Health care costs have risen substantially since the turn of the century as an aging population’s demand for medical care increases. Alongside increasing costs, hospitals and health systems have increasingly consolidated, particularly in states like Nebraska. Such consolidation may be a contributor to the increase in health care costs in the region. Despite increasing consolidation though, health systems continue to increase staffing as demand for health services remains robust, and as the population continues to age.

Section 1: Health Care Costs Have Continued to Increase

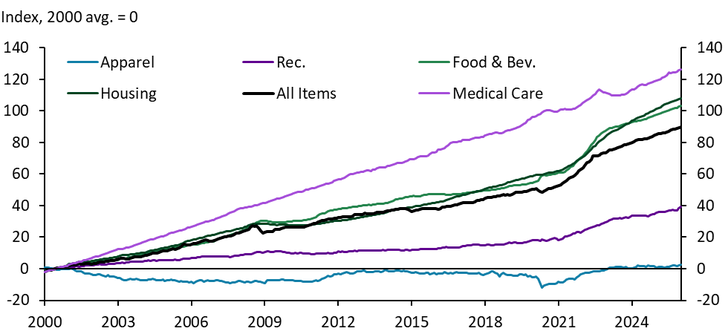

Health care costs have risen more than any other major group of goods and services since 2000. By the end of 2025, medical care goods and services cost 125% more than in 2000 (Chart 1). This represents an average annual increase of nearly 3% for medical care, significantly higher than the 2.3% average annual increase for all goods. Even housing and food—categories often noted for significant price increases—rose at slower rates than medical care.

Chart 1. Cumulative Change in Major Consumer Price Index (CPI ) Categories

Sources: BLS, Haver Analytics.

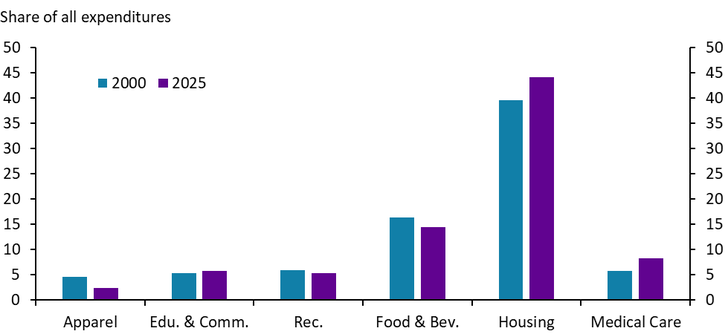

Health care goods and services have increased in importance for households. When calculating the headline price index, the Bureau of Labor Statistics assigns each good or service a weight corresponding to its importance to a household’s monthly spending. Medical care accounted for slightly more than 8% of average monthly spending in 2025 (Chart 2). While this was lower than housing (44%) and food (15%), the two largest categories, the increase in the relative importance of medical care is notable.

Chart 2. Relative Importance of Consumer Price Index Categories

Sources: BLS, Haver Analytics.

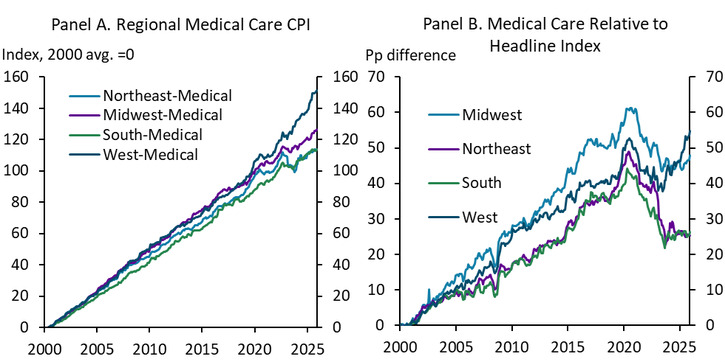

Medical care has increased in price more rapidly in the Midwest than in some other regions. By the end of 2025, medical care costs in the Midwest were 126% higher than in 2000, only slightly above the national average, but significantly higher than the increase in the South or Northeast (Chart 3, Panel A). Further, the gap between medical care and the headline consumer price index has been larger in the Midwest. By 2020, the medical care cost index was 60 percentage points higher than the overall index in the Midwest, the largest discrepancy in the country until recently (Chart 3, Panel B). The gap between the overall index and medical care narrowed after the pandemic, other than in the West, only because other goods and services accelerated more than usual.

