Business investment is a key component of the business cycle. When firms are optimistic about the outlook and demand for their products, they hire workers and invest in capital to improve their productive capacity. Thus, during economic expansions, investment increases along with the productive capacity of the entire economy; similarly, during recessions, the pace of investment decreases.

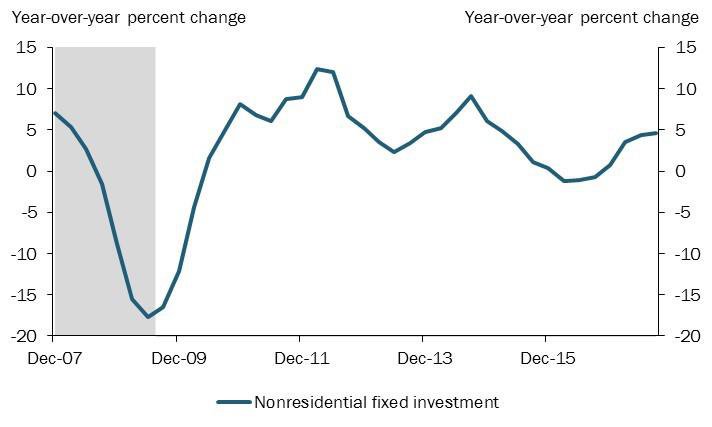

However, from 2014 to 2016, business investment declined while the overall economy expanded. Chart 1 shows year-over-year changes in real private nonresidential fixed investment since the Great Recession. This measure includes investment in structures, equipment, and intellectual property, but excludes residential investment and inventory accumulation. The chart shows a sharp downturn in investment during the Great Recession followed by a rebound as the economy entered the expansion. However, investment growth decelerated noticeably from 2014 to 2016, and even became negative in year-over-year terms for the first three quarters of 2016. GDP growth slowed slightly in those quarters but remained above 1 percent.

Chart 1: Real Private Nonresidential Fixed Investment since the Great Recession

Note: Gray bars denote National Bureau of Economic Research (NBER)-defined recessions.

Sources: BEA, NBER, and Haver Analytics.

Characterizing the investment downturn from 2014 to 2016 requires some nuance. Although Chart 1 clearly shows that growth slowed over several quarters, this slowdown was nowhere near as dramatic as the slowdown during the Great Recession. The more recent slowdown might simply represent a couple of rather weak observations in an otherwise standard expansion—but it might also represent an unofficial recession that affected only the investment sector.

To characterize the recent changes in investment, I estimate a “regime-switching” model for investment growth from 1947:Q1 to 2017:Q3. This statistical model attributes changes in quarterly growth to either an “investment-expansion” or an “investment-recession” regime._ Although the National Bureau of Economic Research (NBER) dates U.S expansions and recessions, these dates do not necessarily match up with the investment regimes; thus, an investment-recession regime could occur during an NBER-defined expansion.

Estimates from the statistical model on investment growth show that investment largely moves with the business cycle. In the first, expansionary regime, quarterly investment grows at a relatively high annual rate of around 7.6 percent, on average. As is typical of economic expansions, this regime tends to be persistent, with an expected duration of slightly less than 11 quarters. In the second, recessionary regime, quarterly investment falls by an average of 3.7 percent at an annual rate, with a shorter expected duration of around four quarters.

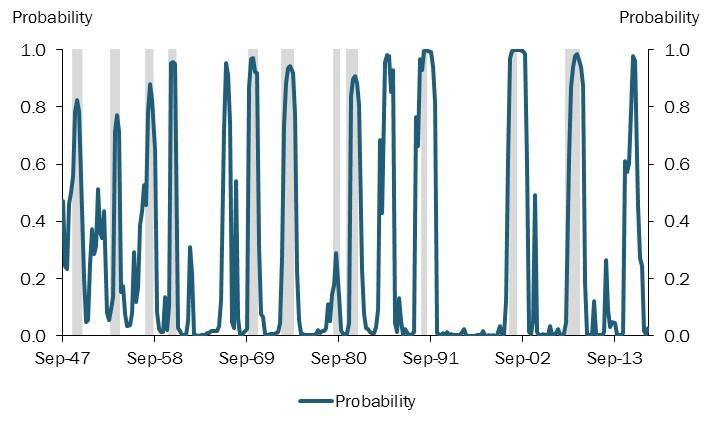

The regime-switching model also produces estimates of when investment growth was in each regime, which can shed light on the slowdown in 2014–16. Chart 2 shows the probability of investment being in the recession regime for every quarter in the sample. These “smoothed probabilities” represent a retroactive, rather than real-time, view of investment growth dynamics over the full sample. When the line in Chart 2 is close to 1, investment is more likely to be in a recession; when the line is close to 0, investment is more likely to be in an expansion.

Chart 2: Probability of Being in Investment-Recession Regime

Note: Gray bars denote National Bureau of Economic Research (NBER)-defined recessions.

Sources: BEA, NBER, Haver Analytics, and author’s calculations.

The estimates of when investment growth was in each regime align closely with NBER-defined recession dates for the economy as a whole. During NBER recessions—and occasionally, in quarters immediately before or after them—investment enters the recession regime. This finding makes intuitive sense, since a contracting economy overall should lead firms to cut back on their investment activities.

The regime estimates in Chart 2 also show that the investment sector was in the recession regime in 2014–16. Specifically, using a threshold value for the probabilities of 0.5, the model implies that investment was in a recession from 2014:Q4 to 2016:Q2. However, this recessionary period appears to have ended, as readings from 2016:Q3 onward declined from 0.3 to 0. Overall, the estimates suggest that investment did not simply receive weak transitory shocks from 2014 to 2016; rather, the investment sector entered a recession within an overall economic expansion.

Investment’s recent behavior is highly unusual. The historical probabilities in Chart 2 suggest investment rarely enters the recession regime outside of an NBER recession for the economy as a whole. In fact, investment entered a recession inside an overall expansion only one other time since 1970, from 1985:Q3–1987:Q1. While circumstances differed during the 1985–87 and 2014–16 periods, this historical context gives some perspective as to the rarity of the more recent investment slowdown.

Endnotes

-

1 Foerster and Choi use regimes to model consumption dynamics, while Brown uses them to identify state-level recessions. I use the “2 Average, 2 Volatility” model from Foerster and Choi to allow for volatility regimes but focus on average growth regimes in this Bulletin. The characterization of the average growth regimes as being “investment-expansion” or “investment-recession” is a result and not imposed from the outset.

References

Brown, Jason. 2017. “Identifying State-Level Recessions.” Federal Reserve Bank of Kansas City, Economic Review, vol. 102, no. 1, pp. 85–108.

Foerster, Andrew, and Jason Choi. 2016. “Consumption Regimes and the Post-Financial Crisis Recovery.” Federal Reserve Bank of Kansas City, Economic Review, vol. 101, no. 2, pp. 25–48.

Jordan Rappaport is a senior economist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.