Notes: Gray bars denote National Bureau of Economic Research (NBER)-defined recessions at a quarterly frequency. All values taken as a year-over-year percentage point change for the four-quarter rolling average.

Sources: Bloomberg, U.S. Bureau of Economic Analysis (Haver Analytics), NBER (Haver Analytics), and authors’ calculations.

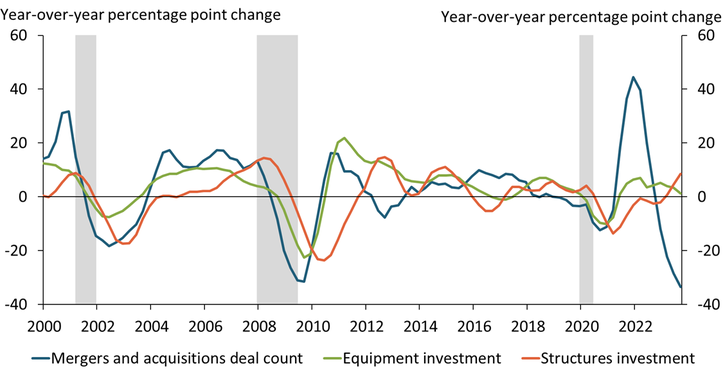

Higher interest rates and tighter financial conditions tend to slow firms’ growth and reduce mergers and acquisitions (M&A) activity. M&A deal activity (blue line) complements business fixed investments and tends to lead changes in spending on equipment (green line) and structures (orange line). The sharp decline in M&A deals in late 2022 and throughout 2023 may be a reversal of the sharp rise in M&A activity in the second half of 2021 but could also portend a decline in capital investment in the coming quarters. To learn more, see Rodziewicz and Sly (2019).

See more research from Charting the Economy.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Bethany Greene

Research Associate II

David Rodziewicz

Advanced Economics Specialist