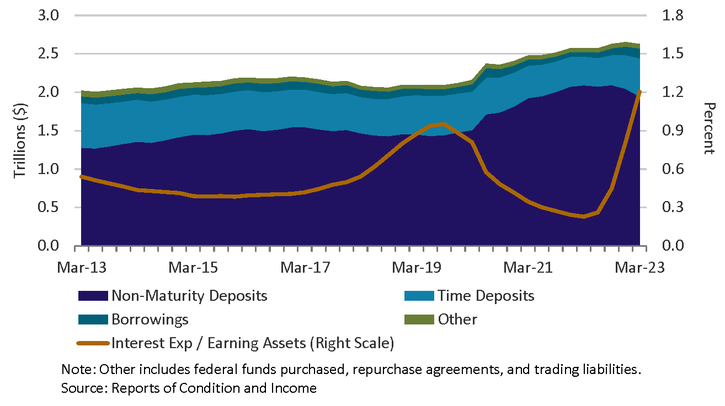

Total Liabilities by Category and Quarterly Cost of Earning Assets

- Total deposits declined for nearly half of all community banking organizations_ (CBOs) during 1Q 2023, down $39 billion (1.6 percent) from year-end 2022. Pricing pressures and consumer behavior in the high-interest rate environment have also led to a change in bank deposit composition, with shifts from non-maturity deposits (declining $99 billion) into time deposits (increasing $60 billion), which now comprise over 20 percent of total deposits.

- With deposit runoff and increased competition, CBOs are increasingly using noncore funding sources to boost asset-based liquidity and support growth in earning assets. Total borrowings increased $15 billion (14 percent) in 1Q 2023, led by an $8.0 billion increase in other borrowings—including, but not limited to, Discount Window activity and Bank Term Funding Program funds—and an additional $7.4 billion increase in Federal Home Loan Bank (FHLB) advances._

- The cost of earning assets (interest expense as a percentage of earning assets) has increased rapidly, up 39 basis points in 1Q 2023, and was nearly double the increase of 21 basis points in the yield on earning assets (interest income as a percentage of earning assets). Given the ongoing elevated interest rate environment, heightened competition and changes in consumer behavior may continue to put upward pressure on funding costs at CBOs.

Questions or comments? Please contact KC.SRM.SRA.CommunityBankingBulletin@kc.frb.org

Endnotes

-

1 Community banking organizations are defined as having less than $10 billion in total assets.

-

2 See recent CBB discussing increases in FHLB borrowings in relation to tangible common equity.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.