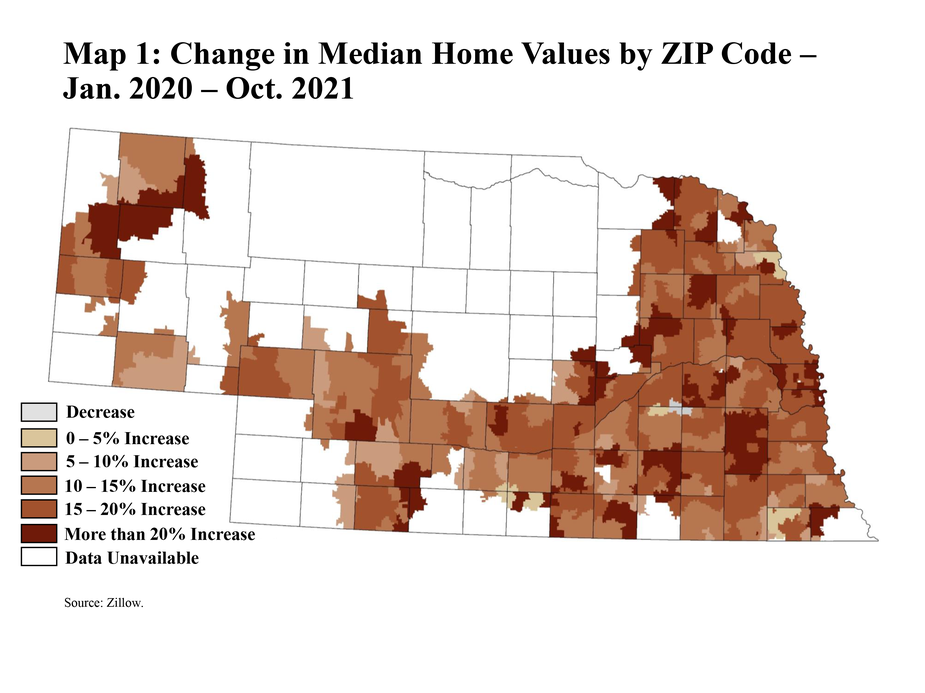

Across the state, the price of residential real estate accelerated in 2021. Home prices increased at least 5% in many locations from January 2020 through October 2021, including in many rural areas (Map 1). In Omaha and Lincoln (Douglas, Lancaster and Sarpy counties), home prices increased more than 10% in most communities. Even in parts of northwest and northeast Nebraska, home prices appreciated by more than 10%.

