Recent articles and reports have suggested that the U.S. agricultural sector is facing a dire trajectory._ Indeed, U.S. farmers balance myriad risks and challenges, some of which have intensified in recent years. However, underlying data show that, in aggregate, the sector has remained resilient, and severe financial pressure has been limited.

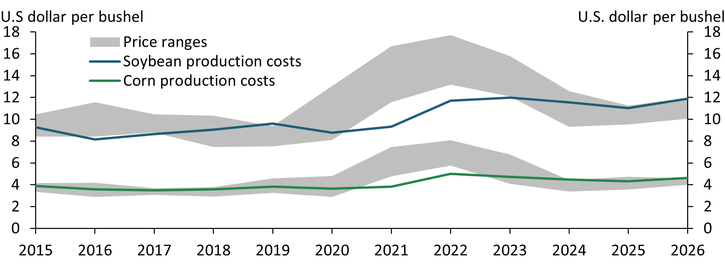

Relatively low crop prices and high costs have been a primary factor in recent weakness in U.S. agriculture. Since 2022, the prices of corn and soybeans have decreased by roughly 40 and 30 percent, respectively, while cotton and wheat have each dropped by 45 percent. At the same time, expenses have been elevated: From 2019 to 2022, total production costs in U.S. agriculture increased by 25 percent; since 2022, these costs have increased by an additional 10 percent. Chart 1 shows that the combination of lower crop prices (gray areas) and persistently high production costs (blue and green lines) has led to sharply lower profit margins for most producers.

Chart 1: Average profit opportunities for crop producers have been narrow alongside elevated production costs and relatively low crop prices

Notes: Production costs are estimated using the USDA cost and return data with national average yields. The opportunity cost of unpaid labor is excluded from production costs. Price ranges represent the highest and lowest daily spot price during each calendar year. Figures for 2026 are forecasts.

Sources: USDA, Wall Street Journal (Haver Analytics), CME Group, and authors’ calculations.

Although the tariff environment of the past year has often been cited as a leading cause of low prices in agricultural commodities, the economic reality is more complex. Following announcements of tariffs last year, China—a critical soybean trading partner in recent years—sharply curtailed purchases of U.S. soybeans (Kreitman 2025). Despite reduced exports, the price of soybeans has remained higher than at the beginning of 2025. Soybeans are a globally traded commodity, and markets adjust to shifting trade flows. For example, when China sources more soybeans from Brazil, prices respond across regions and the commodity is redirected to alternative export markets and domestic end-uses (Cowley 2020). Since 2023, domestic consumption of U.S. soybeans has increased by more than 15 percent, supported by strong demand for renewable diesel and soybean oil. The decline in soybean prices since 2022 has more likely been the result of strong production in both South America and the United States than the tariff environment that began in 2025.

More recently, conflict in the Middle East has led to a surge in the cost of fuel and fertilizer, but the effects on crop producers have thus far been small in aggregate. Historically, 40 percent of global production of urea, a nitrogen-based fertilizer applied in the production of major U.S. row crops such as corn, has transited through the Strait of Hormuz. With the Strait effectively closed over the past two months, the price of urea has increased by nearly 70 percent (Cooray 2026). In addition, the price of diesel fuel, necessary for fieldwork and farm operations, has also increased by about 70 percent since February.

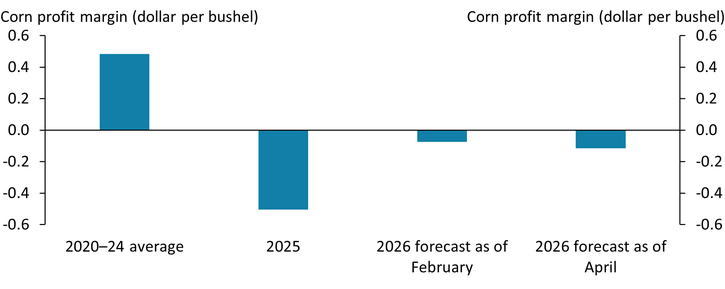

Nevertheless, the near-term effects on profit margins have been relatively small. Chart 2 shows that in February, the projected per-bushel profit margin for an average U.S. corn producer in 2026 was about −$0.07. Accounting for the increase in fertilizer and fuel prices as of late April puts the average projected profit margin at about −$0.12, recognizing that crop prices have also increased since February.

Chart 2: Fertilizer and fuel price surges are likely to reduce 2026 crop profit margins only slightly

Notes: Corn breakeven prices are calculated using the USDA cost and return data with national average yields. The opportunity cost of unpaid labor is excluded from production costs. Corn prices for 2026 are based on futures prices and set to $4.67 per bushel as of February 2026 and $4.88 per bushel as of April 2026. Prices and quantity used of nitrogen fertilizer (N) are derived from Iowa State University’s “Estimated Costs of Crop Production” for a typical corn-corn rotation for 2026. The updated price of N is based on the increase in urea prices at the Gulf. We assume that farmers adjust N application based on price changes and use consumption data from the International Fertilizer Association to determine the change in annual U.S. N consumption during the supply disruption from the Russia-Ukraine war to identify the sensitivity of U.S. N use to prices (elasticity of −0.115). We then use a rule-of-thumb of 1 bushel per acre reduction in corn yield from a 1 pound per acre decrease in N application to update corn yields for March 2026 (Enrria and others 2024). The increase in fuel and energy costs is based on the percentage increase in Brent crude oil prices and the pass-through rate of oil prices to energy prices from Känzig (2021) (elasticity of 0.45).

Sources: USDA, International Fertilizer Association, Iowa State University, Enrria and others (2024), Känzig (2021), and authors’ calculations.

Consistent with typical practices, many farmers had also already pre-purchased fertilizer requirements well in advance of the Iran conflict, limiting their immediate exposure. According to a survey conducted by the National Corn Growers Association, about 90 percent of farmers had purchased at least a portion of their fertilizer as of the end of March, and over 60 percent had purchased nearly all fertilizer needed for the season. While a prolonged conflict could affect fertilizer availability and application rates, U.S. producers are significantly less exposed in the near term than other leading global producers, such as Brazil (Arita and others 2026).

While the aggregate effects have been relatively small so far, tighter profit margins and unprecedented changes in global trade and geopolitical turmoil do place strain and uncertainty on U.S. producers. Although profit margins of U.S. crop producers are expected to improve compared with a year ago, they are substantially lower than the near-record levels of 2022 and their five-year average. Farmers have emphasized the challenges of managing their operations through these adjustments and regularly have expressed concerns about the viability of their operations if these trends persist.

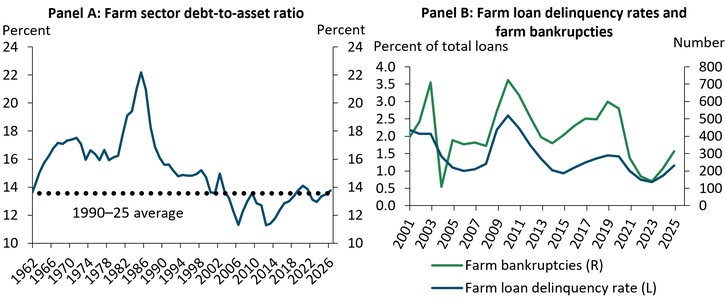

Despite recent challenges, however, the aggregate financial health of the U.S. agricultural sector has remained relatively stable. Panel A of Chart 3 shows that the debt-to-asset ratio of the U.S. farm sector is expected to increase slightly in 2026 to 13.8 percent but remains near historical norms—and well below its level during the 1980s farm crisis. The distribution of leverage across individual farms is also near historic norms, and liquidity is strong for many operations (Kreitman 2026). Resilient farm real estate values have been a primary factor limiting the increase in debt-to-asset ratios. From 2010 to 2025, the average value of farmland increased about 150 percent and has generally remained near record levels (Scott and Kreitman 2026). Lastly, while delinquency rates on farm loans have increased in recent years alongside reduced farm incomes, Panel B of Chart 3 shows that those rates remain near historical lows. In addition, Panel B shows that bankruptcy filings (green line) among farm operations have remained below levels observed during the last period of recognized financial stress from 2015 to 2019.

Chart 3: Deterioration of aggregate financial conditions in the U.S. farm sector has been modest

Sources: FFIEC, Farm Credit Administration, U.S. Courts, USDA, and authors’ calculations.

