Core banking systems are the backbone of the products and services that depository institutions (DIs)—including banks and credit unions—offer their customers. Core systems provide DIs primary services such as account and customer management, deposit and withdrawal processing, loan processing, and finance and accounting. Core systems also often provide ancillary services, such as payment processing and customer support (Alcazar and others 2024). Most DIs rely on core banking services providers for their core systems and ancillary services, so DIs’ ability to modernize their core systems largely depends on how responsive core providers are to DIs’ needs. This Payments System Research Briefing examines the market structure surrounding core providers and its potential effects on DIs. A forthcoming Briefing will explore the role of core providers in facilitating the adoption and broad use of instant payments.

Market concentration in the core services market

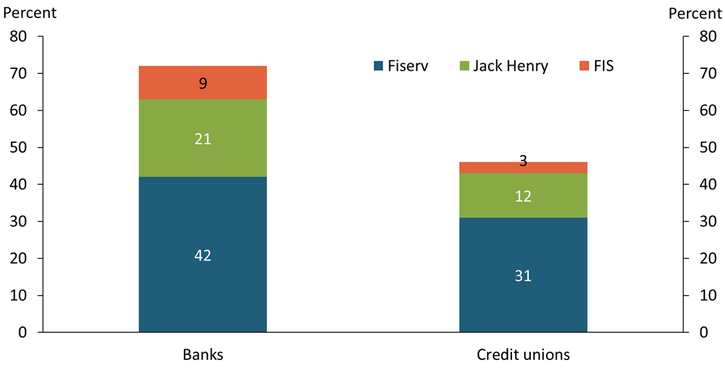

The core services market is highly concentrated, as the “Big Three” core providers—FIS, Fiserv, and Jack Henry and Associates (Jack Henry)—have sizable market shares. Chart 1 shows the shares of banks and credit unions the Big Three serve according to recent surveys (ABA 2023; Chilingerian and Schafer 2020). Collectively, the Big Three served more than 70 percent of banks surveyed in 2022 and nearly half of credit unions surveyed in 2020. Individually, Fiserv serves the largest share of DIs: 42 percent of banks and 31 percent of credit unions use a Fiserv core platform such as Premier, Precision, DNA, or Cleartouch. Jack Henry serves 21 percent of banks and 12 percent of credit unions across core platforms such as SilverLake, CIF 20/20, Core Director, or Symitar. And FIS serves 9 percent of banks and 3 percent of credit unions using a FIS core platform such as Horizon or IBS.

Chart 1. Market share of the Big Three core providers (percent)

Sources: American Bankers Association, Chilingerian and Schafer (2020), and Callahan & Associates.

Although each of the Big Three core providers serve both banks and credit unions, their client bases vary based on client type and asset size. FIS primarily serves large and midsized banks, while Jack Henry primarily serves small banks. Fiserv serves some large and midsized banks as well as many small banks. According to a 2019 Aite report, FIS is the leading core provider for large banks, serving 78 banks with assets greater than $10 billion (Barry and Albertazzi 2019). However, FIS serves less than 20 large credit unions with assets greater than $1 billion, while Jack Henry and Fiserv serve 160 and 140, respectively (Chilingerian and Schafer 2020). Fiserv and Jack Henry are also the top two core providers for midsized credit unions with assets between $250 million and $1 billion. For small credit unions (with assets less than $250 million), Fiserv is again the top provider, while Jack Henry and FIS are outside the top three.

Although the Big Three dominate the core services market, other players have nontrivial market share. The market is less concentrated for credit unions in particular, suggesting credit unions have more core provider options than banks. Indeed, many credit unions use core providers that specifically serve credit unions. FedComp served 10 percent of credit unions surveyed in 2020, and other core providers such as CompuSource Systems, FLEX Credit Union Technology, and Sharetec Systems served more credit unions than FIS (Chilingerian and Schafer 2020). Some credit unions also use the UK-based Finastra, one of several core providers that also serve modest shares of banks. Finastra served 3 percent of banks in 2022, while long-standing domestic firms CSI and COCC served 7 percent and 3 percent of banks, respectively (ABA 2023). In addition to Finastra, other global core providers, such as Accenture, Oracle, and TCS, have entered the U.S. market, although they have not yet accumulated even modest market share. Some domestic firms such as Corelation and Nymbus are emerging as next-generation core providers that could increase competition, but only if they are not acquired by larger counterparts, as were other providers. For example, Finxact, a prominent emerging next-generation core provider, was acquired by Fiserv in 2022 and integrated into Fiserv’s fintech business segment (Fiserv 2022).