Strong Demand for Housing

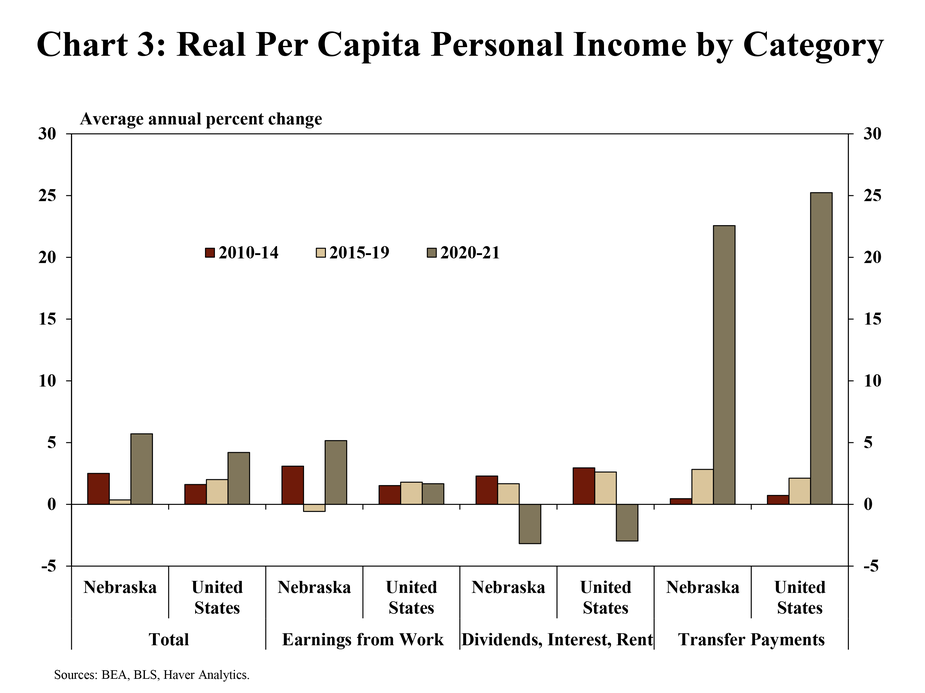

Despite the severity of the pandemic and recession in 2020, the demand for housing has been supported by significant gains in income. In the last two years, real per capita personal income in Nebraska increased almost 6%, more than in the prior two five-year periods (Chart 3). Government transfer payments accounted for a large share of these income gains. In fact, transfer payments increased an average of 20% over the previous year in Nebraska in 2020 and 2021. In comparison, transfer payments increased just by an average of about 3% between 2015 and 2019. More recently, increases in wages have also supported household incomes, which may have provided additional strength to the housing market.

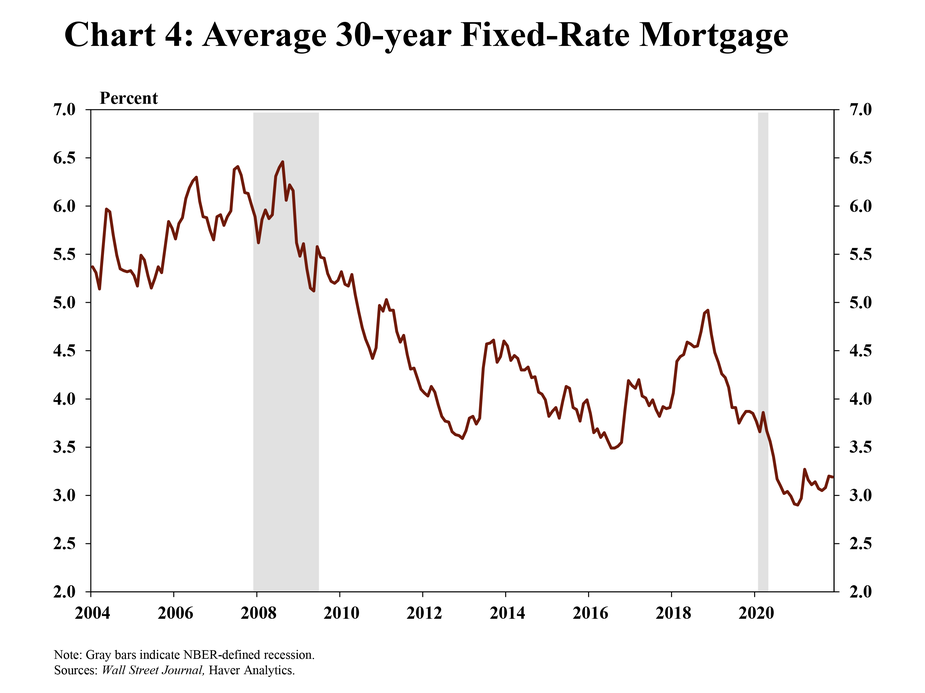

Historically low interest rates have also supported demand for new mortgages and housing. Prior to the pandemic, average interest rates for a fixed, 30-year mortgage had been holding steady at just under 4% (Chart 4). As the pandemic intensified in March 2020, mortgage rates dropped sharply alongside numerous monetary policy actions to provide accommodation to credit markets. Throughout 2021, 30-year mortgage rates remained just above 3%, a full percentage point less than before the pandemic.

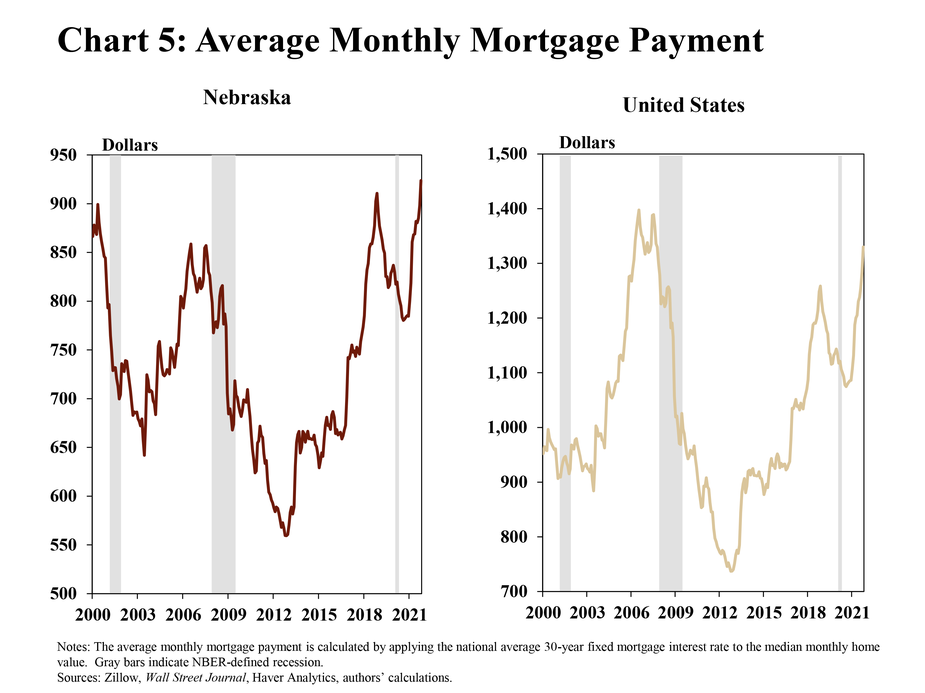

Although housing prices have increased sharply, favorable lending conditions have limited the increases in average mortgage payments, enabling some households to more easily afford higher-priced homes. Although average mortgage payments are considerably higher today than in the years following the 2007-09 recession, recent averages have been similar to the years before the pandemic. In Nebraska, the average monthly payment for a new mortgage in October 2021 was $924, the highest on record, but only a few dollars more than the previous peak in 2018 (Chart 5). Nationally, the average monthly mortgage payment has remained less than the peak that occurred prior to the Great Recession.

Supply Constraints

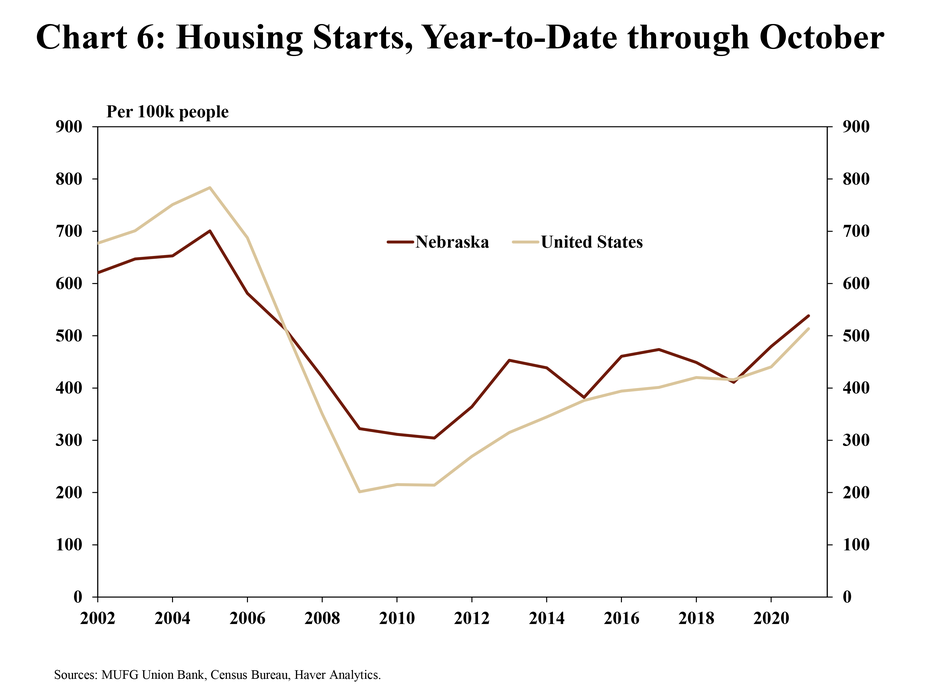

Increased home prices and strong demand have contributed to a modest increase in building activity. On a per capita basis, new home starts in Nebraska and the nation in recent years have trended higher (Chart 6). Despite the increase, housing starts in both Nebraska and the nation have remained less than the years leading up to the Great Recession.

