The U.S. payments industry migrated to EMV chip-card technology in 2015 with the aim to mitigate card-present fraud. Since then, however, payment card fraud has continued to climb. From 2015 to 2021, both card-present and card-not-present fraud rates increased for non-prepaid debit card transactions processed by dual-message networks (such as Visa and Mastercard). During this period, the card-not-present fraud rate also increased for single-message networks (such as Star, NYCE, and Pulse)._

In its latest biennial report on debit cards published in December 2025, the Board of Governors of the Federal Reserve System provides debit card fraud statistics for 2023. In this Payments System Research Briefing, I update earlier research on card-present and card-not-present fraud rates through 2023 and examine how these fraud losses were allocated across issuers, merchants, and cardholders.

Card-present fraud rates and loss allocation

To examine how counterfeit, lost-or-stolen, and overall card-present fraud rates have changed more recently, I use data included in the Federal Reserve Board’s biennial reports on debit cards._ Similar to Hayashi (2025a, b), I calculate fraud rates separately for non-prepaid debit card transactions processed by dual-message networks versus single-message networks. I define the counterfeit, lost-or-stolen, or overall card-present fraud rate as the value of counterfeit, lost-or-stolen, or card-present fraud divided by the value of card-present transactions. (I follow a similar method to define and calculate card-not-present fraud rates in the next section.)

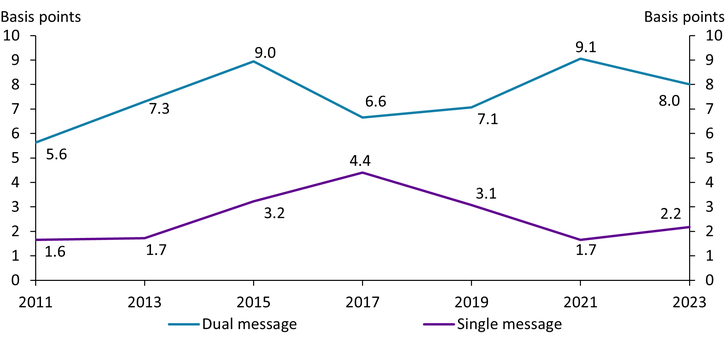

Data through 2023 show that previous trends on counterfeit fraud have reversed. Although EMV chip-card technology was intended to mitigate card-present fraud from counterfeit cards, the counterfeit fraud rate declined only for single-message networks, not dual-message networks, from 2015 to 2021 (Hayashi 2025a). However, these trends changed during the 2021–23 period. As Chart 1 shows, from 2021 to 2023, the counterfeit fraud rate declined for dual-message networks (blue line) by 0.9 basis points but increased for single-message networks (purple line) by 0.5 basis points. Despite these changes, the counterfeit fraud rate remains significantly higher for dual-message networks than for single-message networks in 2023 (8.0 basis points versus 2.2 basis points)._

Chart 1: Counterfeit fraud rates of non-prepaid debit cards

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

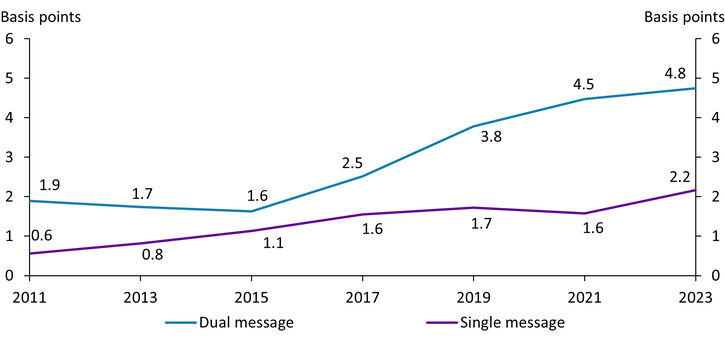

The lost-or-stolen fraud rate of non-prepaid debit cards continued its previous trend. From 2015 to 2021, the lost-or-stolen fraud rate of non-prepaid debit cards increased for both types of networks (Hayashi 2025a). Chart 2 reveals that from 2021 to 2023, this upward trend for both networks has continued. For dual-message networks, the lost-or-stolen fraud rate remains significantly lower than the counterfeit fraud rate shown in Chart 1 (4.8 basis points versus 8.0 basis points in 2023); in contrast, the lost-or-stolen fraud rate for single-message networks has been almost the same as the counterfeit fraud rate since 2021.