Chart 3. Differences in Regional Medical Care CPI

Sources: BLS, Haver Analytics, author’s calculations.

Section 2: Health Care Consolidation Has Increased, Particularly in Rural Areas

Over the last 25 years, the health care industry has increasingly consolidated. Consolidation has affected hospitals, general care practitioners, specialists, and insurers alike (Fulton 2017). In most circumstances, consolidation results in fewer services offered at hospitals and other provider locations, but can also result in closure of an entire health care facility (Edmiston 2019). Consolidation or closure of health care facilities have been shown to cause several detrimental outcomes including lower growth in local employment and wages (Edmiston 2019; Prager and Schmitt 2021), lower quality of care (Joynt 2011), increasing wait times at the next nearest facility (Hsia 2019), and longer drive times to health care facilities (Hung 2016).

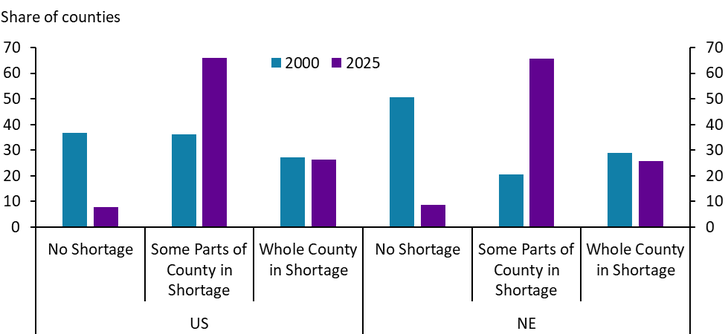

Amid higher costs and increasing consolidation, the number of areas facing shortages of health professionals has increased. In 2025, about 90% of counties faced primary care provider shortages to some degree in both the United States and Nebraska (Chart 4). In 2000, less than half of Nebraska counties faced provider shortages. However, for most areas, primary care shortages only affected some locations or populations within a county. Thus, in most counties, some number of health care facilities likely remain open but consolidation in the industry may have made it more challenging for some communities within a certain county to physically access care.

Chart 4. Counties with a Shortage of Primary Care Health Providers

Note: A county is in shortage if the ratio of the population to the full-time-equivalent primary care physicians is at least 3,500:1 or at least 3,000:1 with unusually high needs for primary care or insufficient capacity of existing providers.

Sources: HRSA Area Health Resources File, author’s calculations.

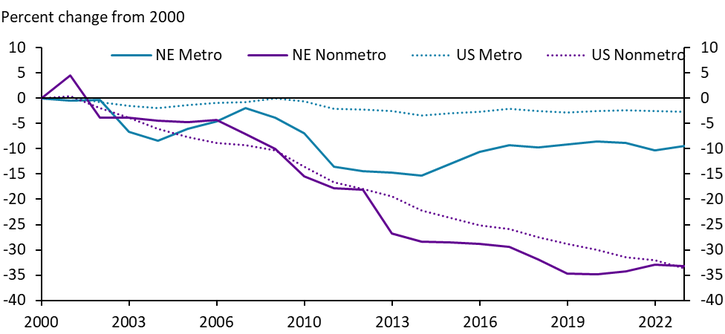

Perhaps indicative of consolidation across provider locations, the number of hospital beds has fallen nationwide. The decline has been smallest in metropolitan areas, where the number of available beds in Nebraska declined by 10% from 2000 to 2023 (Chart 5). In contrast, the decrease in nonmetropolitan, or rural, areas has been much more severe. In both rural Nebraska and rural areas nationwide, hospital beds have declined by more than a third since 2000.

Chart 5. Hospital Beds by Region

Sources: HRSA Area Health Resources File, author’s calculations.

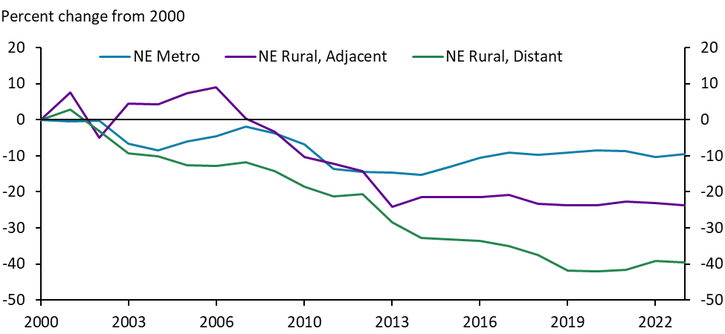

In Nebraska, the number of hospital beds has fallen most substantially in areas that are further from major cities. In rural areas that do not border a metropolitan area, the number of available hospital beds has fallen by 40% since 2000 (Chart 6).

Chart 6. Hospital Beds by Region, Nebraska

Sources: HRSA Area Health Resources File, author’s calculations.

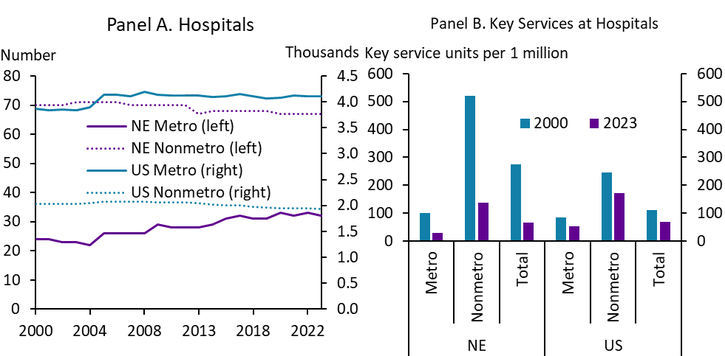

The number of key services offered by hospitals has fallen alongside the decline in availability of hospital beds even as the number of hospitals has remained relatively unchanged. Since 2000, the number of hospital locations has increased slightly in Nebraska’s cities while only declining slightly in rural areas (Chart 7, Panel A). Over the same time period, the number of key service units has fallen on a per capita basis across all areas (Chart 7, Panel B). A “key service unit” could be an emergency department, a trauma center, or an intensive care unit (see the note for a full list included in this analysis). In an area undergoing a degree of hospital consolidation, a hospital system that previously comprised five hospitals might choose to close all but one obstetrics unit, for example, contributing to an overall decline in the number of key services available.

Chart 7. Hospitals and Number of Units Offering Key Services at Hospitals

Note: “Key Services” include general medicine and surgery care for adults, pediatric general medicine and surgery, obstetrics, general intensive care, physical rehabilitation, psychiatrics, acute long term care, alcohol and drug rehabilitation, emergency department, trauma center, oncology, outpatient surgery, primary care, urgent care, and women’s health.

Sources: HRSA Area Health Resources File, author’s calculations.

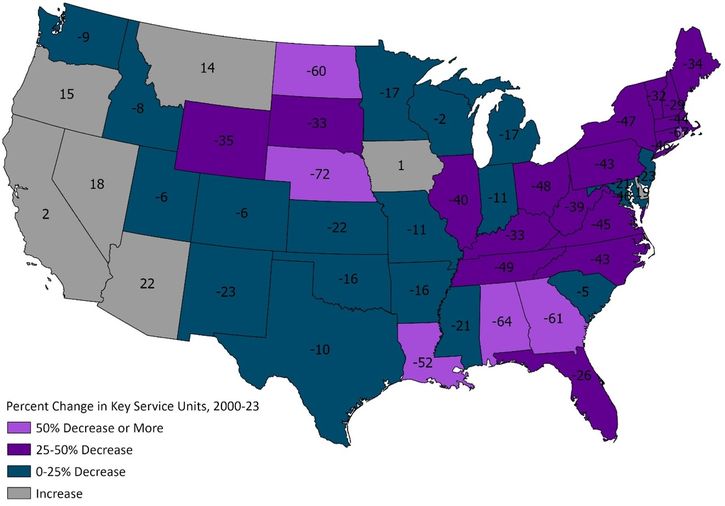

Closures of specialized health care units have been particularly acute in Nebraska. In fact, the number of unique health care units offering key services fell the most in Nebraska relative to other states between 2000 and 2023 (Map 1). Unique key service offerings fell by more than 70% between 2000 and 2023 compared with a 26% decline nationally. Notably, key health care service units in demographically and economically similar states like Kansas and Iowa either fell at a slower pace than the nation (Kansas) or actually increased (Iowa). However, even in states where more key service units opened, new units did not keep pace with the increase in population. Nationwide, while the number of key service units operating declined by 26%, the number of per capita key service units declined by more than 37%. Thus, consolidation alongside a growing population has limited the physical availability of health care.

Map 1. Unique Offerings of Key Services at Hospitals

Note: “Key Services” include general medicine and surgery care for adults, pediatric general medicine and surgery, obstetrics, general intensive care, physical rehabilitation, psychiatrics, acute long-term care, alcohol and drug rehabilitation, emergency department, trauma center, oncology, outpatient surgery, primary care, urgent care, and women’s health.

Sources: HRSA Area Health Resources File, author’s calculations.

Section 3: Despite Consolidation, Demand for Health Care to Remain Robust

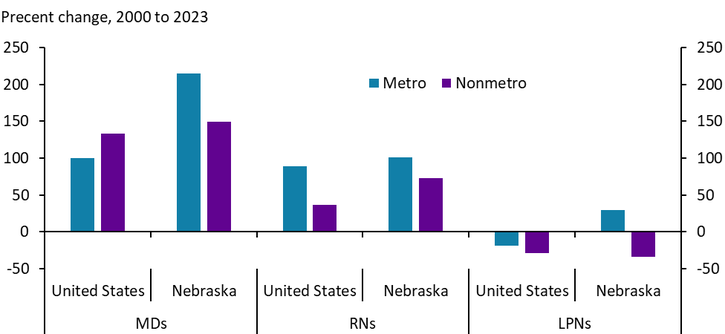

Despite consolidation of key services, hospital staffing increased between 2000 and 2023. The number of physicians in rural Nebraska more than doubled between 2000 and 2023, and registered nurses nearly doubled as well (Chart 8). Hospitals and health systems have continued seeking highly trained health professionals while relying less on licensed practical nurses (LPNs) and other positions requiring less education. While not shown, robust hiring in the health care sector continued through 2025.

Chart 8. Full Time Hospital Staff

Sources: HRSA Area Health Resources File, author’s calculations.

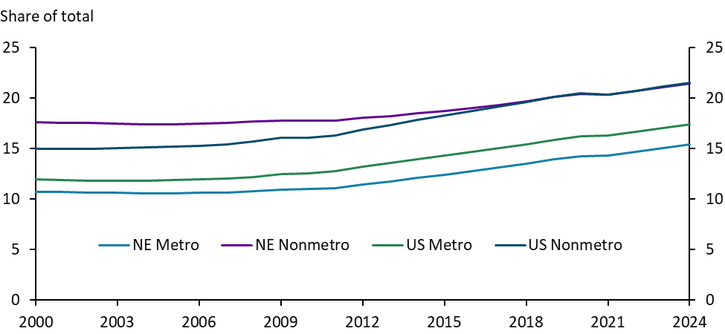

Long-running staffing increases at hospitals likely reflect growing demand for health care services as the population ages. The share of the population age 65 or older began increasing steadily across all geographies around 2010 (Chart 9). By 2024, more than 20% of the nonmetropolitan population was older than 65. As this share increases, demand for health care services by residents in these areas is likely to rise as well. Further, while consolidation has affected all areas, the more significant losses of hospital beds in nonmetropolitan areas could place additional stress on the physical provision of health services outside of cities even as systems continue to add staff.

Chart 9. Share of Population Age 65 and Above

Sources: Census Bureau, Haver Analytics.

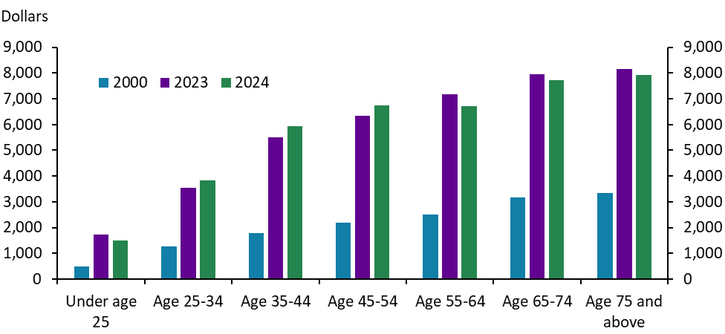

Older people have tended to spend more on health care than younger people. As of 2024, people aged 65 years and older spent more than $7,500 per year on health care services on average (Chart 10). In contrast, individuals younger than 35 spent less than $4,000 per year on average. While dollar values have increased with prices over the past 25 years, the pattern has remained consistent: as individuals age, personal health care outlays have increased substantially.

Chart 10. Consumer Expenditures on Health Care, U.S. Average

Source: BLS

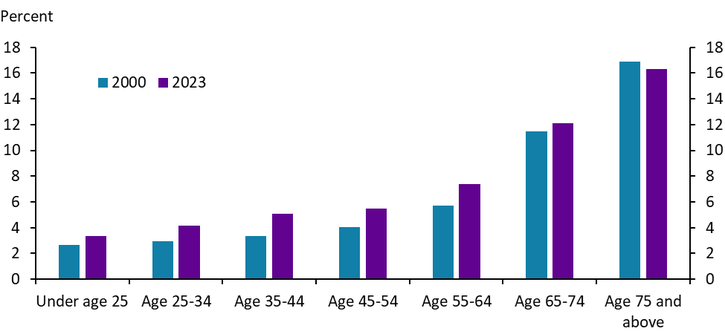

Not only have actual health care expenditures increased with age, but the share of disposable income devoted to health care has also risen with age. The share of post-tax income devoted to health care expenses has been close to 12% for those age 65 to 74 and increases to approximately 16% by age 75 (Chart 11). As individuals retire and incomes fall from peak earning years, both expenditures and the share of income directed to health care typically increase. Thus, the persistent rise in health care costs in recent decades likely affects older populations most significantly, as they both spend more on health care overall and devote a larger share of their income to medical care.

Chart 11. Health care expenses as a share of post-tax income

Source: BLS

Strong and steady increases in medical care prices have affected communities throughout the country, but particularly in Midwestern states like Nebraska. Increases in health care prices are likely due, in part, to consolidation in the industry. In addition to higher prices, indirect costs resulting from consolidation – such as increased driving time and lower quality of care – also affect communities throughout the state. While consolidation poses logistical challenges for many communities, demand for health care will likely remain strong as the population continues to age. Hospitals and health systems likely recognize this strong demand and continue to staff rural areas, even if the location of that staff differs from several decades ago.

References

Edmiston, Kelly. 2019. “External LinkRural Hospital Closures and Growth in Employment and Wages.” Federal Reserve Bank of Kansas City, Economic Bulletin, July 19.

Fulton, Brent. 2017. “External LinkHealth Care Market Concentration Trends in the United States: Evidence and Policy Responses.” Health Affairs, vol. 39, no. 9, pp. 1530–1538.

Hsia, Renee Y. and Yu-Chu Shen. 2019. “External LinkEmergency Department Closures and Openings: Spillover Effects on Patient Outcomes in Bystander Hospitals.” Health Affairs, vol. 38, no. 9, pp. 1496–1504.

Hung, Peiyin, Katy B. Kozhimannil, Michelle M. Casey, and Ira S. Moscovice. 2016. “External LinkWhy Are Obstetric Units in Rural Hospitals Closing Their Doors?” Health Services Research, vol. 51, no. 4, pp. 1546–1560.

Joynt, Karen E., Yael Harris, E. John Orav, and Ashish K. Jha. 2011. “External LinkQuality of Care and Patient Outcomes in Critical Access Rural Hospitals.” JAMA, vol. 306, no. 1, pp. 45–52.

Prager, Elena and Matt Schmitt. 2021. “External LinkEmployer Consolidation and Wages: Evidence from Hospitals.” American Economic Review, vol. 111, no. 2, pp. 397–-427.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author