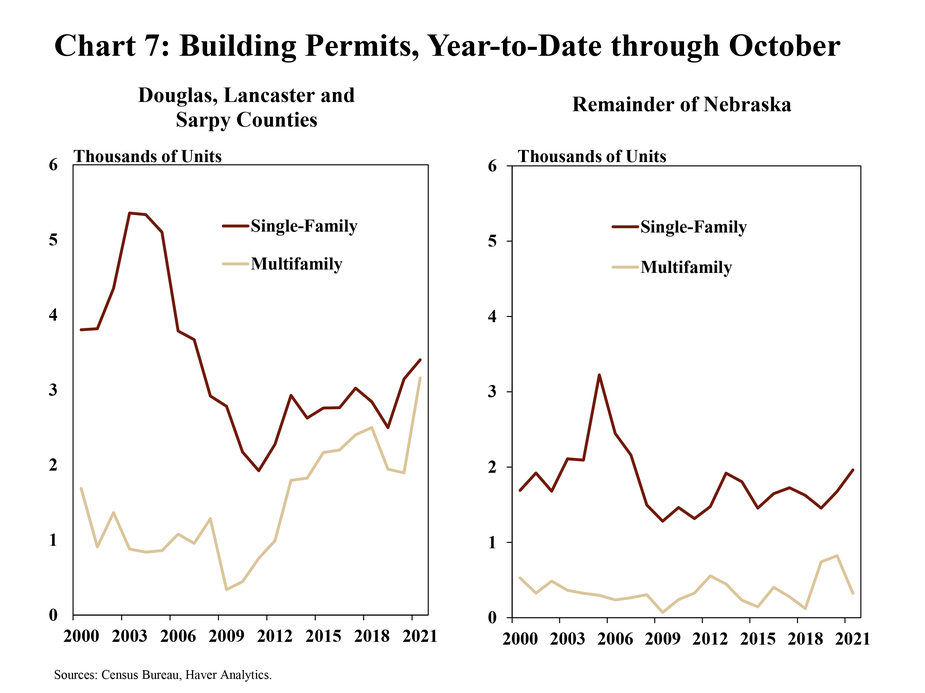

In addition to increased building activity, there have been recent signs of activity that may lead to future building. As of October 2021, permits to build single-family homes were at multiyear highs in Nebraska’s metro areas and other regions of the state (Chart 7). Supplementing the single-family housing supply, permits for multifamily units in the state’s largest cities have reached all-time highs.