Vertical presence of core providers

The Big Three core providers have significant footholds in markets that are vertically related to the core services market. While Jack Henry offers services that are closely related to core services, Fiserv and FIS serve broader related markets, including payment processing services for merchants and governments, card network services, and banking-as-a-service (BaaS)._ As part of their ancillary services, the Big Three firms offer payment processing services to DIs, including transaction authorization, verification of funds, and gateway services that connect DIs to payment operators and networks. These services support DI processing of automated clearinghouse (ACH), wire, check, card, and ATM transactions (Alcazar and others 2024). The Big Three providers also enable DIs to implement instant payment capabilities, including connectivity to the two instant payment infrastructures—the Federal Reserve’s FedNow and the Clearinghouse’s Real-Time Payments (RTP)—as well as Early Warning Service’s Zelle, a person-to-person (P2P) payment service solution. After the introduction of Zelle, Fiserv and FIS discontinued or deemphasized their own P2P solutions (Popmoney and People Pay, respectively). In contrast, Jack Henry acquired Payrailz, a cloud-based payment technology company, and launched a standalone P2P solution that leverages Payrailz’s digital payment platform in 2022 (Jack Henry 2022).

FIS and Fiserv have a large presence in the merchant processing market. FIS’s Worldpay and Fiserv processed, respectively, the second- and fourth-largest volumes of merchant transactions worldwide in 2022 (Nilson Report 2023). Fiserv became the fourth-largest merchant processor worldwide in 2020 after its 2019 acquisition of First Data, a leading global merchant processor (Nilson Report 2020). The two firms have recently pursued different strategies in their merchant businesses. Following investor complaints, FIS announced a spin-off of Worldpay in February 2023 to separate merchant solutions from other business lines (FIS 2023). As of February 2024, FIS had completed the spin-off of Worldpay while maintaining ongoing collaboration with them, with FIS’s CEO announcing that “Worldpay will remain an important distribution center for us” (Stewart 2024)._ In contrast, Fiserv plans to strengthen its merchant business. In January 2024, Fiserv applied for a special-purpose banking charter to become a merchant-acquirer limited-purpose bank in the state of Georgia. If approved, the designation would allow Fiserv to directly interact with card networks instead of operating through a sponsor bank, giving Fiserv more control over the payment process and driving down their costs (Woodward 2024).

FIS and Fiserv also have large presences in the card network service and government benefit markets. FIS owns two single-message, PIN-based debit card networks—NYCE and CULIANCE (formerly CU24)— out of 12 nationally. Before its recent spin-off of Worldpay, FIS also owned another network, Jeannie. Fiserv owns two networks, Accel and Star; the latter was acquired through its 2019 acquisition of First Data. For Electronic Benefit Transfer (EBT) cards that disburse Supplemental Nutrition Assistance Program (SNAP) benefits, FIS serves as a contractor for 15 states and Washington, DC._ For state government benefit disbursement programs via prepaid card, Fiserv serves 13 states, following its recent expansion to California (Berry 2024).

Fiserv and FIS have recently expanded their presence to the new BaaS market. In March 2023, Fiserv announced its partnership with Central Payments, a BaaS provider, to offer fintechs, enterprise businesses, and other firms access to a BaaS platform, relationships with sponsor banks, management of unique payment products and services, and compliance oversight. The partnership “will help any business become a fintech without the need to add the staff or expertise to manage the program in-house” (Fiserv 2023). FIS acquired Bond, a startup that specializes in BaaS and embedded finance, in 2023; and this acquisition is expected to expand FIS’s portfolio of solutions for fintechs (Azevedo and Lunden 2023; PYMENTS 2023)._

Effects of core provider market structure on DIs

The Big Three providers have grown their respective footprints through mergers and acquisitions and evolved to support an increasing variety of processing needs, enabling them to become “one-stop shops.” This market structure may give the Big Three firms market power over DIs of all sizes, which may be enhanced by the necessity of core and ancillary services and the high costs of switching core platforms.

