Relationship Between Unrealized Gains and Losses and Tangible Equity Capital Ratio

Source: Reports of Condition and Income

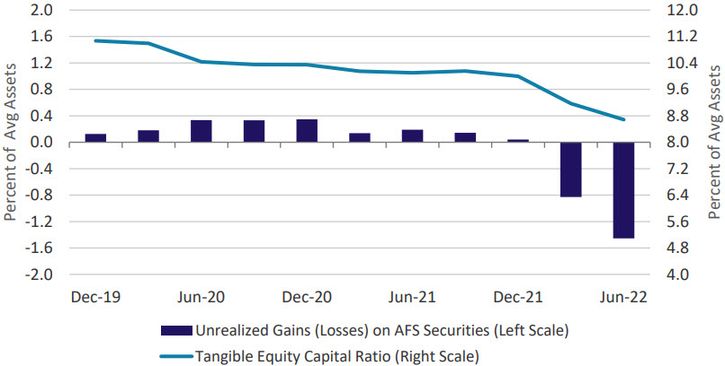

- Due to the increasing rate environment, securities that were purchased when the market dictated lower yields have become less desirable to investors resulting in declining valuations. Accounting standards require that changes in available-for-sale (AFS) securities valuations be reflected through accumulated other comprehensive income, thereby resulting in growing unrealized loss positions within community banking organization (CBO) AFS portfolios; these values are not typically reflected within CBO regulatory capital ratios.

- Tangible equity capital, a non-regulatory capital measure, defined as total equity capital, including other comprehensive income less goodwill and other intangible assets, can be useful in measuring financial strength since unrealized loss positions make these assets a much less attractive source of liquidity. Moreover, parent company equity is impacted by unrealized losses at the bank-level, potentially hindering its ability to serve as a source of strength.

- At June 30, 2022, the Tangible Equity Capital Ratio at CBOs fell to 8.7 percent as a result of mounting unrealized losses on AFS securities, which totaled 1.5 percent of average assets. At year-end 2021, only 4 community banks had tangible equity capital ratios below 5 percent; that number increased to 333 at June 30, 2022, indicating less ability to sustain economic shocks.

Questions or comments? Please contact KC.SRM.SRA.CommunityBankingBulletin@kc.frb.org.

*Community banking organizations are defined as having $10 billion or less in total assets

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.