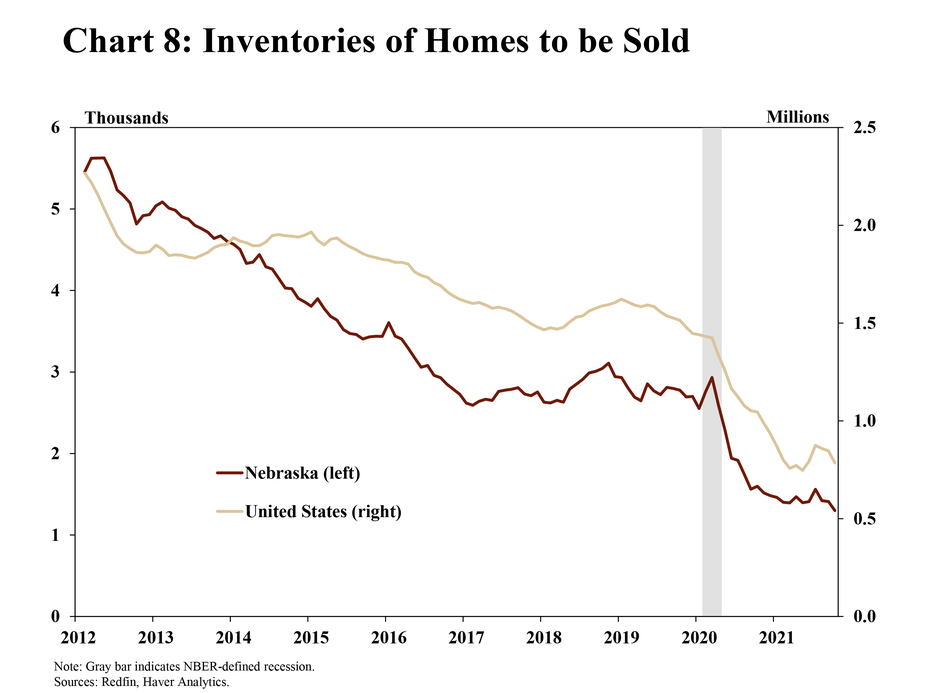

Despite the increased building activity, inventories of homes have remained depleted and have continued to dwindle. As of October 2021, inventories of homes for sale in Nebraska were at the lowest levels in at least a decade (Chart 8). Though construction has increased recently, demand for housing has steadily outpaced supply and building activity. Extremely low inventories of homes have been a primary factor of the recent surge in home prices in Nebraska, and in the nation more generally.

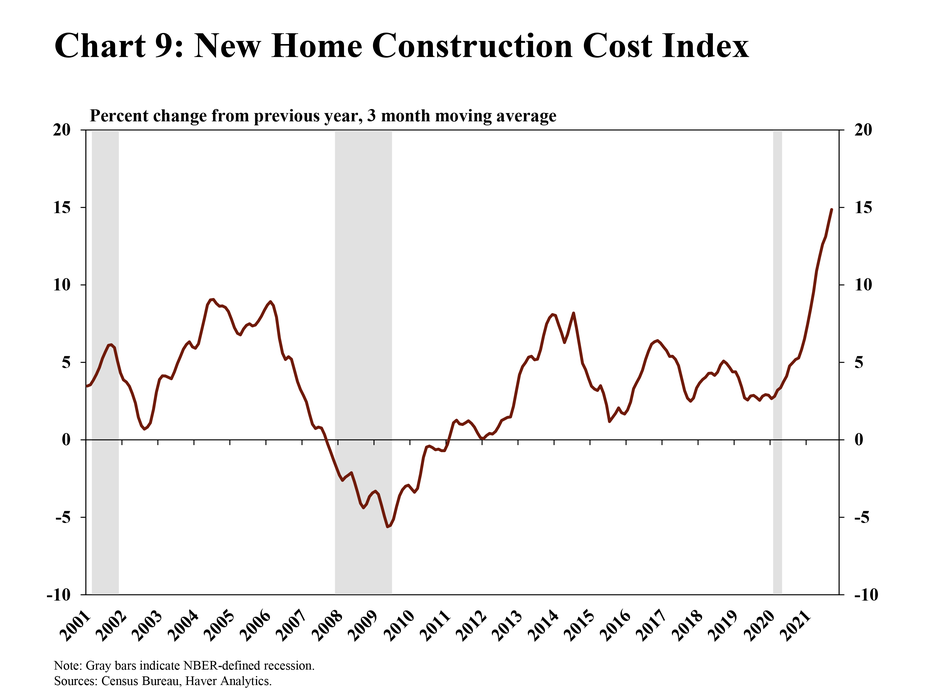

Increased costs and a lack of available lots have been notable factors limiting the construction of new homes. Home construction costs have generally been rising over the past decades, but in 2021 the cost to build a new home increased nearly 15%, the fastest increase in at least 20 years (Chart 9). Residential construction relies on many inputs, such as lumber, which have been difficult for builders and contractors to acquire during the pandemic. Costs for many of these items have also surged or have been especially volatile over the past two years. In addition, a record number of home builders have External Linkcited an extremely limited quantity of lots available for development as a factor constraining further building activity.

