In an effort to lower inflation, the Federal Open Market Committee quickly raised rates in 2022, increasing the federal funds rate by 4.5 percentage points from March to December. However, inflation remains high: the price index for personal consumption expenditures excluding food and energy (core PCE) increased by 4.4 percent over 2022, well above the FOMC’s 2 percent objective. Although goods inflation has slowed in recent months, strong services inflation has kept overall inflation high.

More specifically, inflation in non-housing services (which constitute over half of the core PCE index) has been running high, in part due to the tight labor market (Powell 2022). Indeed, employee compensation makes up about 60 percent of total value added in this sector, which means that wage increases are likely to play an important role in price setting. In aggregate, wages have remained strong, with the Atlanta Fed Wage Growth Tracker reporting a 6.1 percent increase in wages over the past year._

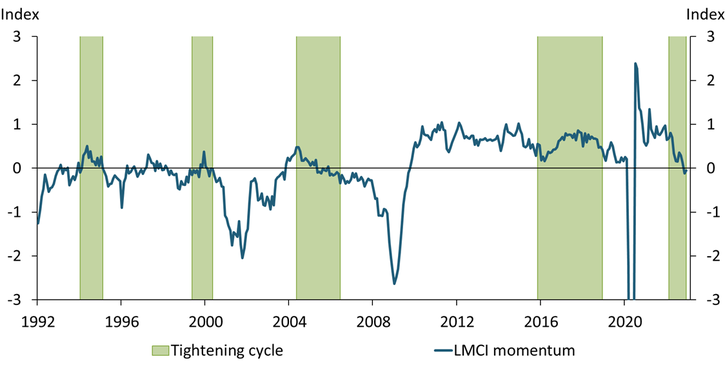

Although many labor market indicators remain tight, the Kansas City Fed Labor Market Conditions Indicators (LMCI) suggest the labor market may be starting to soften. Chart 1 shows that the LMCI measure of labor market momentum (blue line)—a composite of 24 labor market variables—turned negative in November 2022._ The chart also shows that LMCI momentum has followed a remarkably consistent pattern: during the last 20 years, momentum has only turned negative during monetary policy tightening cycles (green shaded areas), except for a short period at the start of the pandemic. Moreover, except for the 2015–19 tightening cycle, momentum has turned negative within eight to 12 months of the start of each tightening cycle. This consistent historical relationship between the timing of policy tightening and momentum turning negative suggests that the LMCI momentum indicator could provide an early indicator of policy transmitting to labor markets. To this point, momentum turned negative in November 2022 after only eight months of monetary policy tightening.

Chart 1: LMCI momentum has turned negative within a year of the start of most monetary policy tightening cycles

Sources: Board of Governors of the Federal Reserve System and Federal Reserve Bank of Kansas City (both accessed through Haver Analytics).

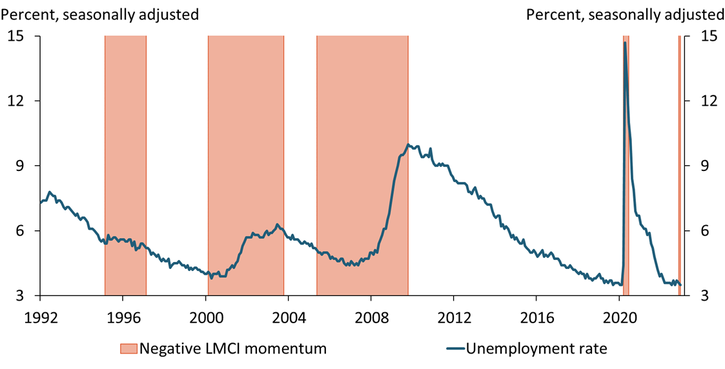

In contrast, other commonly cited measures of the labor market are much slower to react. Chart 2 shows the relationship between negative LMCI momentum (orange shaded areas) and the unemployment rate (blue line). Like momentum, the unemployment rate responded to the tightening cycles of the early and mid-2000s. However, as this figure shows, the unemployment rate began rising a year or two after momentum turned negative, and thus two to three years after the tightening cycle began.

Chart 2: The unemployment rate tends to rise a year or two after LMCI momentum turns negative

Sources: Federal Reserve Bank of Kansas City and U.S. Bureau of Labor Statistics (both accessed through Haver Analytics).

