Farm debt at agricultural banks grew considerably in 2024 and delinquency rates increased from historic lows. According to commercial bank call report data, farm debt at banks with concentrations in agricultural lending grew about 7% from a year earlier. Debt increased alongside weaker conditions in the agricultural economy that increased demand for production loans and led to slightly higher farm loan delinquency rates. Loan growth was accompanied by improved interest margins and slightly higher capital ratios for farm lenders. The outlook for the agricultural sector remained relatively subdued alongside low crop prices, but ad hoc government payments related to the American Relief Act could support the sector and limit financial stress for some producers in early 2025.

Fourth Quarter Commercial Bank Call Report Data

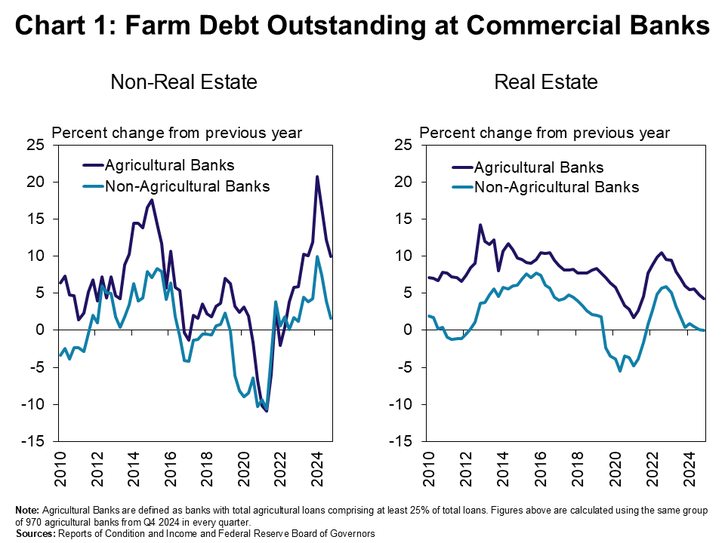

Farm debt continued to increase through the end of 2024 and was particularly strong at agricultural banks. Non-real estate loans at agricultural banks increased 10% from the previous year and, at non-agricultural banks, ended 2024 less than 2% higher (Chart 1). Real estate debt was unchanged at non-agricultural lenders and increased about 4% at farm banks.

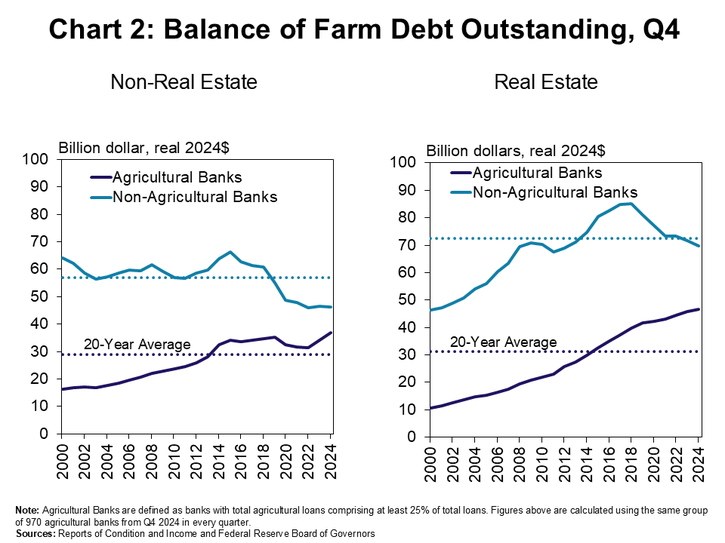

Strong loan growth pushed debt levels at agricultural banks well above historic averages. When adjusted for inflation, real estate and non-real estate loan balances at agricultural banks ended the year considerably above the average of the past 20 years (Chart 2). Production loans at non-agricultural lenders were largely flat and remained well below average while real estate debt among those banks dropped to the lowest level since 2012.

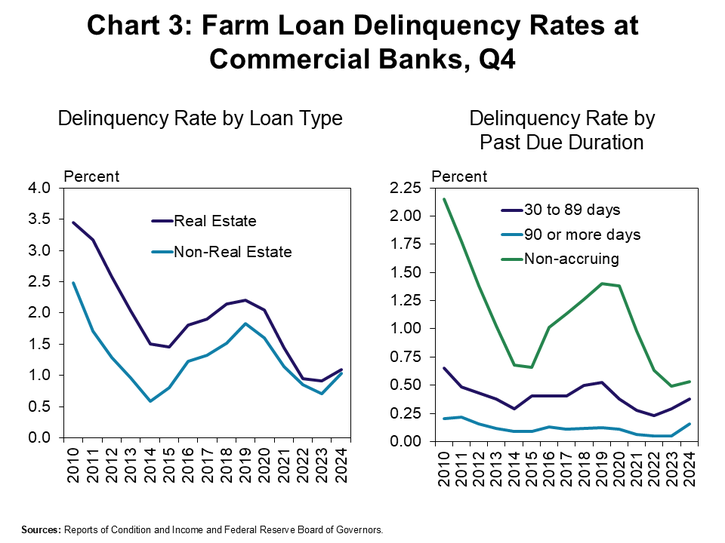

As farm debt grew and conditions in the farm economy weakened, delinquency rates increased modestly from historic lows. Delinquency rates for both real estate and non-real estate loans climbed above 1%, reversing the downward trend that began in late 2020 (Chart 3, left panel). While non-accruing debt increased only slightly, the volume of loans that were delinquent for more than 90 days more than tripled compared to the previous year, albeit from historically low levels.

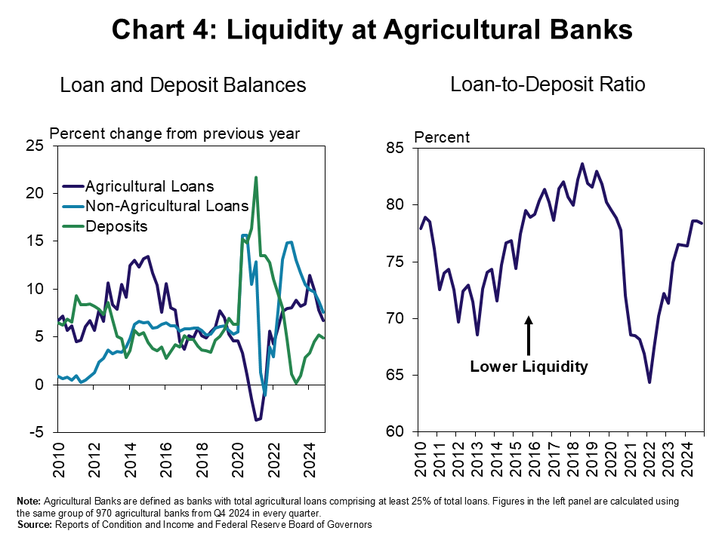

Liquidity at agricultural banks moderated alongside strong loan growth. Agricultural and non-agricultural loans grew by an average of 7% over the past year, slowing from double-digit growth in 2023 and early 2024 (Chart 4, left panel). Meanwhile, deposit growth remained strong at 5% year-over-year. The continued rise in outstanding loans relative to deposits further contributed to declining liquidity at agricultural banks (Chart 4, right panel).

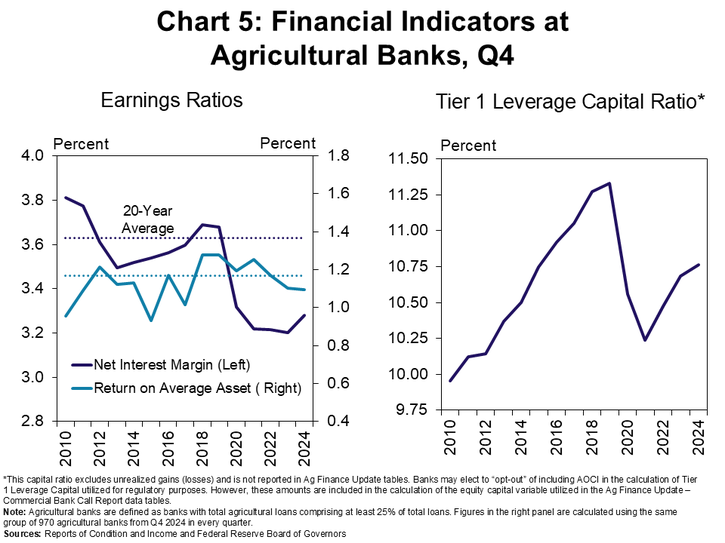

Interest margins improved along with loan growth and supported bank capital ratios. Despite a 2% increase in net interest margins over the past year and stable returns on average assets, earnings for agricultural banks remained below historical averages (Chart 5, left panel). Nevertheless, core capital levels continued to grow, underscoring the ability of agricultural banks to navigate possible economic uncertainties ahead (Chart 5, right panel).

Commercial Bank Call Report Historical Data

Commercial Bank Call Report Data Tables

About Commercial Bank Call Report Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Francisco Scott

Senior Economist