Farm lending activity at commercial banks slowed through the first half of 2023 as interest rates continued to push higher. The volume of non-real estate farm loans at commercial banks declined for the second consecutive quarter and average interest rates on agricultural loans increased for the sixth consecutive quarter. The rise in interest rates was generally consistent across loans and lenders of all sizes, but rates remained slightly lower for bigger loans and at the largest banks. As rate terms have moved up rapidly over the past year, variable rate notes have become more prevalent.

The outlook for the U.S. farm economy has moderated in recent months as risks of more limited profit opportunities have grown alongside softening in commodity markets and elevated production expenses. High input costs and increases in interest rates have raised financing costs considerably, but conditions have also encouraged many producers to adjust operations to reduce borrowing needs or utilize cash reserves to fund some expenses. Broad strength in farm finances has continued to support historically strong loan performance, but farm profitability will remain important for agricultural credit conditions and lending demand in the coming months.

Second Quarter National Survey of Terms of Lending to Farmers

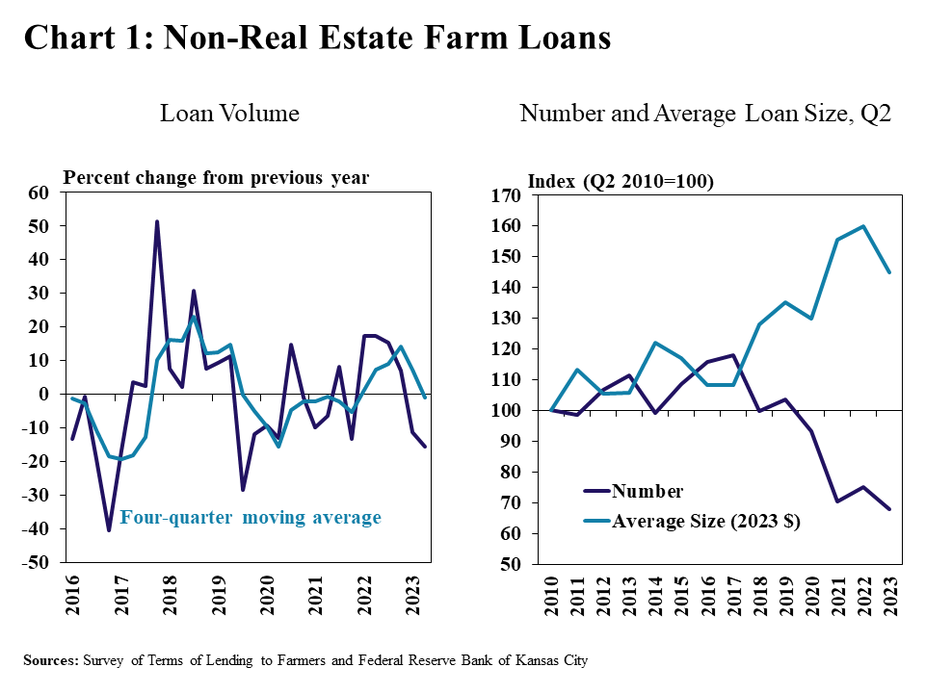

A slowdown in farm lending continued into the second quarter. According to the Survey of Terms of Lending to Farmers, the volume of new non-real estate farm loans at commercial banks was about 15% less than a year ago (Chart 1). The drop in lending was attributed to a lower average size of loans and a fewer number of loans compared with last year.

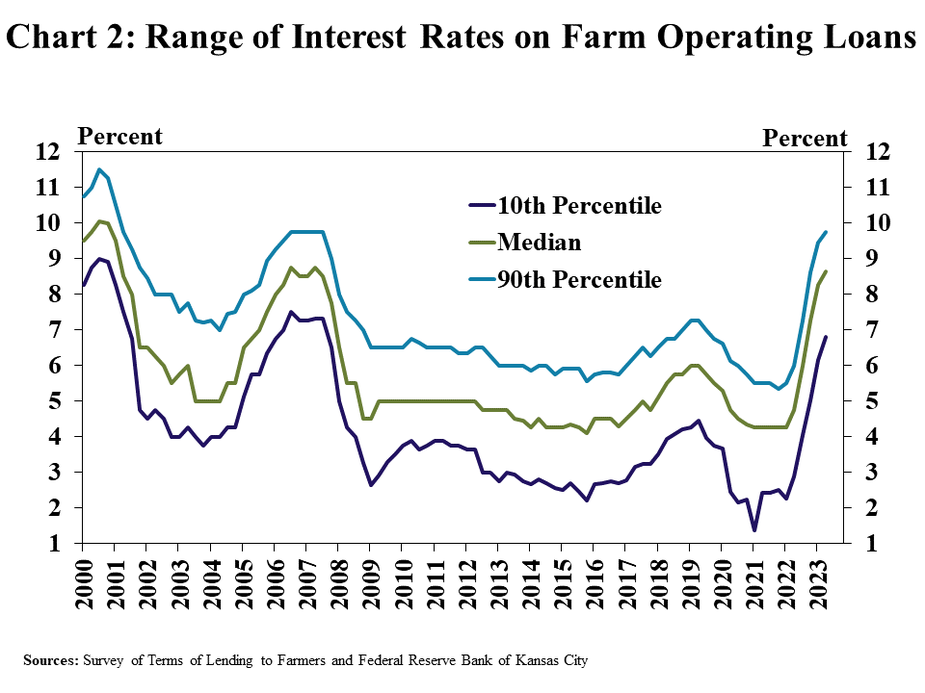

Agricultural lending has slowed as interest rates on farm loans have increased considerably. The median rate on non-real estate loans doubled from the beginning of 2021 and half of all new operating loans in the second quarter garnered a rate above 8.5% (Chart 2). Moreover, one tenth of new farm operating loans carried an interest rate of nearly 10% according to the second quarter survey. In contrast, at the beginning of 2022, more than half of all loans had a rate less than 4.5% and the sharp change has likely influenced operational and financing decisions for many producers.

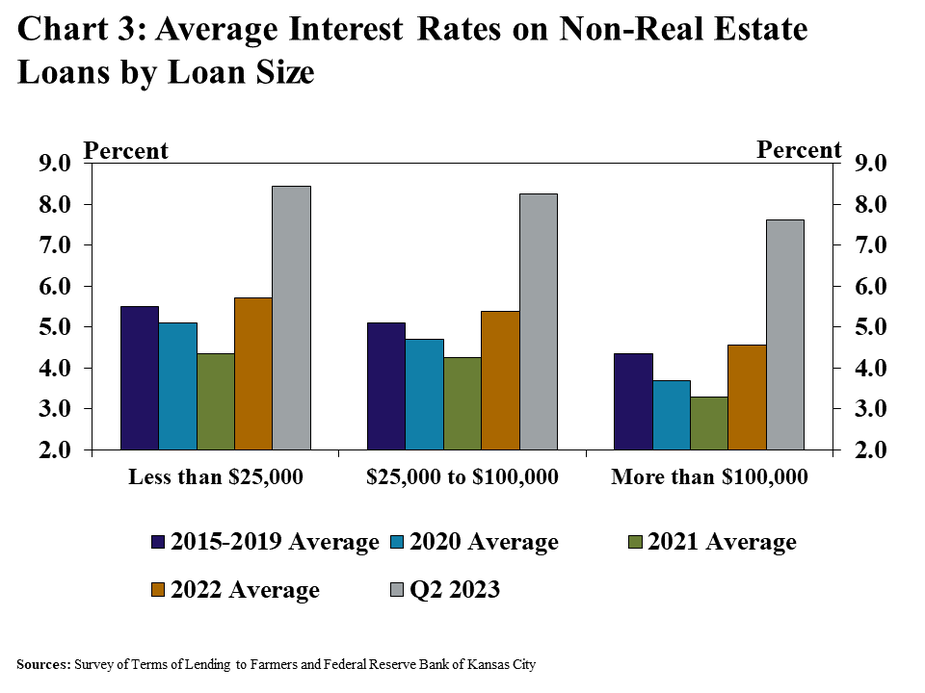

The uptick in rates remained consistent across loans of all sizes. The average rate on loans of various amounts was at least 300 basis points above the average from 2015 to 2019 (Chart 3). The mean rate on loans above $100,000 increased slightly more than smaller loans, but rates still remained somewhat lower for the largest-sized loans.