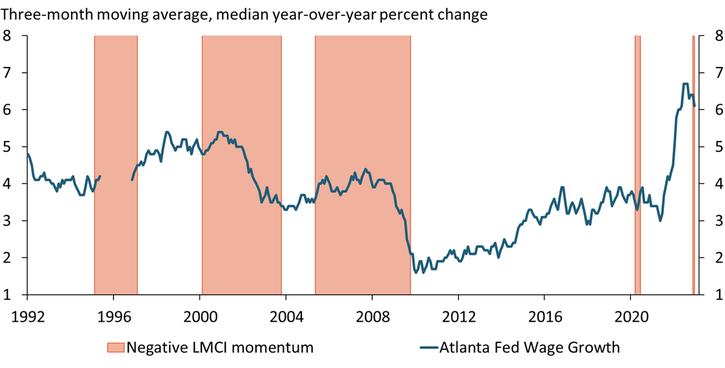

Negative momentum also appears to signal a future softening in wage growth. Chart 3 shows how wage growth (blue line), as measured by the Atlanta Fed Wage Growth Tracker, evolves during times of negative momentum (orange shaded areas). Again, much like in Chart 2, during the tightening cycles of the early and mid-2000s, wage growth peaked a year or two after momentum turned negative. Together, Charts 2 and 3 highlight that negative LMCI momentum may signal that both unemployment and wage growth could soften within the next two years.

Chart 3: Wage growth tends to slow a year or two after LMCI momentum turns negative

Notes: The Atlanta Fed Wage Growth Tracker reports the median year-over-year percent change in wages of respondents to the U.S. Census Bureau’s Current Population Survey (CPS). Due to changes to the CPS in the mid-1990s, the data are unavailable from June 1995 to October 1996.

Sources: Federal Reserve Bank of Atlanta and Federal Reserve Bank of Kansas City (both accessed through Haver Analytics).

Because momentum captures movements in 24 labor market variables, we can assess which variables contributed to momentum turning negative in each tightening cycle. For instance, when momentum turned negative in May 2005, the largest contributor to the decline from the previous month was the ISM Manufacturing Employment Index. When momentum decreased in November 2022, however, the largest contributor to the decline was an increase in announced job cuts (Challenger-Gray-Christmas). These differences in the key contributors to momentum suggest that not all tightening cycles affect the labor market the same way. In addition, the top contributors in both 2005 and 2022 did not account for even a third of the total momentum declines. Instead, the declines in momentum were caused by a range of factors in both years, with 12 variables pushing momentum down in May 2005 and 17 variables contributing to the decline in November 2022. By virtue of its construction, momentum seems to do a better job of capturing these different signals of labor market trajectory than any of its components.

In sum, LMCI momentum appears to be a leading indicator of how changes in monetary policy are affecting labor markets. Although many standard labor market variables do not begin to soften until months or even years after the end of a tightening cycle, LMCI momentum responds more quickly to monetary policy tightening. If the recent negative readings in LMCI momentum continue, other labor market variables, such as wage growth, are likely to begin to soften—reducing price pressures in the services sector and likely helping to reduce overall inflation.

Download Materials

Endnotes

-

1 Specifically, the wage growth measure from the Atlanta Fed Wage Growth Tracker is the unweighted, three-month moving average series.

-

2 While the more commonly cited LMCI level of activity indicator measures overall labor market health, the momentum indicator gives us a sense of labor market trajectory, or whether labor markets are tightening or loosening. For more details on the construction of the LMCI, see Hakkio and Willis (2014). For more recent work using the LMCI, see Glover, Mustre-del-Río, and Pollard (2021).

References

Glover, Andrew, José Mustre-del-Río, and Emily Pollard. 2021. “External LinkKC Fed LMCI Implies the Labor Market Is Closer to a Full Recovery than the Unemployment Rate Alone Suggests.” Federal Reserve Bank of Kansas City, Economic Bulletin, October 19.

Hakkio, Craig S., and Jonathan L. Willis. 2014. “External LinkKansas City Fed’s Labor Market Conditions Indicators (LMCI).” Federal Reserve Bank of Kansas City, Macro Bulletin, August 28.

Powell, Jerome H. 2022. “External LinkInflation and the Labor Market.” Speech at the Hutchins Center on Fiscal and Monetary Policy, Washington, DC, November 30.

José Mustre-del-Río is a research and policy officer at the Federal Reserve Bank of Kansas City. Emily Pollard is an assistant economist at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

José Mustre-del-Río

Research and Policy Officer