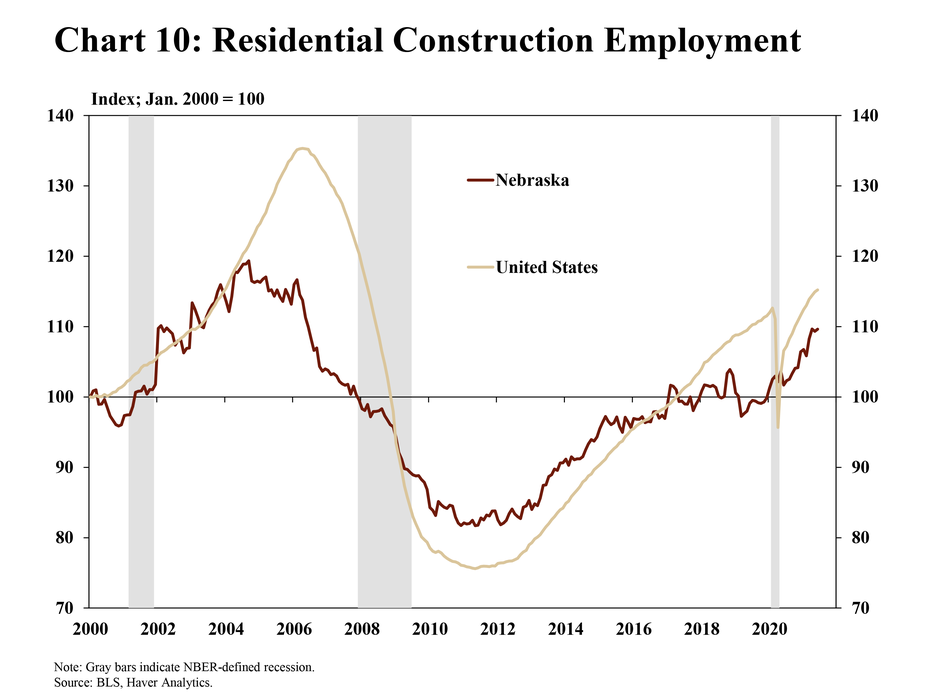

Labor shortages likely have also been a significant factor in restricting new home construction. Following the Great Recession and associated housing crisis, there was a sharp drop in the number of workers employed in the construction industry (Chart 10). Even as construction activity began to rebound during the economic recovery that ensued, the level of employment in the residential construction industry has increased more gradually. Only recently has the level of employment in Nebraska’s residential construction industry neared its pre-Great Recession peaks. As of June 2021, employment in residential construction was within 10% of its peak in 2004.

Challenges of Affordability

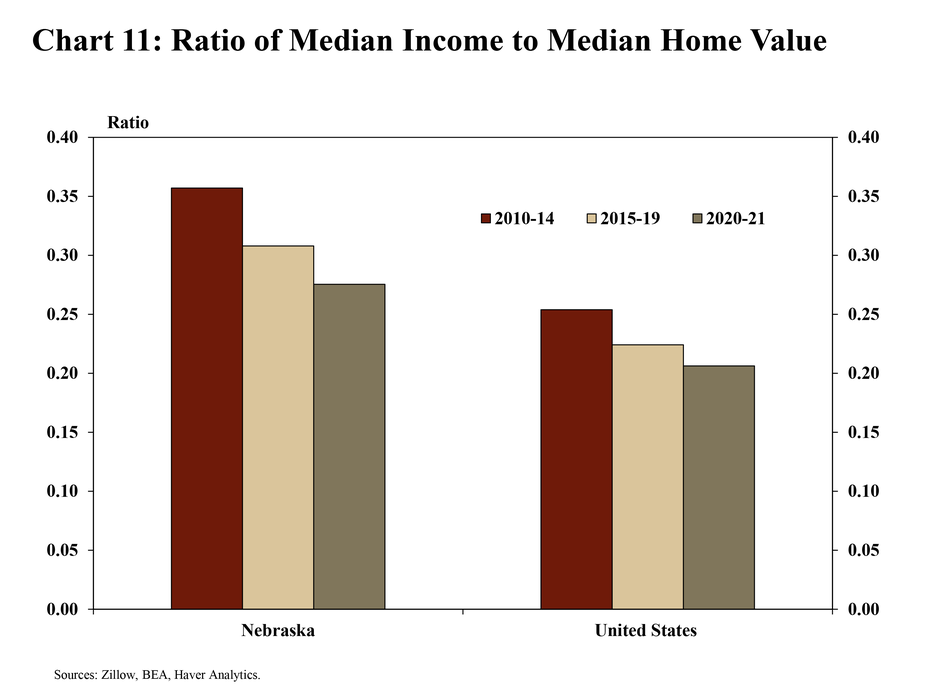

Although incomes have increased throughout the pandemic, home prices have increased notably faster. In 2020 and 2021, the ratio of income to home values declined to 0.28, on average (Chart 11). This ratio of income to home values has declined over the past decade, suggesting that homes have become even more expensive relative to household financial resources. Although home prices have risen rapidly during the pandemic in both Nebraska and the nation, homes are generally still more affordable in Nebraska compared with the U.S. average.

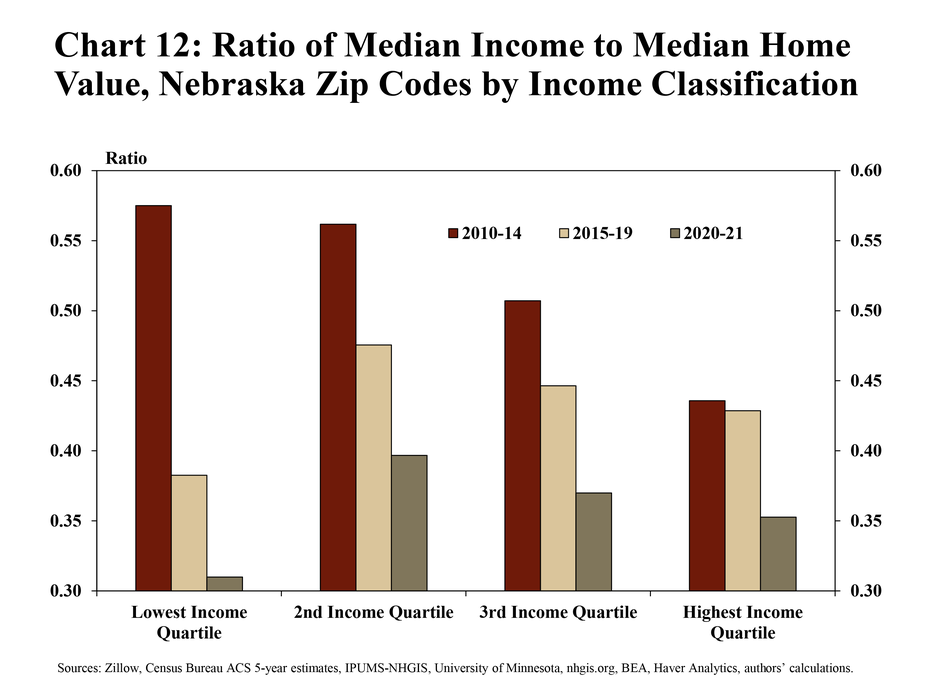

Relative to incomes, the increase in home values has been especially sharp in low-income communities, underscoring challenges of home ownership in these areas. At a local (ZIP code) level, home prices have grown most quickly relative to incomes in low-income communities (Chart 12). Compared with a decade ago, the ratio of income to home prices for the lowest-income communities dropped from almost 0.60 to nearly 0.30. In contrast, in the highest-income communities, this ratio decreased by a much smaller amount, from 0.44 to 0.35.