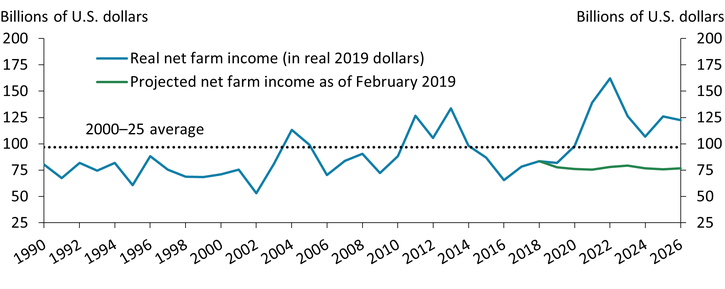

Moreover, while U.S. farm income has decreased sharply since 2022, it remains above the average of the past 25 years. Chart 4 shows that from 2022 to 2025, U.S. net farm income (blue line) dropped by about 25 percent in inflation-adjusted terms. Despite this notable decrease, U.S. farm income is expected to remain above its 25-year average in 2026, supported by strong conditions in the livestock sector and government payments (USDA 2026). Farm income is also higher than what was expected in 2019 (green line), although large government payments in recent years may be masking some of the underlying weakness in the U.S. crop sector.

Chart 4: Despite declining notably since 2022, U.S. net farm income is expected to remain above its long-term average in 2026

Sources: USDA and authors’ calculations.

Ultimately, the growing disconnect between resilient farm fundamentals and bleak public narratives about farm finances could risk leading agricultural producers and lenders to make suboptimal near-term decisions. Bridging this disconnect will require careful analysis of the underlying economic data with a heavy focus on long-term outcomes.

Endnotes

-

1 See, for example, The Economist (2026), Eller (2026), and Ayoub (2026).

Article Citation

Kauffman, Nate, and Ty Kreitman. 2026. “Resilience, Not Crisis, in the U.S. Agricultural Economy.” Federal Reserve Bank of Kansas City, Economic Bulletin, May 20.

References

Arita, Shawn, Rwit Chakravorty, Jiyeon Kim, Wuit Yi Lwin, and Sandro Steinbach. 2026. “External LinkStrait of Hormuz Closure and Global Fertilizer Trade Disruptions.” North Dakota State University Agricultural Trade Monitor, March 12.

Ayoub, Samantha. 2026. “External LinkFarm Bankruptcies Continued to Climb in 2025.” American Farm Bureau Federation, February 9.

Cooray, Ayesha. 2026. “External LinkDisruptions in the Strait of Hormuz Pressure Fertilizer Prices Ahead of the U.S. Growing Season.” Federal Reserve Bank of Kansas City Center for Agriculture and the Economy, Insights on Agricultural and Rural Economies, March 26.

Cowley, Cortney. 2020. “Reshuffling in Soybean Markets following Chinese Tariffs.” Federal Reserve Bank of Kansas City, Economic Review, June 17.

Economist. 2026. “External LinkDonald Trump Is Crushing America’s Farmers—Yet They Back Him.” April 27.

Enrria, Joaquin, Carlos Hernández, Francisco Palmero, Ana Julia Paula Carcedo, and Ignacio Antonio Ciampitti. 2024. “External LinkEvaluating Corn Yield Response to Nitrogen According to Soil Parameters in Midwest American Farmland.” Kansas Agricultural Experiment Station Research Reports, vol. 10, no. 3, July 31.

Eller, Donnelle. 2026. “External LinkCould Iowa Be Facing Another Farm Crisis? Fears Grow as Costs Rise.” Des Moines Register, May 5.

Känzig, Diego R. 2021. “External LinkThe Macroeconomic Effects of Oil Supply News: Evidence from OPEC Announcements.” American Economic Review, vol. 111, no. 4, pp. 1092–1125.

Kreitman, Ty. 2026. “Deterioration in Farm Financial Conditions Remains Gradual.” Federal Reserve Bank of Kansas City, Economic Bulletin, May 13.

Kreitman, Ty. 2025. “Key Agricultural Trade Partners Are Important for U.S. Farm Sector Revenues and Food Prices.” Federal Reserve Bank of Kansas City, Economic Bulletin, April 4.

USDA (U.S. Department of Agriculture). 2026. “External LinkFarm Sector Income & Finances: Farm Sector Income Forecast.” Economic Research Service, February 5.

Scott, Francisco and Kreitman, Ty. 2026. “Farmland Values Remained Strong in 2025.” Federal Reserve Bank of Kansas City, Center for Agriculture and the Economy, Agricultural Finance Updates, March 5.

Nate Kauffman is Senior Vice President, Omaha Branch Executive, and Director of the Center for Agriculture and the Economy at the Federal Reserve Bank of Kansas City. Ty Kreitman is an associate economist at the bank. Views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy