The U.S. labor market is historically tight. Businesses point to broad difficulties in attracting applicants, hiring qualified candidates and retaining their existing workforce. These staffing difficulties are set against a backdrop of greater availability of remote work opportunities, which many workers have sought either at their current job or from new employers. In greater waves than ever before, workers are seeking such opportunities from new employers or in new sectors. More workers quit their jobs over the past 18 months compared to any time in the last 20 years during an episode now known as the “The Great Resignation.” In this edition of the Rocky Mountain Economist, we show that worker quit rates grew faster in industries where the possibility of working remotely is less common. With elevated quit rates, employers needed to compete with higher wages to fill an outsized number of job vacancies. The additional acceleration of quit rates in industries with few remote work opportunities led to even faster wage growth over the past year and a half. Higher worker turnover also means greater challenges onboarding workers. The excess training and recruiting efforts needed where quits rates are high may be hindering productivity growth, as sectors with few remote options and higher quits rates suffered productivity losses recently. Employers currently seem to be paying a premium to bring workers on site both in terms of wages and in terms of actual worker output.

Replacing Workers that Quit Their Job Often Requires Higher Wages

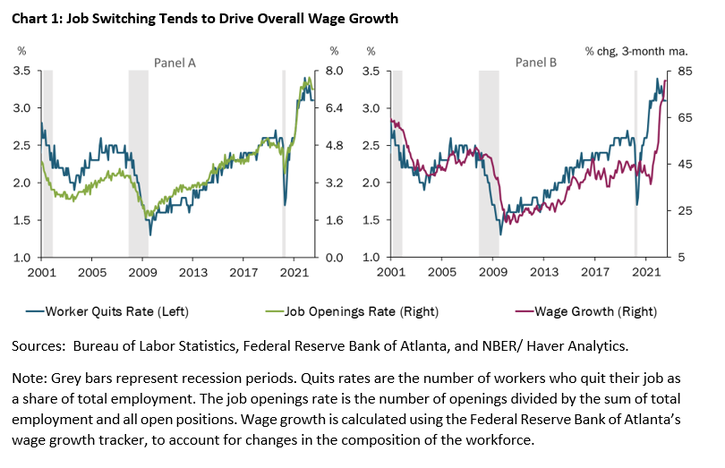

As workers switch from one job to another they leave behind a vacancy that employers must fill. When worker quits rates are elevated, employers are left with many more openings, leading them to raise posted wages to attract quality applicants. This intuitive connection between worker quit rates, job openings, and subsequent wage growth is shown for the U.S. economy in Chart 1. Over the past 20 years, periods of high worker turnover rates are accompanied by an increase in job openings (Panel A) followed by a rise in wage growth (Panel B). Similarly, slower wage growth coincides with subdued worker turnover rates and fewer job openings.

Beginning in January 2021, workers began to leave their jobs in droves. Quits rates accelerated throughout the past 18 months as workers sought employment opportunities that better suited their lifestyle or preferred work environment, a pandemic-induced phenomenon referred to as the Great Resignation. Job openings also increased rapidly, and employers offered better compensation to attract applicants as these job openings persisted. Broad-based wage growth soon followed and remains elevated even as turnover rates have begun to moderate.

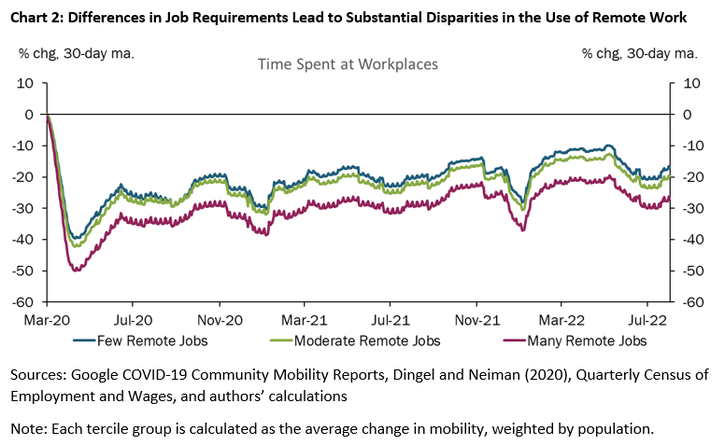

Workers have demonstrated an appetite for working remotely. Chart 2 shows the amount of time workers spent at their job site over the past couple of years based on Google Mobility metrics. Workers are currently spending between 15 to 30 percent less time working on site compared to before the pandemic, even as public health concerns have stabilized. Not surprisingly, some occupations are better suited to accommodate remote employees than others. For example, jobs that rely heavily on technology infrastructure to accomplish tasks are more apt to virtual work environments. Conversely, jobs in manufacturing, and service oriented jobs that require frequent in-person customer interaction are less likely to be performed remotely.

As shown in Chart 2, workers in locations with plentiful remote opportunities are spending approximately 10 percent more of their pre-pandemic work week at home compared to counties where remote work is less prevalent. We linked data measuring the share of employment within major industries that have a potential for remote work from Dingel and Neiman with county-level shares of industry employment from the Quarterly Census of Employment and Wages (QCEW) to measure the potential for remote work across different U.S. counties. Each county is classified as a having many, moderate, or few remote work opportunities for residents. These classifications represent different equally-sized terciles based on the observed shares of employment amenable to remote work.

Considering a 40-hour work week, an additional 10 percent of time workers are remote amounts to roughly 2 more work days offsite per month for each worker where remote work is most available. The ebbs and flows of worker mobility patterns were closely tied to the waves of COVID-19 in 2020 and 2021. However, in recent months, the stark decline in time workers spent at their job site coincided with a sudden rise in gas prices that affected the costs of commuting to work. The use of remote work now seems to respond to economic conditions, even as public safety concerns have stabilized. Altogether, the use of remote work is both prevalent enough and persistent enough to create substantial challenges for employers as they seek to attract, retain, and enable an effective workforce.

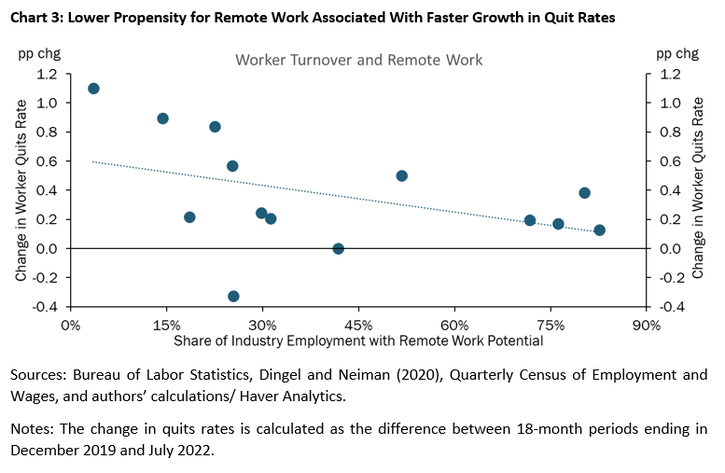

Workers More Likely to Quit Jobs Where Remote Work Is Less Available

Worker retention indeed proved more difficult for employers that could not offer remote opportunities to staff over the last 18 months. Chart 3 shows each major industry’s share of remote work potential and its corresponding change in the rate workers quit their jobs over the last 18 months. From the beginning of 2021 through the middle of 2022 the percentage of workers that quit their job surged in all industries, but increased by approximately 15 basis points more in the sectors where less than half of the workforce had remote work capability. Accordingly, job posting rates increased more in industries less suited to accommodating remote workers – such as accommodation and food services, and manufacturing – to backfill the excess churn in the labor force. The flexibility afforded by remote work environments may have dissuaded some workers in industries with more remote wok capability from seeking new positions, as employers in industries such as financial services and information technology experienced relatively lower growth in worker turnover rates.

Worker Quits Drive Wage Growth Up Faster Where Remote Work is Less Available

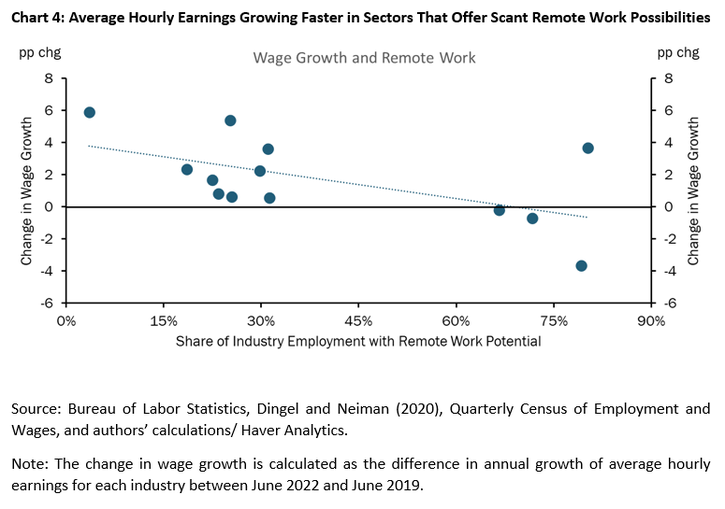

In response to accelerated rates of job turnover, employers in sectors most affected by higher quits relied on wage increases to attract more workers. The value that job seekers placed on the ability to work from home was reflected in faster wage growth employers needed to offer to try to fill onsite positions. Chart 4 plots the acceleration of wage growth across major industries based on the availability of remote work. The additional tightening that pinched employers that cannot offer remote options, led to roughly 3 percentage points faster wage growth than observed in sectors with many remote work opportunities. Wage growth accelerated faster for industries with few remote work opportunities – namely, hospitality and healthcare workers – as compared to workers in financial services and information sectors – industries that actually experienced decelerations in wage growth. This differential points to the premium employers are paying to bring workers on site.

Drags on Productivity To Train Replacement Hires Exacerbated Costs of Wage Growth

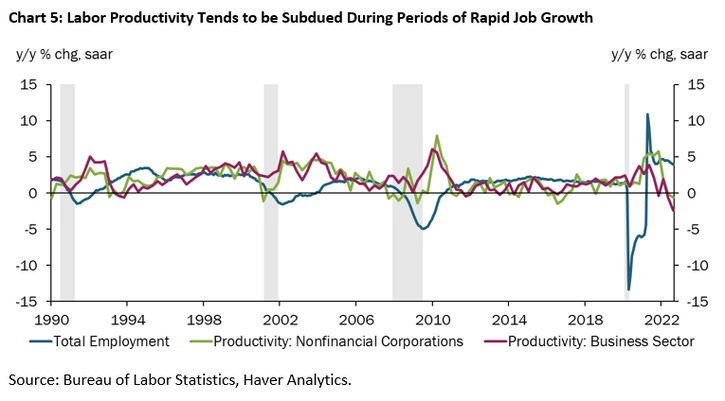

The challenges of attracting and retaining workers seem to go beyond outsized wage pressures as labor productivity has dragged in sectors where worker turnover has been high and remote work is rare. Worker productivity growth – measured as real output per hour worked – tends to decline as employment recovers coming out of recession periods. As seen in Chart 5, during the early 1990s, the early 2000s, following the global financial crisis, and at the onset of the pandemic, employment declined in the wake of recessionary periods. Then, as job losses slowed and employment subsequently begins to recover, overall productivity growth tends to decline temporarily. In other words, productivity growth typically faces headwinds during periods of rapid hiring.

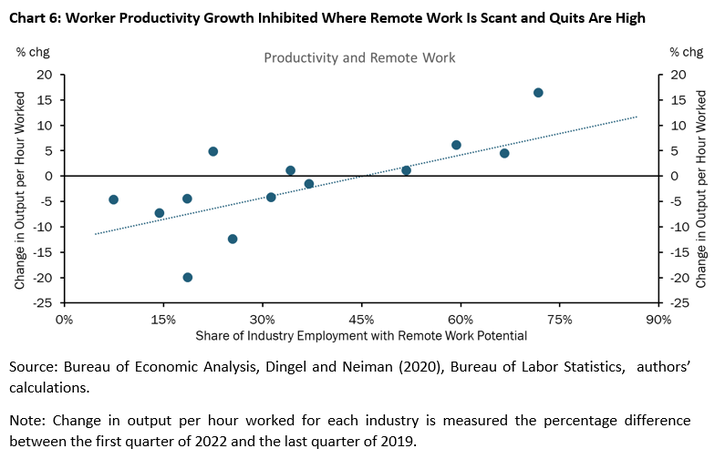

The headwinds to productivity growth have been more prominent for employers that cannot offer as many remote work opportunities and have faced higher worker quits rates. Onboarding and training such a large number of replacement workers takes time, which drags productivity down during periods of rapid hiring. The potential losses associated with being understaffed may have also led some employers to hire workers with less skill or experience than those that quit. In either case, Chart 6 shows that worker productivity growth, measured as change in total industry GDP per hours worked, was suppressed in industries that face higher turnover and offer fewer remote options. For example, industries such as hospitality and food services, where employers lost the most workers and struggled to fill open positions, suffered productivity losses over the past few years. Labor productivity declined in these sectors with few remote work opportunities by an average of 5 percentage points over the past few years. Conversely, industries that retained their workers somewhat better during this period of rapid job turnover, such as information and professional and business services, experienced labor productivity gains, rising 7 percentage points overall.

Looking Ahead

Altogether, the inability to offer remote work has been associated with higher quits rates and job vacancies, faster wage growth, and losses in worker productivity over the past year and a half. A key question that remains is how persistent any influence of remote work on labor market outcomes will be going forward. If the productivity losses experienced where remote work is less common are due to the challenge of onboarding and recruiting a large number of workers, then the productivity drag of the Great Resignation may prove to be temporary as new hires gain experience. However, if employers that need their staff on site recruited workers with lower skill levels, as higher skilled workers sought remote opportunities, then disparities in labor productivity across sectors may prove more persistent. In either case, the tight link between worker turnover levels and the availability of remote work obfuscates the potential productivity benefits of remote work; some of the apparent growth in remote worker productivity may be attributable to labor market dynamics that influenced worker efficiency, rather than being solely due to technologies that enable work from home.

Interested in learning more about the economics of where you work? Click here.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Bethany Greene

Research Associate II