Summary of Quarterly Indicators

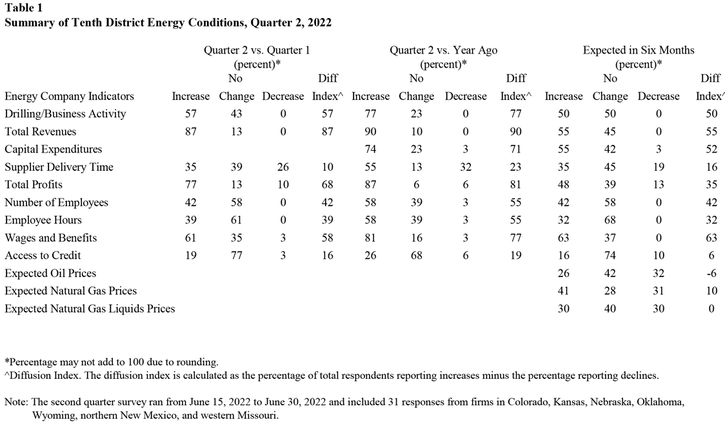

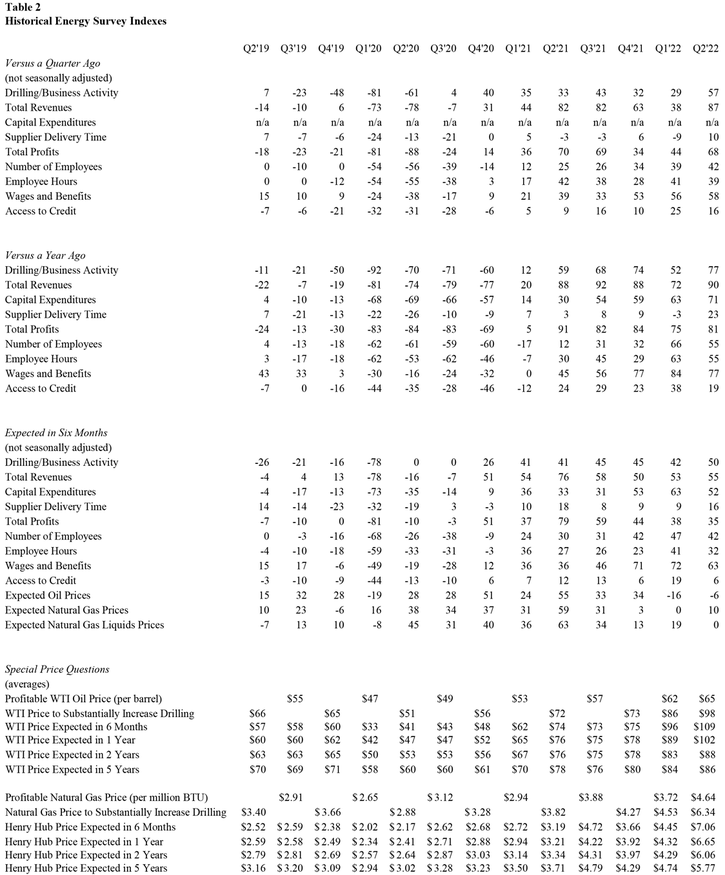

Tenth District energy activity accelerated in the second quarter of 2022, as indicated by firms contacted between June 15th, 2022, and June 30th, 2022 (Tables 1 & 2). The drilling and business activity index accelerated from 29 to 57, the highest on record since December 2016 (Chart 1). The quarterly indexes for revenues, number of employees, and wages and benefits, reached their highest levels since the survey began in 2014. The index for profits remained elevated, and supplier delivery time also increased. On the other hand, the pace of growth for employee hours and access to credit indexes eased.

Chart 1. Drilling/Business Activity Index vs. a Quarter Ago

Skip to data visualization table| Quarter | Vs. a Quarter Ago | Vs. a Year Ago |

|---|---|---|

| Q2 18 | 26 | 41 |

| Q3 18 | 45 | 57 |

| Q4 18 | -13 | 17 |

| Q1 19 | 0 | 17 |

| Q2 19 | 7 | -11 |

| Q3 19 | -23 | -21 |

| Q4 19 | -48 | -50 |

| Q1 20 | -81 | -92 |

| Q2 20 | -62 | -70 |

| Q3 20 | 4 | -71 |

| Q4 20 | 40 | -60 |

| Q1 21 | 35 | 12 |

| Q2 21 | 33 | 59 |

| Q3 21 | 43 | 68 |

| Q4 21 | 32 | 74 |

| Q1 22 | 29 | 52 |

| Q2 22 | 57 | 77 |

Year-over-year indexes were mixed compared with the previous survey. The year-over-year drilling and business activity index rose from 52 to 77. The year-over-year indexes for revenues, capital expenditures, and profits increased at the fastest rate in survey history (since 2014). Other survey indexes remained highly positive, indicating growth.