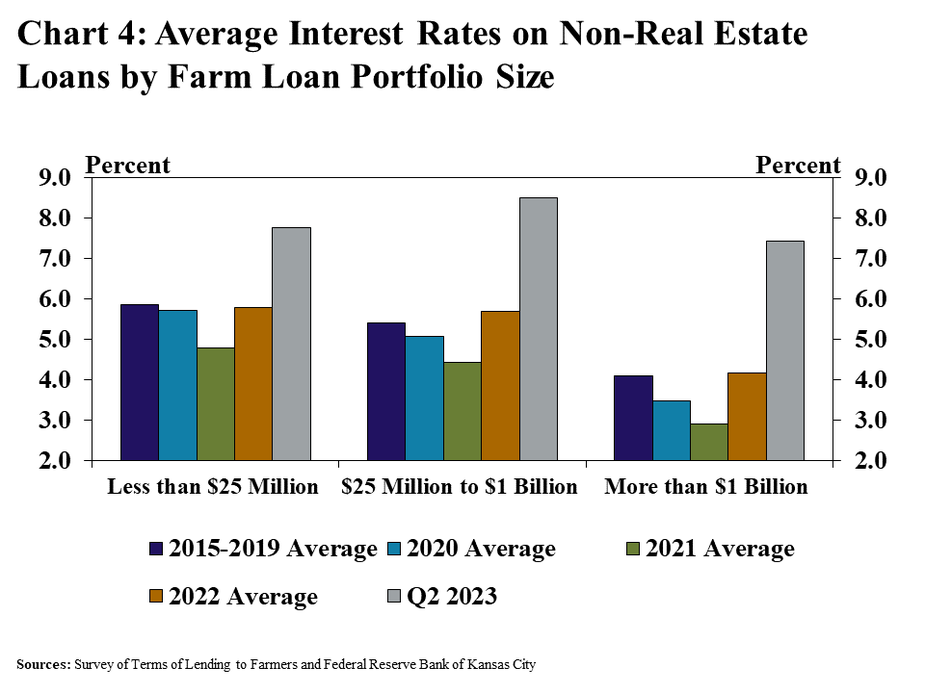

The rise in rates has also been largely consistent across banks of all sizes but has been steepest at the largest lenders. The average rate charged by banks with farm loan portfolios less than $25 million was about 200 basis points above the average from 2015 to 2019 (Chart 4). The average rate at banks with portfolios more than $25 million was over 300 basis points higher and similar to loans of larger sizes, average rates remained slightly lower at the largest lenders.

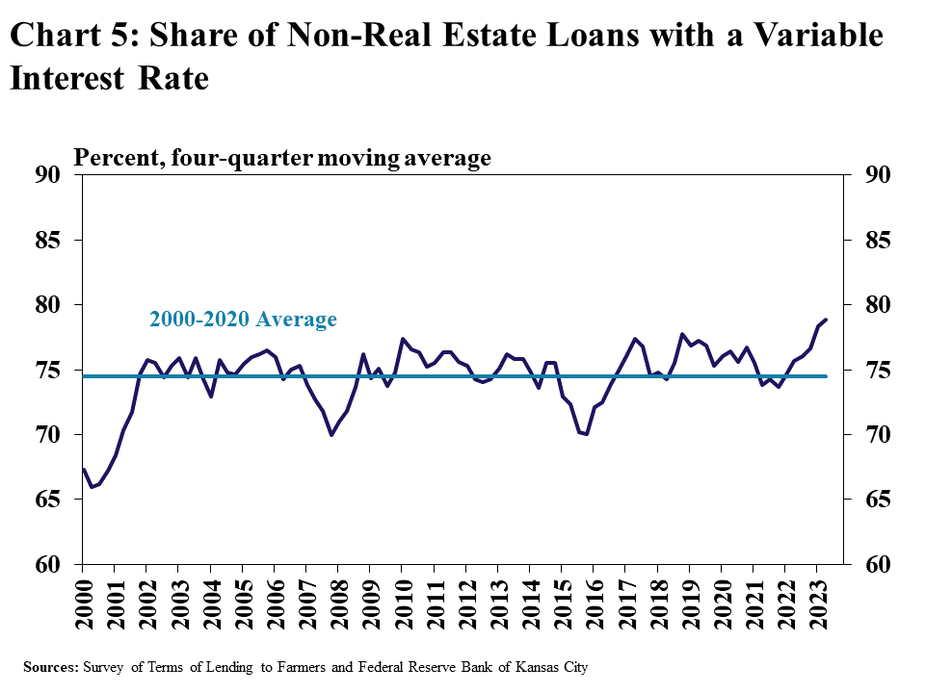

Alongside broad increases in farm loan interest rates, the share of loans with variable rates has increased modestly. Over the last four quarters, nearly 80% of non-real estate farm loans were booked with a variable rate, which was noticeably more than the historic average (Chart 5). Lenders and borrowers have likely been less interested in locking in terms for the duration of the loan in response to the rapid increase in interest rates over the past year to their highest mark since 2007.

Data and Information

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Tables

About the National Survey of Terms of Lending to Farmers

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy