For the second time in about 10 years, the United States economy is confronting a deep recession with a double-digit unemployment rate and inflation below 2 percent. To help return employment and inflation to their longer-run objectives, in March the Federal Open Market Committee (FOMC) lowered the target range for the federal funds rate to near zero, announced large-scale purchases of Treasury and agency mortgage-backed securities, and established several liquidity and credit facilities. In addition, policymakers are reviewing options for further monetary policy accommodation (FOMC 2020). While the FOMC has extensive historical experience with large-scale asset purchases and forward guidance on future short-term interest rates, the Committee is also evaluating the prospect of targeting longer-term interest rates. By directly targeting specific interest rates, a policy known as yield curve control, policymakers commit to buying or selling Treasury securities to achieve the Committee’s specified yield target.

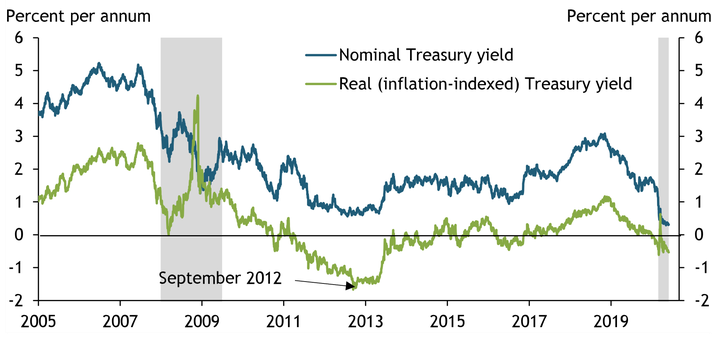

A natural first question is whether the FOMC has scope for the additional policy accommodation that yield curve control and other tools might provide. The exceptionally weak economic outlook amid the COVID-19 pandemic has pushed interest rates on nominal Treasury securities to historic lows. However, the low level of nominal interest rates reflects both low real or inflation-adjusted interest rates as well as low rates of expected inflation. The current level of real interest rates suggests policymakers may have room for additional accommodation. For example, Chart 1 shows that although the five-year nominal Treasury yield reached an all-time low in recent months, the five-year real interest rate has remained above its level in September 2012, a time when the FOMC issued forward guidance on future interest rates and announced an open-ended asset purchase program. According to the five-year real rate, the FOMC appears to retain some scope to further lower real interest rates, which would support household and business spending._

Chart 1: Inflation-Adjusted Treasury Yields Remain Above Their 2012 Lows

Notes: Both the nominal and real yields are at a constant maturity of five years. Gray bars denote National Bureau of Economic Research (NBER)-defined recessions.

Sources: Board of Governors of the Federal Reserve System (Haver Analytics) and NBER.

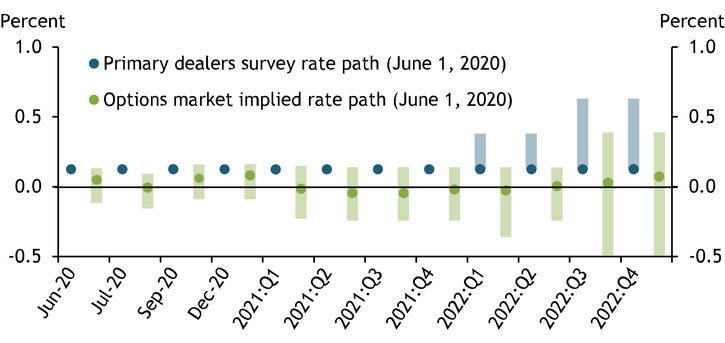

Uncertainty around the expectations of future interest rates may help explain why longer-term real interest rates currently remain above their historic lows reached in September 2012. Despite modal expectations for the policy rate to remain near zero through 2022, both surveys and interest rate options suggest substantial uncertainty around the future path of short-term interest rates. Chart 2 shows a clear upward skew in the survey-based projections for short-term interest rates (in blue) through 2022, implying market participants see a meaningful risk of early lift-off. Meanwhile, options markets (in green) reflect both the possibility of early lift-off as well as the possibility of negative rates._

Chart 2: Projections for Short-Term Interest Rates Reflect Meaningful Uncertainty

Note: Dots represent expected path and shaded areas represent 25th to 75th percentile ranges.

Sources: Federal Reserve Bank of New York, Bloomberg LP, CME Group, and authors’ calculations.

Measures of interest rate uncertainty implied by options markets can help quantify how much room for policy accommodation remains. As of June 1, 2020, the date of the most recent Survey of Primary Dealers, the option-implied volatility of policy rates two years ahead was nearly three-quarters of a percentage point, suggesting participants still see meaningful uncertainty around the rate path. Our recent research (Bundick, Herriford, and Smith 2017) shows that this uncertainty can raise longer-term nominal and real interest rates. While the outlook for employment and inflation remains highly uncertain, this research suggests reducing uncertainty around the path of policy would likely reduce longer-term interest rates.

Given this potential for additional accommodation, how can policymakers best provide it? Both yield curve control and forward guidance could reduce longer-term interest rates that are most relevant for households and businesses. Yield curve control directly targets longer-term rates by committing the central bank to buying or selling Treasury securities to achieve a desired yield. In contrast, forward guidance reduces longer-term interest rates by lowering expectations for the future path of short-term rates as well as reducing uncertainty around that path. In the current environment, even if a change in forward guidance merely ratified the modal expectations for the path of rates over the next few years, greater clarity about the path of policy would reduce interest rate uncertainty, potentially lowering longer-term rates and easing broader financial conditions.

While forward guidance and yield curve control policies may seem quite different, they have some overlap. In targeting rates at a specific time horizon, yield curve control explicitly ties monetary policy to a date on the calendar, similar to date-based forward guidance, which the Committee has used many times during the last decade.

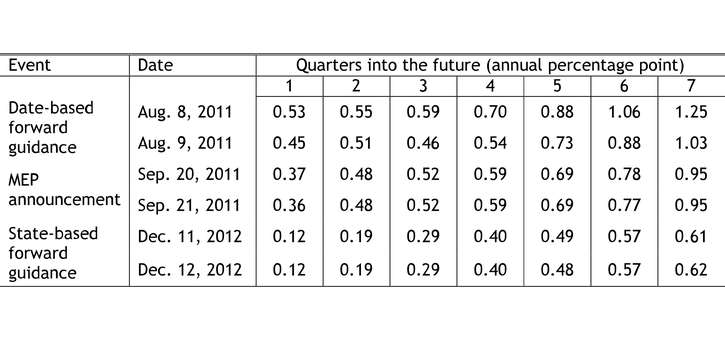

Because uncertainty about the future path of interest rates has historically declined after the FOMC’s use of date-based guidance, we argue that forward guidance can deliver many of the benefits of yield curve targeting, including lower and less volatile Treasury yields. For example, on August 9, 2011, the FOMC stated it expected to keep the federal funds rate near zero “at least through mid-2013” (FOMC 2011). The announcement reduced the two-year Treasury yield to 0.20 percent and essentially eliminated volatility in the yield curve through that horizon (Swanson and Williams 2014). The first row of Table 1 illustrates that this shift to date-based guidance drove sharp declines in options-market-implied uncertainty about future interest rates. This reduction in policy rate uncertainty led to material reductions in nominal and real interest rates (Bundick, Herriford, and Smith 2017).

Table 1: Interest Rate Uncertainty from Options Markets Responds to Date-Based Forward Guidance

Note: Options on Eurodollar futures are used to calculate the implied volatility around future interest rates.

Sources: CME Group and authors’ calculations.

Some policymakers have suggested that yield curve control could reinforce the FOMC’s guidance about the future path of the federal funds rate. However, how helpful this reinforcement would be likely depends on the type of forward guidance the FOMC issues.

The FOMC’s experience with date-based forward guidance and large-scale asset purchases in 2011, for example, suggests policymakers may not need to reinforce date-based guidance with asset purchases for the guidance to be credible. In September 2011, one month after issuing date-based guidance, the FOMC announced the maturity extension program (MEP). The goal of the MEP was to extend the average maturity of the Federal Reserve’s Treasury security portfolio by purchasing longer-term Treasuries while simultaneously selling short-term Treasuries. The MEP is thought to have operated in part through the signaling channel: by increasing the duration of the Fed’s balance sheet, the FOMC signaled its commitment to keep rates low. If operative, this mechanism would likely reduce uncertainty around the path of interest rates. However, the second row of Table 1 shows that the MEP announcement had virtually no effect on interest rate uncertainty. This suggests that once date-based guidance is in place, an increase in the duration of the Federal Reserve’s balance sheet has not historically led to further reductions in interest rate uncertainty through a signaling channel.