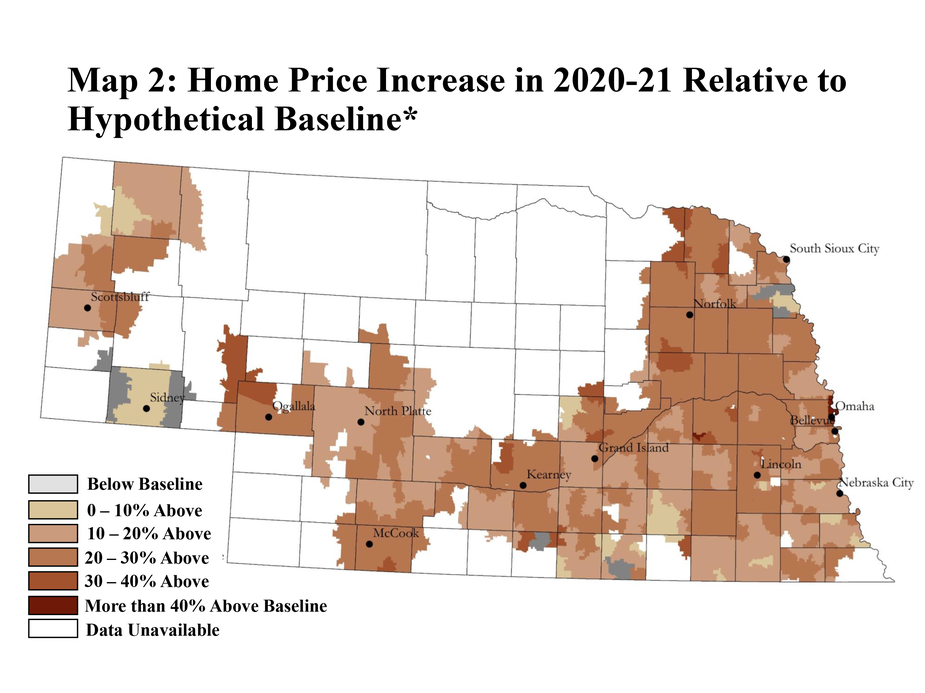

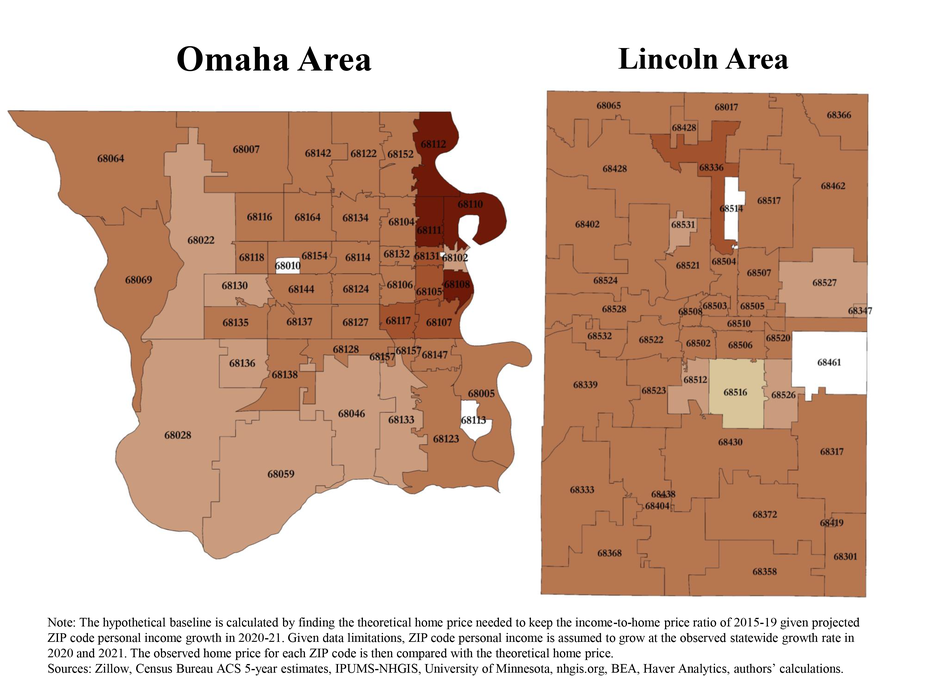

More specifically, the challenges of housing affordability have intensified most significantly in North Omaha and South Omaha since the onset of the pandemic. Compared with a baseline scenario, home prices increased more than 40% in four communities in North and South Omaha (Map 2 and 2a)._ In fact, by the end of 2021, home prices had increased about 30% over the baseline for many areas east of 72nd Street in Douglas County, leading to much lower home affordability compared with the years prior to the pandemic.

Conclusion

The COVID-19 pandemic has resulted in numerous market disruptions and significant changes, including in the housing market. Alongside low unemployment, increasing wages and a relatively strong outlook for Nebraska households, demand for homes in Nebraska appears likely to remain stable in the year ahead. If housing demand remains steady in 2022, the pace of home construction and associated costs will be key determinants of the price and affordability of housing in the state.

Endnotes

-

1 Throughout this article and in corresponding charts, the terms “price” and “value” are used interchangeably for ease of exposition.

-

2 The hypothetical baseline is calculated by finding the theoretical home price needed to keep the income-to-home price ratio of 2015-19 given projected ZIP code personal income growth in 2020-21. Given data limitations, ZIP code personal income is assumed to grow at the observed statewide growth rate in 2020 and 2021. The observed home price for each ZIP code is then compared with the theoretical home price.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy