Commercial banks reported a decline in farm lending activity during the second quarter of 2026. According to the Survey of Terms of Lending to Farmers, new loan originations declined for nearly all non-real estate loan purposes. Loan volumes declined alongside smaller loan sizes at banks with larger farm portfolios, and smaller loan sizes for operating expenses and non-feeder livestock. Meanwhile, farm loan interest rates remained stable across loan sizes compared to the previous quarter, although rates continued to exceed historical norms.

Energy and fertilizer prices fell by the end of May and reduced operating costs for some U.S. farmers. However, crop farmers’ profit margins remained tight as domestic agricultural prices also declined alongside reduced oil prices. Providing ongoing support to the agricultural economy, cattle prices remained high in the second quarter real estate values were still near record highs in key agricultural regions.

Second Quarter National Survey of Terms of Lending to Farmers

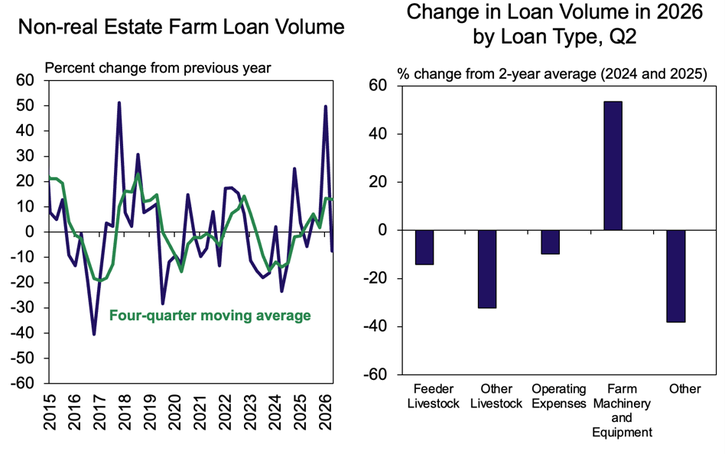

Non-real estate agricultural loan volumes at commercial banks contracted from the previous quarter and were slightly lower than averages of recent years. The effects of seasonality led to a pronounced decline in the volume of non-real estate loans from the previous quarter, and a more moderate decline of 10% from the averages of the last two years (Chart 1, left panel). Lending volumes declined for most loan purposes, with the exception of farm machinery and equipment loans, which increased by more than 50% from recent years (Chart 1, right panel).

Chart 1: Volume of Non-Real Estate Farm Loans

Sources: Survey of Terms of Lending to Farmers and Federal Reserve Bank of Kansas City

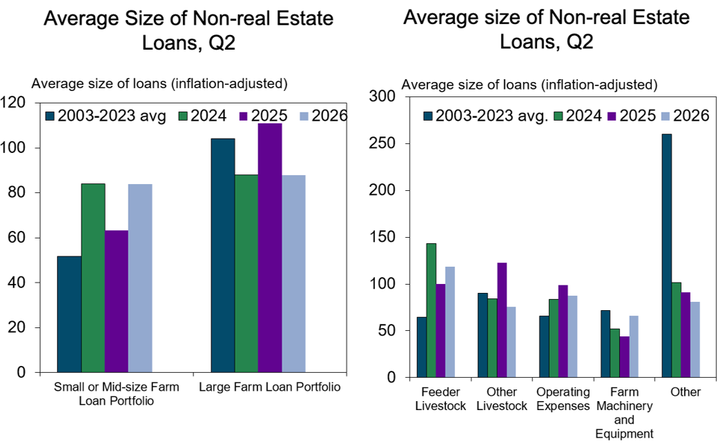

Across banks, average loan sizes returned to second-quarter 2024 levels, but the adjustment varied by loan type. Banks with small or mid-sized farm loan portfolios increased loan sizes by more than 30% from a year ago, nearing 2024 levels but exceeding historical averages (Chart 2, left panel). In contrast, loan sizes at commercial banks with large farm loan portfolios declined by 20% from last year to levels below historical averages. Loans used to finance feeder livestock and operating expenses remained above historical levels, while the loans for other purposes were more subdued (Chart 2, right panel).

Chart 2: Non-real Estate Farm Loan Size, Q2

Sources: Survey of Terms of Lending to Farmers and Federal Reserve Bank of Kansas City

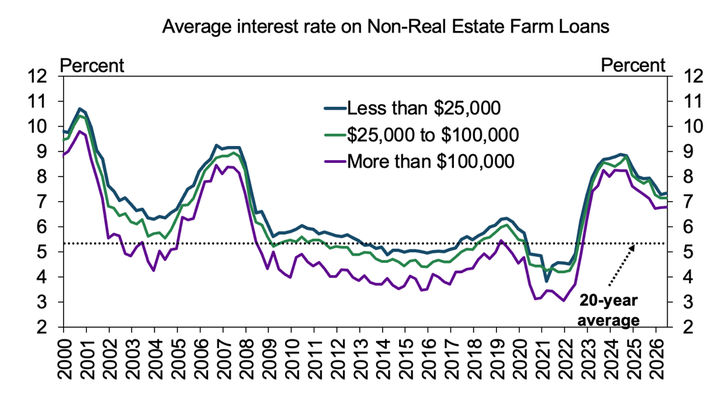

Interest rates remained mostly stable during the second quarter of 2026. The average rate on loans greater than $100,000 was slightly less than 7%, and nearly unchanged from the previous quarter (Chart 3). Average rates on loans of smaller sizes remained slightly above 7% and were similar to previous quarters.

Chart 3: Average Interest Rate on Non-Real Estate Farm Loans by Loan Size

Sources: Survey of Terms of Lending to Farmers and Federal Reserve Bank of Kansas City

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Data Tables

External LinkAbout National Survey of Terms of Lending to Farmers Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author