Provision Activity and Allowance Level in Relation to Problem Loan Volume

Source: Reports of Condition and Income

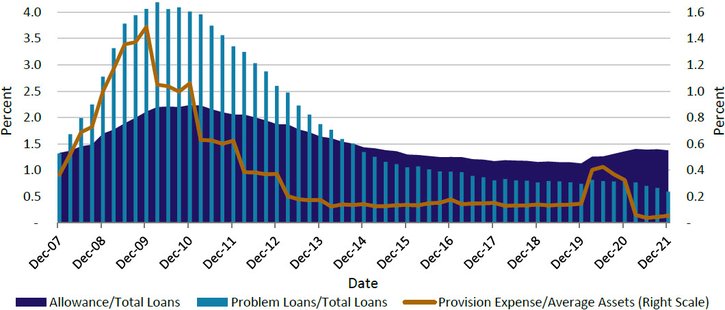

At the onset of the pandemic, banks boosted allowance levels through provisioning in anticipation of potential deterioration in loan portfolios. However, as the level of past due and nonaccrual loans remained low, banks pulled back provisions with allowance balances now declining towards pre-pandemic levels.

- Community banking organizations_ (CBOs) entered the pandemic with allowance levels as a percent of total loans at the lowest level since 1982. However, strong provisioning amidst economic uncertainty at the onset of the pandemic boosted allowance levels to a peak of 1.40 percent of total loans in mid-2021, up from the 37-year low of 1.13 percent at year-end 2019.

- The volume of problem loans remains low across all major lending types and has been supported by pandemic-induced government programs and relief efforts. As such, banks have reduced or reversed provision expenses. Throughout 2021, 12 percent of CBOs recognized reverse provisions, a historic high, with total provision expenses of only 0.06 percent of average assets at year-end, a historic low.

- While past due and nonaccrual balances remained low throughout the pandemic, loans that have been restructured or modified under Section 4013 of the CARES Act are not captured in problem asset levels though carry the potential to present asset quality concerns. Allowance levels have been directionally consistent with credit quality concerns, including the volume of Section 4013 loans, which accounted for 11 percent of total loans at CBOs when first implemented but have since declined to 1.3 percent.

Questions or comments? Please contact KC.SRM.SRA.CommunityBankingBulletin@kc.frb.org.

Endnotes

-

1 Community banking organizations are defined as having $10 billion or less in total assets.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.