Economic conditions for low- and moderate-income (LMI) communities in the Tenth District of the Federal Reserve System continue to recover from the pandemic recession. LMI communities appear to be facing continued stress across many factors due to the persistence of COVID-19. While there are some differences in the economic conditions between states, the Tenth District overall does not differ much from the conditions experienced nationally.

For this report, I used responses to the most recent External LinkPerspectives from Main Street COVID-19 survey by the Federal Reserve as well as supporting data from other sources to provide an overall perspective of the conditions affecting LMI communities in the Tenth District. The Federal Reserve Bank of Kansas City represents the Tenth District of the Federal Reserve System which covers seven states: Colorado, Kansas, western Missouri, Nebraska, northern New Mexico, Oklahoma and Wyoming.

The COVID-19 survey was sent to nonprofit organizations, financial institutions, government agencies and other community organizations across the U.S. This report only focuses on responses representing the Tenth District. See the methodology section at the end of the report for more information.

Overview

- Economic conditions are improving compared with conditions during the peak period of distress.

- 4% fewer LMI people were employed in September 2021 than in January 2020.

- COVID-19 is still a significant disruption to financial stability, small businesses, services for children and housing stability.

- COVID-19 is still causing some disruption to access to health care and access to basic consumer needs.

- New Mexico appears to be currently experiencing the most impact from COVID-19.

- Oklahoma and Wyoming appear to be currently experiencing the least impact from COVID-19.

- LMI economic conditions appear strongly related to the recovery of leisure and hospitality jobs.

- Most jurisdictions in the Tenth District spent more than half of their first round of Emergency Rental Assistance (ERA1), but only Douglas County, CO and Kansas City, MO have spent all of it.

- About 15% of LMI renters still report being behind on rent.

- Over 25% of LMI renters in Oklahoma reported they were behind on rent while ERA1 spending across the state was second highest in the District.

Economic Conditions

In general, the economic conditions in LMI communities have improved, but there were still significant disruptions due to COVID-19. Nearly all respondents reported COVID-19 was currently having at least some disruption on economic conditions. The share of respondents saying there was a significant disruption decreased from 88% at the peak to 48% currently (Chart 1). However, in New Mexico, 65% of respondents still report significant disruptions caused by COVID-19.

In general, the economic conditions in LMI communities have improved, but there were still significant disruptions due to COVID-19. Nearly all respondents reported COVID-19 was currently having at least some disruption on economic conditions. The share of respondents saying there was a significant disruption decreased from 88% at the peak to 48% currently (Chart 1). However, in New Mexico, 65% of respondents still report significant disruptions caused by COVID-19.

Chart 1: COVID-19 Disruption on Economic Conditions – Tenth District

Source: Federal Reserve, Perspectives from Main Street Survey COVID-19 Survey

Employment

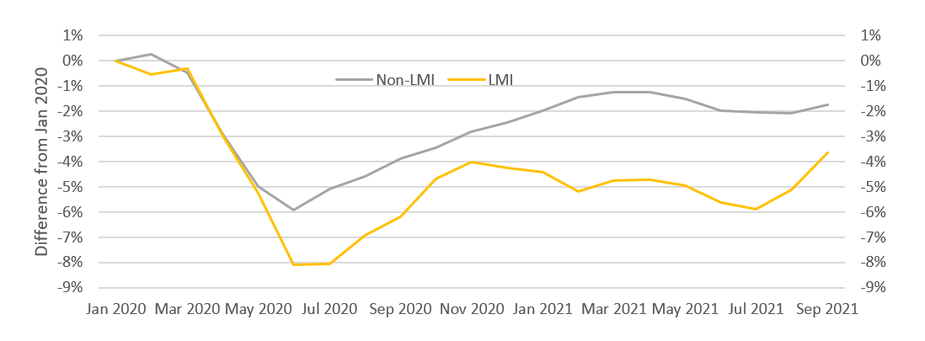

As shown in Chart 2, LMI populations experienced more relative job loss than non-LMI populations. This was largely due to their high employment concentration in jobs that could not be done from home and in industries that were hard hit by the pandemic. Since the peak of the recession, LMI populations have recovered a little more than half of their employment losses. But their recovery has lagged that of non-LMI populations. About 4% fewer LMI people were employed in September 2021 than in January 2020. Non-LMI employment is less than 2% lower than pre-pandemic.

Chart 2: Employment-to-Population Ratio (EPR) of LMI workers - Tenth District

Notes: Employment population ratio is calculated only for the working-aged population, ages 25-64. A worker is classified as LMI if their reported family income was less than $50,000, which approximates 80% of the District median income. This figure was used for ease of understanding and may differ from analyses that use localized area median income calculations.

Source: Current Population Survey PUMS; University of Minnesota, www.ipums.org

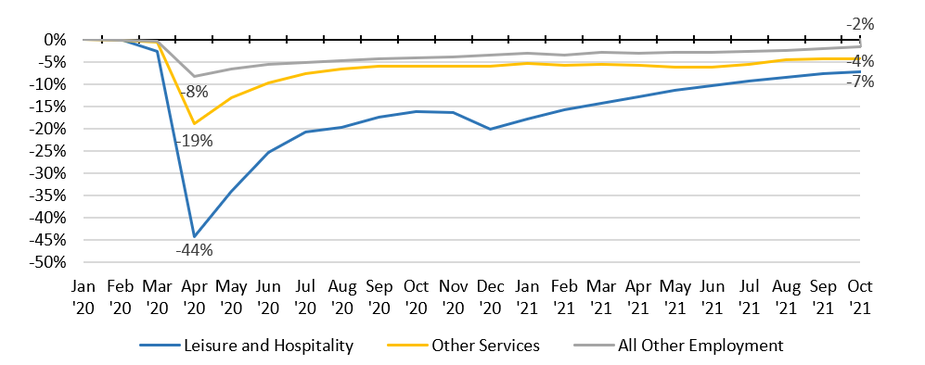

Employment by industry showed that the industries most impacted by the pandemic-induced recession have struggled to fully recover (Chart 3). Leisure and hospitality employment especially has struggled to recover. While restaurant jobs are still not back to January 2020 levels, tourism-related jobs have been much slower to come back. COVID still presents a threat to those jobs.

Chart 3: Leisure and Hospitality Employment Lagging in the Recovery

Note: Data includes the full states of Missouri and New Mexico.

Source: Bureau of Labor Statistics/Haver Analytics

Financial Stability

COVID is causing significant disruptions to financial stability, according to most respondents. Continued impacts on financial stability may mean respondents are still seeing many people experiencing job loss, irregular employment, or other income disruptions.

Respondents in Oklahoma and Wyoming reported lower levels of disruption than other states. Respondents for those states reported lower levels of stress across all topics in the survey. This suggested those states may be further along in recovery than other states in the District. I explain this more in the discussion section.

Small Businesses

About a third of organizations either did not answer the question about small businesses or said they were unsure, the highest rate for any of the primary survey questions. When only looking at organizations that were sure about the conditions of small businesses, 70% said there were significant disruptions to small businesses. The high share at the District level was heavily weighted by responses from New Mexico, where nearly 80% of respondents said COVID was causing a significant disruption. It is difficult to know for sure what impact COVID-19 is continuing to have on small businesses from the structure of the survey. But responses may have been motivated by labor shortages, supply chain issues and continued public hesitancy about in-person activities, which may impact their sales.

Housing

Housing stability is also significantly disrupted by COVID. Only Oklahoma had fewer than half of respondents say housing stability was significantly disrupted by COVID. Meanwhile, 70% of respondents in Missouri said COVID was a significant disruptor to housing stability.

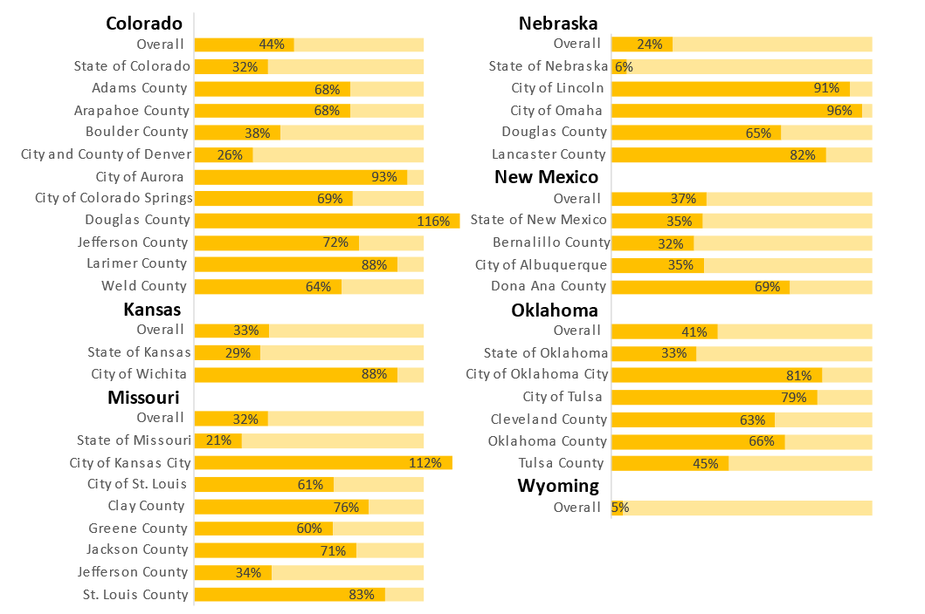

Responses to housing stability were likely linked to the ongoing stress for renters. Congress passed two rounds of Emergency Rental Assistance (ERA1 and ERA2). Every state in the District still has over half their ERA1 funds available. Through Oct. 31, 2021, only two jurisdictions in the Tenth District had spent 100% of their ERA1 funds – Douglas County, CO. and Kansas City, MO. (Chart 4).

According to the Census Household Pulse survey for September, there is still a considerable need to address rent payments._ About 15% of Tenth District LMI renters stated they were behind on rent._ However, over 25% of LMI renters in Oklahoma said they were behind on rent.

Oklahoma’s renter distress is highest even though their ERA spending is second highest in the District. Overall, Oklahoma had spent 41% of its ERA1 funds by the end of October. This was led by cities and counties who spent down 71% of their collective ERA1 funds. Based on the ERA1 spending, it makes sense that Oklahoma respondents would report lower levels of disruption. However, it is unclear why this was contradicted by the Household Pulse data.

Chart 4: Emergency Rental Assistance (ERA1) Spending through Oct. 31, 2021

Source: U.S. Treasury

Basic Consumer Needs

The component of the survey with the most positive response was for access to basic consumer needs. Most respondents reported only some disruptions on people being able to access food, household essentials and other personal needs in their communities. While inflation and supply chain issues have affected many segments of the economy, it was unclear whether respondents were seeing these issues in their communities or factoring it into their understanding of “access.”

Discussion

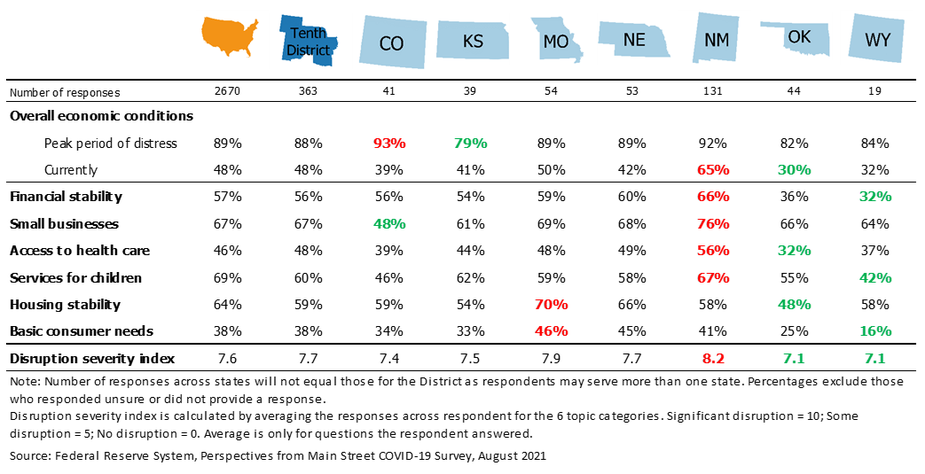

Overall, there is evidence that LMI communities across the District are recovering from the pandemic-induced recession, but COVID-19 continues to have a significant impact on many areas of their lives. New Mexico in particular seemed to have the most struggles (Table 1). Employment struggles are likely to continue while COVID-19 remains a significant threat. Housing struggles are likely related to continued financial disruption and slow dispersal of Emergency Rental Assistance funds. And small businesses are likely to face continued disruptions as COVID effects supply chains, labor and demand for services.

Based on the disruption severity index I calculated, Oklahoma and Wyoming appear to be doing much better than the rest of the District (Table 1). This seemed to relate a lot to where each state was in the recovery of their leisure and hospitality industry sector. Oklahoma and Wyoming have recovered the most employment in leisure and hospitality (down 5% and 4% from January 2020, respectively). New Mexico and Missouri lag the most (both are down 10% from January 2020). No other industry sector had as strong a relationship to the sentiments expressed in the survey. Considering the very high concentration of LMI employment in leisure and hospitality jobs, it is not surprising that there is a strong relationship there. But it does highlight the importance of that industry’s recovery in the recovery of LMI communities.

Table 1: Percent Reporting Significant Disruptions due to COVID-19

Methodology Note

The survey was administered between Aug. 3 and Aug. 27, 2021. After cleaning the data, there were 3,681 responses to the survey at the national level. While the national analysis included respondents who said their organizations did not primarily serve LMI populations or were not direct service providers, I did not include them in my analysis. Excluding them, the national sample was 2,670 responses. Respondents could report COVID-19 was causing significant, some, or no disruption for the questions analyzed here.

Tenth District responses were selected based on the respondent stating they worked in a Tenth District state, other states they represented were contiguous to Tenth District states, and they were not a nationwide organization. Respondents who stated their organizations did not primarily serve LMI population or were not direct service providers were excluded from the analysis. Given the structure of their organization they likely had further distance from LMI populations, and thus were likely not as representative of the conditions in LMI communities. I also found that their responses were statistically different from other respondents. I used 363 responses for the Tenth District analysis.

Responses were collected through a convenience sampling method that relied on contact databases to identify representatives of nonprofit organizations, financial institutions, government agencies and other community organizations. These representatives were invited to participate in the survey via emails, newsletters and social media posts.