Chart 2: Lost-or-stolen fraud rates of non-prepaid debit cards

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

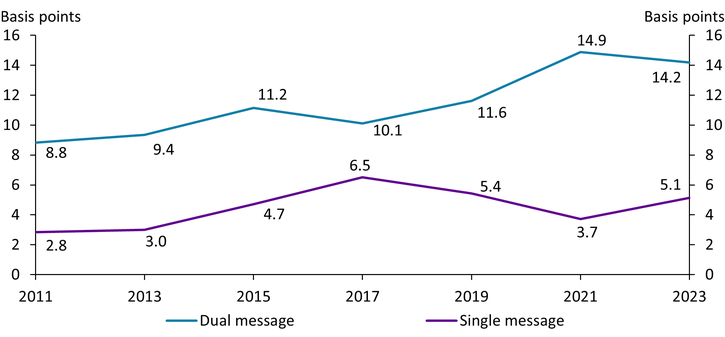

Like the counterfeit fraud rate, trends for the overall card-present fraud rate—which combines counterfeit, lost-or-stolen, and other (fraud rates (such as card-not-received)—also reversed in 2021–23. From 2015 to 2021, the card-present fraud rate increased for dual-message networks but decreased for single-message networks (Hayashi 2025a). However, Chart 3 shows that from 2021 to 2023, the card-present fraud rate decreased for dual-message networks (blue line) by 0.7 basis points but increased for single-message networks (purple line) by 1.4 basis points. Again like the counterfeit fraud rate, the overall card-present fraud rate remains significantly higher for dual-message networks than for single-message networks in 2023 (14.2 basis points versus 5.1 basis points). However, even the single-message networks’ card-present fraud rate in 2023 was substantially higher than the card-present fraud rate of both credit and debit cards in other countries, such as Australia (1.0 basis points) and the European Economic Area (0.7 basis points)._

Chart 3: Card-present fraud rates of non-prepaid debit cards

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

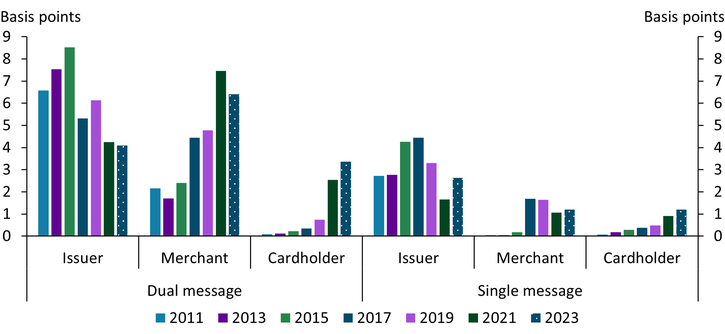

I use the Federal Reserve Board’s 2023 report on debit cards to reexamine how fraud losses have been allocated across issuers, merchants, and cardholders. I calculate each party’s fraud loss rates for non-prepaid debit card transactions for both single- and dual-message networks. The sum of the three parties’ fraud loss rates should be the same as (or very close to) the card-present fraud rates shown in Chart 3.

The left side of Chart 4 shows fraud loss rates from card-present fraud for each of the three parties for dual-message networks from 2011 through 2023. The recent decline in the overall card-present fraud rate reduced loss rates for issuers and merchants, but not cardholders. From 2021 (dark green bars) to 2023 (patterned blue bars), the fraud loss rate declined by 1.0 basis points for merchants and 0.2 basis points for issuers. However, the fraud loss rate for cardholders increased by 0.8 basis points, continuing its upward trend.

Chart 4: Card-present fraud loss rates of non-prepaid debit cards by party

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

The right side of Chart 4 shows that the recent increase in the overall card-present fraud rate for single-message networks led to increased loss rates for all three parties: issuers, merchants, and cardholders. From 2021 to 2023, the fraud loss rate increased by 1.0 basis points for issuers, by 0.3 basis points for cardholders, and by 0.1 basis points for merchants. Although the fraud loss rate had been lowest for cardholders through 2021, both cardholders and merchants had the same fraud loss rate in 2023 of 1.2 basis points.

Card-not-present fraud rate and loss allocation

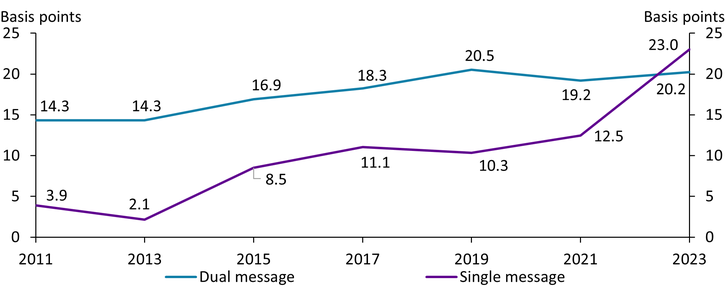

Data through 2023 show that the upward trend of card-not-present fraud rates has continued. Over the 2011–21 period, the card-not-present fraud rate of non-prepaid debit cards increased gradually, though the rate declined slightly for dual-message networks from 2019 to 2021 (Hayashi 2025b). However, Chart 5 shows that from 2021 to 2023, the card-not-present fraud rate increased for dual-message networks, almost offsetting the 2019–21 decline. More notable is a sizable increase—more than 10 basis points—in the card-not-present fraud rate for single-message networks from 2021 to 2023. Because of this increase, the card-not-present fraud rate for single-message networks surpassed that of dual-message networks for the first time._ Both types of networks’ card-not-present fraud rates were higher than the 2023 card-not-present fraud rates of credit and debit cards in other countries, such as Australia (19.2 basis points) and the European Economic Area (10.3 basis points)._