In contrast, state-based forward guidance, which ties the path of the federal funds rate to the evolution of the FOMC’s inflation or unemployment objectives, may benefit from the reinforcement of yield curve control. The FOMC last deployed this form of forward guidance on December 12, 2012, when it stated that it expected to keep the federal funds rate near zero “at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored” (Board of Governors 2012). The third row of Table 1 shows that this December 2012 announcement had little effect on interest rate uncertainty over the next one to two years. In addition, some longer-term Treasury rates actually increased following the announcement. Because state-based guidance does not explicitly link interest rates to a date on the calendar, augmenting state-based guidance with yield curve control could reduce uncertainty about future interest rates by effectively layering a calendar-based path for policy on top of state-dependent guidance.

However, yield curve control has the potential to create a powerful link between monetary and fiscal policy, presenting a risk to central bank independence. In the absence of a yield curve control policy, unexpected changes in the supply of government debt can influence Treasury yields. For example, the May 6, 2020 Treasury Quarterly Refunding Statement revealed a larger-than-expected amount of long-term debt issuance. This announcement steepened the Treasury yield curve, with yields on five-year, seven-year, and 10-year Treasury notes increasing on the day of the statement. If these higher government borrowing rates are passed on to other market rates, then this increase in government borrowing could reduce or “crowd out” private spending by households and firms.

This increase in yields may not have materialized if monetary policy had an explicit yield curve target in place. Instead, investors would have expected the central bank to absorb the increased Treasury issuance to achieve their targeted Treasury rate. While this added channel of yield curve control likely provides some additional accommodation relative to forward guidance, the explicit linkage between fiscal and monetary policy could create challenges for central bank independence.

Recent communication from Federal Reserve officials suggests that the FOMC is contemplating the potential for further monetary policy accommodation. Despite historically low levels of nominal yields, there exists some scope for further monetary policy accommodation. Moreover, the FOMC has several tools at its disposal to provide this accommodation, including forward rate guidance and yield curve control, or perhaps a combination of the two tools. The additional accommodation provided by yield curve control, however, may be costly: by creating a direct link between monetary and fiscal policy, yield curve control has the potential to erode the independence of the central bank. Based on the FOMC’s past use of forward guidance, we argue that date-based forward guidance has the potential to deliver much, though not all, of the accommodation of yield curve control.

Endnotes

-

1 While monetary policy can only directly control its short-term nominal policy rate, Hanson and Stein (2015) show that policy announcements can significantly influence short- and longer-term real interest rates.

-

2 While monetary policy can only directly control its short-term nominal policy rate, Hanson and Stein (2015) show that policy announcements can significantly influence short- and longer-term real interest rates.

References

Board of Governors of the Federal Reserve System. 2012. “External LinkFederal Reserve Issues FOMC Statement.” Press release, December.

Bundick, Brent, and Trenton Herriford. 2017. “How Do FOMC Projections Affect Policy Uncertainty?” Federal Reserve Bank of Kansas City, Economic Review, vol. 102, no. 2, pp. 5–22.

Bundick, Brent, Trenton Herriford, and A. Lee Smith. 2017. “Forward Guidance, Monetary Policy Uncertainty, and the Term Premium.” Federal Reserve Bank of Kansas City, Research Working Paper no. 2017-07, July.

FOMC (Federal Open Market Committee). 2020. “External LinkMinutes of the Federal Open Market Committee, June 9–10, 2020.” July 1.

———. 2011. “External LinkMinutes of the Federal Open Market Committee, August 9, 2011.” August 30.

Hanson, Samuel G., and Jeremy C. Stein. 2015. “External LinkMonetary Policy and Long-Term Real Rates.” Journal of Financial Economics, vol. 115, pp. 429–448.

Swanson, Eric T., and John C. Williams. 2014. “External LinkMeasuring the Effect of the Zero Lower Bound on Medium- and Longer-Term Interest Rates.” American Economic Review, vol. 104, no. 10, pp. 3154−3185.

Brent Bundick and A. Lee Smith are research and policy advisors at the Federal Reserve Bank of Kansas City. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Brent Bundick

Vice President