Expectations for future activity remained strong in Q1 2022. The future drilling and business activity index grew from 42 to 50, and expectations for future revenues rose at a faster pace. However, firms expected slightly more modest growth for capital spending, profits, employment, wages and benefits, and access to credit moving forward. Price expectations for oil were lower compared to current prices. Expectations for natural gas prices expanded, while natural gas liquids prices were expected to remain flat.

Summary of Special Questions

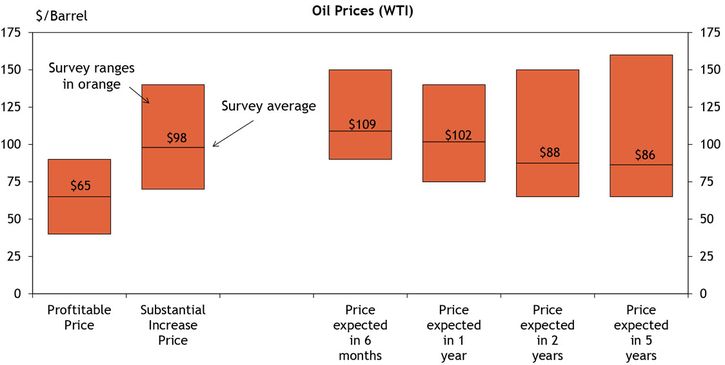

Firms were asked what oil and natural gas prices were needed on average for drilling to be profitable across the fields in which they are active. The average oil price needed was $65 per barrel, while the average natural gas price needed was $4.64 per million Btu (Chart 2). Firms were also asked what prices were needed for a substantial increase in drilling to occur across the fields in which they are active. The average oil price needed was $98 per barrel, with a range of $70 to $140. The average natural gas price needed was $6.34 per million Btu, with responses ranging from $3.50 to $12 (Chart 3). Overall, firms reported the highest prices needed to substantially increase drilling in survey history (since 2014).

Chart 2. Special Question - What price is currently needed for a drilling to be profitable and for a substantial increase in drilling to occur for oil? What do you expect WTI prices to be in six months, one year, two years, and five years?

Chart 3. Special Question - What price is currently needed for a drilling to be profitable and for a substantial increase in drilling to occur for natural gas? What do you expect Henry Hub prices to be in six months, one year, two years, and five years?

Firms were also asked what they expected oil and natural gas prices to be in six months, one year, two years, and five years. Oil price expectations again surpassed survey records, and natural gas expectations jumped compared to Q1 2022. The average expected WTI prices were $109, $102, $88, and $86 per barrel, respectively. The average expected Henry Hub natural gas prices were $7.06, $6.65, $6.06, and $5.77 per million Btu, respectively.

Energy firms were also asked about the impact of supply-chain issues (Chart 4). More than 80% of firms reported that supply-chain issues had a slightly or significantly negative impact.

Chart 4. Special Question - How would you rate the impact of supply-chain issues on your firm?

Skip to data visualization table| Supply-chain issues | How would you rate the impact of supply-chain issues on your firm? |

|---|---|

| No supply-chain issues | 3.2 |

| No impact | 0 |

| Slightly negative | 54.8 |

| Significantly negative | 38.7 |

| No opinion/don't know | 3.2 |

In addition, firms were asked about constraints to growth (Chart 5). Around 55% of firms reported uncertainty about government regulation, 32% of firms reported labor shortages, cost inflation and/or supply-chain bottlenecks, and about 7% of firms reported volatility in oil prices.

Chart 5. Special Question - Which of the following is the primary reason driving uncertainty regarding your firm's outlook?

Skip to data visualization table| Primary reason | Which of the following is the primary reason driving uncertainty regarding your firm's outlook? |

|---|---|

| Uncertainty about government regulation | 54.8 |

| Labor shortages, cost inflation and/or supply-chain bottlenecks | 32.3 |

| Volatility in oil prices | 6.5 |

| Other | 6.5 |

Selected Energy Comments

“Historically, higher prices would usher in higher supplies and thus lower prices. External factors will prolong the cycle this time.”

“There is a near term supply imbalance that was manifested out of multi-year capital under-investment and rapid demand improvements (hence global inventories decreasing rapidly). Now we're finding demand tempered with economic uncertainty entering the picture. Long term the marginal barrel should decrease, however the restraint in OPEC and service situation could be important to better predicting supply changes.”

“[Oil] demand will be steady post COVID moderated by high prices. Supply will be capacity restrained with below average capital spending.”

“Increases in [oil] supply will continue to be minimal due to capital constraints, regulatory burdens and labor/supply shortages.”

“We need labor. We would produce more if we could.”

“[Our price expectations are based on] continued development of domestic resources and easing of tensions in eastern Europe.”

“Global growth will continue to play the biggest role with higher prices. Russia has a major role with this as well.”

“The majority of our acreage is federal. We cannot drill it without the ability to fracture treat the well during completion due to the quasi moratorium on fracking on federal acreage.”

“Prices will stay elevated due to little new investment in the search for reserves. Much of the expenditures have just replaced depleted reserves. Demand for fossil fuels will remain steady or even increase.”

“The markets will be very volatile for a while… maybe for the next 12 months.”

Additional Resources

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author