Chart 5: Card-not-present fraud rates of non-prepaid debit cards

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

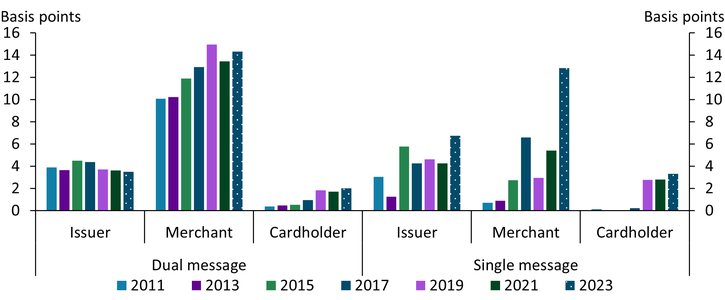

The recent increase in the card-not-present fraud rate for dual-message networks increased the fraud loss rate for merchants and cardholders, but not issuers. As the right side of Chart 6 shows, from 2021 to 2023, the fraud loss rate increased by 1.1 basis points for merchants and by 0.3 basis points for cardholders but declined by 0.1 basis points for issuers.

Chart 6: Card-not present fraud loss rates of non-prepaid debit cards by party

Sources: Board of Governors of the Federal Reserve System and author’s calculations.

The recent significant increase in the card-not-present fraud rate for single-message networks increased the fraud loss rate for all three parties. The right side of Chart 6 shows that the fraud loss rate more than doubled for merchants, from 5.4 basis points in 2021 to 12.8 basis points in 2023. The increase was more modest for issuers (by 2.5 basis points) and cardholders (by 0.5 basis points).

Conclusion

Newly available 2023 fraud data show a continuation of some trends and a reversal of others. Card-not-present fraud rates of non-prepaid debit cards have continued to climb. In contrast, card-present fraud rates have reversed their previous trend, declining for dual-message networks and increasing for single-message networks. The data clearly show an upward trend in cardholders’ fraud loss rates for both card-present and card-not-present transactions across both types of networks. Recent research finds that financially vulnerable consumers are more likely to experience financial fraud and ultimately incur fraud losses (Routh and Toh 2025). Uncovering which types of consumers are more likely to experience debit card fraud and incur fraud losses may help explain why cardholders’ fraud loss rates have been increasing and inform efforts to mitigate them.

Endnotes

-

1 See Hayashi (2025a, b) for analysis through 2021.

-

2 In these reports, fraud information was provided by debit card issuers subject to Regulation II’s interchange fee cap. These issuers’ cards have accounted for more than two-thirds of non-prepaid debit card transactions in value.

-

3 Card-present transactions of debit cards in value were almost evenly split between single- and dual-message networks in 2023 (47 percent versus 53 percent).

-

4 Author’s calculations based on fraud data reported in AusPayNet (2024) and European Banking Authority and European Central Bank (2024) and on payment data reported by the Reserve Bank of Australia.

-

5 Single-message networks accounted for only 5 percent of card-not-present transactions of debit cards in value in 2023.

-

6 Author’s calculations based on fraud data reported in AusPayNet (2024) and European Banking Authority and European Central Bank (2024) and on payment data reported by the Reserve Bank of Australia.

Article Citation

Hayashi, Fumiko. 2026. “New Data on Card-Present and Card-Not-Present Fraud Rates in the United States.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, February 25.

Fumiko Hayashi is a vice president at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

References

AusPayNet (Australian Payments Network). 2024. “External LinkAustralian Payment Fraud 2024: January-December 2023 Data.” September 26.

Board of Governors of the Federal Reserve System. 2025. “External Link2023 Interchange Fee Revenue, Covered Issuer Costs, and Covered Issuer and Merchant Fraud Losses Related to Debit Card Transactions.” October.

European Banking Authority and European Central Bank. 2024. “External Link2024 Report on Payment Fraud.” August 1.

Hayashi, Fumiko. 2025a. “External LinkDid Card-Present Fraud Rates Decline in the United States After the Migration to Chip Cards?” Federal Reserve Bank of Kansas City Payments System Research Briefing, February 12.

———. 2025b. “External LinkCard-Not-Present Fraud Rates in the United States After the Migration to Chip Cards.” Federal Reserve Bank of Kansas City Payments System Research Briefing, May 21.

Routh, Aditi, and Ying Lei Toh. 2025. “External LinkHow Do Consumers’ Fraud Experiences Vary with Their Financial Vulnerability?” Federal Reserve Bank of Kansas City Payments System Research Briefing, October 8.

Fumiko Hayashi is a vice president at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author