Whether core providers leverage their market power is difficult to assess; however, DIs’ lower satisfaction with the Big Three firms may be an indication of their market power when considered alongside other factors. According to the 2022 ABA survey, nearly half of banks (46 percent) that used the Big Three were either extremely or somewhat dissatisfied with their core provider, compared with about a quarter of banks (27 percent) that used a smaller core provider (ABA 2023). Notably, nearly 80 percent of large banks (with assets greater than $5 billion) were dissatisfied or neutral, compared with about 40 percent of small banks (with assets less than $500 million). The surveyed banks noted that their core providers were ineffective in delivering quality, timely customer support, integration with third parties, and data maintenance. In contrast, core providers assessed the effectiveness of their own performance much higher. The ABA concludes that this gap in effectiveness assessment between the banks and core providers “is the root cause of bank leaders’ dissatisfaction with core providers” (ABA 2023).

Potentially unfair contract terms may be another indication of core provider market power. In addition to their core providers’ performance, many DIs are not satisfied with their contract terms. According to the 2020 ABA survey, more than half of the surveyed banks cited “fees charged for implementation with third-party providers” and “fees charged for upgrades” as the most problematic contract provisions (ABA 2020). Although the share of banks that cited these two provisions shrank in the 2022 ABA survey, the two provisions continued to be among the top three most problematic (ABA 2023). These fees can hinder a DI’s ability to innovate without incurring significant costs or penalties (BFKN 2021). Moreover, some contracts stipulate that the core provider has sole ownership of any work related to core functioning, including software, source code, modifications, and enhancements. These contract provisions not only increase the fees incurred by DIs but also limit DIs’ options to modify their core or ancillary services (FIS 2011; Fiserv 2015). Opacity in contract terms is another problem for DIs. Fees for making changes or ending contracts early (such as deconversion fees) may not be clear (Nelson Mullins 2020). The limited transparency of contract timelines or of specific services to be provided has also raised concerns among DIs. Core services contracts have been described as “complex” and “tome-like,” as they can be hundreds of pages long with contract duration details that are difficult to decipher by less sophisticated clients or hidden among other terms (Chopra 2022). Some banks have brought legal action against core providers for what they perceived as unfair contract lengths and “coercive” renewal strategies (Silva 2020).

Smaller banks and credit unions may be particularly susceptible to the effects of core providers’ contract terms. Smaller DIs often struggle to absorb the costs charged by their core providers to implement updates or adopt new payment rails. Indeed, despite their scarce resources, smaller DIs may be charged the same amount as their larger counterparts for implementing new services._ In some cases, smaller DIs may incur further charges if their core providers use a bundling agreement requiring them to use the core provider’s other services to access the new rails or update._

Despite these challenges, most DIs have longstanding relationships with their core providers, and survey data suggest few DIs plan to switch. According to the 2022 ABA survey 20 percent of banks have been with their core providers for five to 10 years, and 61 percent of banks have been with their core provider for more than 10 years. Across all contract lengths, 37 percent of banks reported that they were somewhat likely to renew their contracts rather than switch providers, while 24 percent of banks reported that they were extremely likely to renew (ABA 2023). This loyalty may be partly due to contract terms that lock banks into long relationships, exclusive dealing arrangements, or the substantial costs of switching to another provider. The difficulties associated with modernizing a core platform may also play a role (Alcazar and others 2024).

With few options for switching providers or negotiating better contracts, industry leaders and government agencies have expressed concerns about the Big Three core providers’ market power. In 2016, banking and legal executives formed a coalition to negotiate with the Big Three core providers and ancillary vendors for “necessary, equitable concessions.”_ In 2022, CFPB Director Rohit Chopra expressed concerns about the lopsided power dynamic between smaller DIs and the Big Three core providers (and Finastra), citing cost increases, inflexibility, declining services, and unfair contract terms. Chopra noted that there could be downstream effects on relationship banking and consumers due to smaller DIs’ dependency on core providers to serve communities (Chopra 2022).

The Big Three core providers are responding to these criticisms and to the apparent trend toward cloud-based, next-generation core products (Alcazar and others 2024). In 2020, FIS began offering a simplified pricing and contracting model for certain community banks and credit unions, which “eliminates required term lengths, liquidated damages, and exclusivity requirements and provides clearly defined fees around deconversion services” (FIS 2020). In this model, DIs choose from pre-defined bundled solutions comprising a range of core processing and ancillary services with a flat monthly subscription fee (Banking Exchange 2020). FIS has also begun offering the “Modern Banking Platform,” which leverages the cloud, component-based cores, and APIs, relieving some of the burdens of bundling and certain exclusivity agreements (FIS 2019). More recently, Fiserv has started offering a cloud-native, open API-first core platform through its acquisition of Finxact._ Jack Henry has also started making use of APIs to give their DI clients access to third-party services, offering integration with more than 200 vendors. Additionally, Jack Henry announced plans to unbundle its services and put them on the public cloud with third-party services, allowing its community and regional bank clients to have more choice in the services they use (Marek 2022).

Summary

The “Big Three” core providers—Fiserv, FIS, and Jack Henry—not only dominate the U.S. core services market but also have a large presence in related vertical markets, such as card network services; payment processing services for DIs, merchants, or governments; and BaaS. Although this market structure may give the Big Three firms market power over DIs, it is difficult to assess whether the Big Three are leveraging this power. Many Dis are unsatisfied with core providers’ performance and contract terms, motivating banking and legal executives to form a coalition to assist DIs to better negotiate with their core providers. CFPB has also expressed its concerns about the large core providers’ power in the system and its effects on DIs and their customers. The Big Three providers are responding to these developments by simplifying contract terms, unbundling services, and offering new core services to meet DIs’ needs. As more DIs modernize their core systems and implement new services such as instant payments and BaaS, market structure dynamics surrounding core providers may continue to evolve.

Endnotes

-

1 BaaS describes a model in which DIs integrate their digital banking services seamlessly into the products of other nonbank businesses. Under this model, a DI allows a nonbank business to market the DI’s products—such as mobile banking accounts, debit cards, loans, and payment services—under the nonbank business’s name.

-

2 FIS will retain a 45 percent non-controlling equity stake in Worldpay (FIS 2024).

-

3 -

4 Embedded finance refers to financial solutions that are offered by consumer-facing businesses in conjunction with the purchase of goods and services. The purpose is to eliminate the need for consumers to leave the merchant’s channel to make payments, borrow money, or procure insurance associated with the purchase. BaaS enables embedded finance as well as the provision of financial services by nonbanks (Lehman 2022).

-

5 This information is obtained through authors’ interviews with a few community banks.

-

6 Bundling and tying agreements are not inherently anticompetitive but can be deemed as such when a firm has market power in the tying product or artificially closes an otherwise open system. See External LinkFederal Trade Commission Guide to Antitrust Laws Tying the Sale of Two Products.

-

7 -

8

References

ABA (American Bankers Association). 2023. “Closing the Effectiveness Gap: ABA Core Platforms Survey.Closing the Effectiveness Gap: ABA Core Platforms Survey.” February.

———. 2020. “ABA 2020 Core Processor Survey Results.” October.

Alcazar, Julian, Sam Baird, Emma Cronenweth, Fumiko Hayashi, and Ken Isaacson. 2024. “External LinkCore Banking Systems and Options for Modernization.” Federal Reserve Bank of Kansas City Payments System Research Briefing, February 28.

Azevedo, Mary Ann, and Ingrid Lunden. 2023. “External LinkFIS Acquirers Banking-as-a-Service Startup Bond.” TechCrunch, June 9.

Banking Exchange. 2020. “External LinkFIS Launches Community Banking Subscription Service.” August 25.

Barry, Christine, and David Albertazzi. 2019. “External LinkAIM Evaluation: The Leading Providers of U.S. Core Banking Systems.” Aite, February (obtained at Fiserv’s website for free).

Berry, Kate. 2024. “External LinkCalifornia Benefits Contract Shifts to Fiserv from Bank of America.” January 26.

BFKN (Barack Ferrazzano Kirschbaum & Nagelberg LLP). 2021. “External LinkBFKN Alert: Preparing to Negotiate Core Processing Agreements.” February 17.

Chilingerian, Natasha and Tim Schafer. 2020. “External LinkMarket Share Overview: Who’s Providing Credit Union Core Systems in 2020?” Credit Union Times, December 21.

Chopra, Rohit. 2022. “External LinkDirector Chopra's Opening Remarks to the Community Bank and Credit Union Advisory Councils.” Consumer Financial Protection Bureau, April 7.

FIS (Fidelity National Information Services). 2024. "External LinkFIS Completes Sale of Majority Stake of Worldpay to GTCR.” Press release, February 1.

———. 2023. “External LinkFIS Announces Plans to Spin Off Merchant Business.” Press release, February 13.

———. 2020. “External LinkFIS Offers Simplified Contracting and Pricing Model for Qualifying Community Banks and Credit Unions.” Press release, May 1.

———. 2019. “External LinkModern Banking Platform.”

———. 2011. “External LinkFIS Core System Processing Services Agreement with Independent Bank Corp.”

Fiserv. 2023. “External LinkFiserv and Central Payments Deliver Modern Issuing Capabilities to Fintechs and Financial Institutions.” Press release, March 20.

———. 2022. “External LinkFiserv Completes Acquisition of Finxact.” Press release, April 1.

———. 2015. “External LinkFiserv Master Agreement with Pioneer Financial Services.”

Jack Henry. 2022. “External LinkJack Henry Launches Standalone, Real-Time Person-to-Person (P2P) Payments.” Press release, October 25.

Lehman, Matt. 2022. “External LinkEmbedded Finance vs. Banking as Service (BaaS): What’s the Difference?” Ring Central Blog, March 29.

Marek, Lynne. 2022. “External LinkJack Henry to Unbundle Services, Put Them on the Public Cloud.” Banking Dive, February 11.

Nelson Mullins. 2020. “External LinkFear of Commitment: Negotiating Core Contracts and the Importance for Banks of Planning Strategically.” Presented at the Georgia Bankers Association Operations & Technology Conference, February 26–28.

Nilson Report. 2023. “Largest Merchant Acquiring Portfolios Worldwide.” Nilson Report, no. 1250, October.

———. 2020. “Top 150 Merchant Acquirers Worldwide.” Nilson Report, no. 1183, September.

PYMNTS. 2023. “External LinkReport: FIS Acquired Bond Financial Technologies to Grow Embedded Finance.” June 9.

Silva, Aaron. 2020. “External LinkMillington Bank Sues FIS Over Coercive Contract Tactics.” Golden Contract Coalition, June 9.

Stewart, John. 2024. “External LinkPost Worldpay, FIS Looks to Share Buybacks And Growth in Digital Payments.” Digital Transactions, February 26.

Woodward, Kevin. 2024. “External LinkLower Costs Plus More Control Could Be Part of Fiserv’s Ambition for a Bank Charter.” Digital Transactions, January 16.

Julian Alcazar and Sam Baird are payments specialists at the Federal Reserve Bank of Kansas City, Emma Cronenweth is a senior payments policy analyst at the Federal Reserve Bank of Chicago, Fumiko Hayashi is a senior policy advisor at the Federal Reserve Bank of Kansas City, and Ken Isaacson is a senior vice president at the Federal Reserve Bank of Cleveland. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Chicago, Cleveland, or Kansas City, or the Federal Reserve System.

Authors

Julian Alcazar

Senior Payments Specialist

Sam Baird

Associate Payments Specialist