In recent years, interest in central bank digital currencies (CBDCs) has been increasing around the globe. Although only a few central banks have thus far implemented a retail CBDC, many banks have been assessing the need within their economies. According to the Bank for International Settlements, the share of central banks that have been researching, experimenting, or developing CBDCs grew from about 70 percent in 2018 to over 85 percent in 2020 (Boar and Wehrli 2021). The vast majority of these banks have focused on retail (or general-purpose) CBDCs._

In this Briefing, we examine what motivations, if any, central banks have identified for retail CBDCs. In general, we find that central banks in emerging markets and developing economies (EMDEs), such as China, Mexico, and Nigeria, tend to be more enthusiastic about retail CBDCs and have clearer motivations for their issuance relative to central banks in advanced economies, such as Canada, Japan, and Singapore._ Indeed, several central banks in EMDEs have made progress in developing or implementing a retail CBDC; in contrast, many central banks in advanced economies have only undertaken technical research on a retail CBDC, and most have not developed plans to implement one.

Retail CBDCs in emerging markets and developing economies (EMDEs)

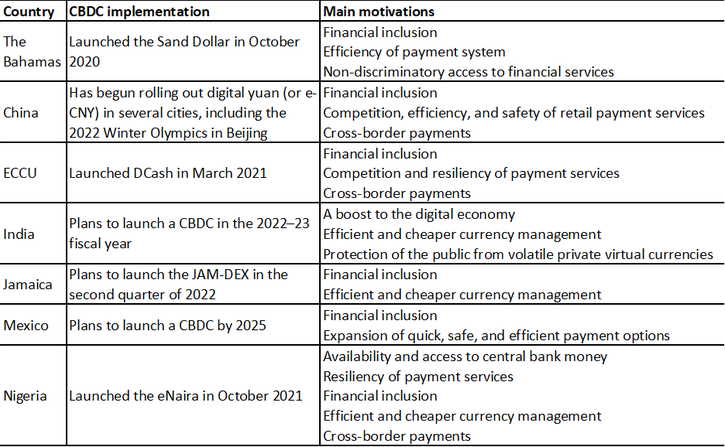

Central banks in many EMDEs view a retail CBDC as a viable solution to problems in their economies and payment systems. Table 1 shows that central banks in seven EMDEs have implemented or plan to implement a retail CBDC: the Bahamas, China, the Eastern Caribbean Currency Union (ECCU), India, Jamaica, Mexico, and Nigeria.

Table 1: Retail CBDC implementation and motivation by central banks in seven EMDEs

Note: Motivations are listed in the order they are given in the respective central banks’ papers, speeches, or press releases.

Sources: Central Bank of The Bahamas (2019), People’s Bank of China (2021), Eastern Caribbean Central Bank (2021), Shankar (2021), Bank of Jamaica (2021), Rodríguez (2022), and Central Bank of Nigeria (2021).

Although policy goals for a retail CBDC vary by country, Table 1 shows a few common motivations include promoting financial inclusion; enhancing payment system efficiency, competition, security, or resiliency; and improving cross-border payments. These motivations are consistent with unique challenges of EMDEs relative to advanced economies. In EMDEs, many consumers lack access to financial services, rely heavily on cash, and tend not to use electronic payment systems, which are often less developed.

All central banks except the Reserve Bank of India have explicitly identified financial inclusion as one of their main policy goals for a retail CBDC. Individuals without a bank account, who are considered excluded from the financial system, make up a relatively large share of the population in these countries. In Mexico and Nigeria, the share of unbanked individuals in the adult population (age 15 or older) is about 60 percent (World Bank Group 2017). In the Bahamas, China, India, and Jamaica, the unbanked share is about 20 percent, but still higher than the share in advanced economies (World Bank Group 2017; International Monetary Fund 2019; Laidley 2022)._ For unbanked individuals who lack internet access or a smartphone, some of these central banks have developed offline solutions to address financial exclusion with their CBDC, such as the physical CBDC payment card introduced by the Central Bank of The Bahamas (Mastercard 2021)._

All seven central banks in Table 1 also cited enhancing the efficiency, competition, security, or resiliency of their payment systems as another main motivation for implementing a CBDC. Most of these countries’ economies are based on cash, which tends to involve higher operational costs (Bank of Jamaica 2021; Shankar 2021). A retail CBDC may improve efficiency by reducing the demand for physical cash, easing currency management in turn. In countries where electronic payments have already been widely adopted, such as China, electronic payment services may be highly concentrated within a few large private-sector providers, so a retail CBDC may increase competition and lower transaction costs or increase choices for merchants and consumers. In countries where the electronic payments system is not fully developed, a retail CBDC could be more secure than existing electronic payment processes and add resiliency to the overall payment system.

Some EMDE central banks have also listed cross-border payments as motivation for instituting a retail CBDC. Although most of these banks have focused on domestic use for their retail CBDCs, a few have enabled or envisioned a CBDC for cross-border payments, especially with neighboring countries. For example, the central banks in Nigeria and the ECCU perceive a CBDC as a means of achieving cheaper and faster international remittances (Central Bank of Nigeria 2021; BIS and others 2021). In addition, the People’s Bank of China has been piloting the use of their CBDC, the e-CNY, for retail cross-border payments between China and Hong Kong (Gkritsi 2021).

Retail CBDCs in advanced economies

No central bank in an advanced economy has yet introduced a retail CBDC, which may reflect relatively limited scope for retail CBDCs to improve the payments systems in these countries. In advanced economies, most consumers use less cash and already have access to financial services and well-developed payment systems. Accordingly, only a few central banks have identified key motivations for a retail CBDC; others have conducted studies but not found a compelling case for implementing a CBDC under current circumstances. Table 2 lists the key motivations or the contingency plans for a retail CBDC stated by several central banks in advanced economies, most of which have made significant progress in assessing the need for a retail CBDC.

Table 2: Motivations or contingency plans for a retail CBDC in eight advanced economies

Sources: Lowe (2021), Bank of Canada (2020), ECB (2020), Bindseil, Panetta, and Terol (2021), Bank of Japan (2020), Bache (2020), MAS Economic Policy Group (2021), Söderberg (2019), Bank of England (2020), and Economic Affairs Committee (2022).

Sweden’s Riksbank has long been considering a retail CBDC and has identified three key motivations: payments access, resiliency, and competition. Because cash use has declined rapidly in Sweden, a priority policy goal of the “e-krona” is to ensure broad access to payments, especially for those who may be adversely affected by a cashless society (Söderberg 2019). The e-krona could potentially serve as an additional backup to existing digital payments and facilitate competition among digital payment systems currently offered by the private sector. The final decision on whether to issue an e-krona, however, is up to the national legislature._

In an October 2020 report, the European Central Bank (ECB) describes seven scenarios that could induce the Eurosystem to issue a digital euro (ECB 2020)._ A subsequent paper by ECB researchers mentions two key motivations (Bindseil, Panetta, and Terol 2021). First, a digital euro could be a monetary anchor for payments in the digital era, as public confidence in private money (such as commercial bank money) depends on its conversion at par with central bank money. Second, a digital euro could give the Eurosystem monetary strategic autonomy, which has declined as payment instruments controlled and supervised from abroad (such as payment cards with a Visa or Mastercard logo) have gained dominance in the European retail payment market.

Central banks in Canada, Japan, and Norway have not found a compelling case nor an acute need for a retail CBDC but are preparing in case one is needed in the future. In February 2020, the Bank of Canada concluded that there is no compelling case at this time and outlined a contingency plan for implementing a retail CBDC under two scenarios: should cash use decline to the point where it can longer be used in a wide range of transactions, or should a private cryptocurrency or stablecoin make substantial inroads, raising concerns about privacy and handing control of payments to private companies. In October 2020, the Bank of Japan stated that while it currently has no plan to issue a CBDC, it could issue one if cash use significantly declines and private digital money is not an adequate substitute; if a CBDC is necessary to support private payment services; or if a CBDC is necessary to develop stable and efficient payment and settlement systems suitable for a digital society. And in November 2020, Norway’s Norges Bank stated that there is “no acute need to introduce a CBDC,” despite a rapid decline in cash use in Norway (Bache 2020). Norges Bank, however, has a contingency plan to introduce a CBDC if the payment system evolves in a different direction than currently predicted.

Central banks in Australia and Singapore have not found a strong public policy case for a retail CBDC but are open to the possibility of one in the future. The Reserve Bank of Australia expects that digital wallets, which continue to replace physical wallets, will contain new digital forms of money that could include a retail CBDC (Lowe 2021). The Monetary Authority of Singapore (MAS) believes that a well-designed retail CBDC could have future value in preserving the benefits of generally accessible public money and that a CBDC could mitigate risks to credit creation, financial stability, and monetary policy (MAS Economic Policy Group 2021). MAS also considers supporting the growth of Singapore dollar-denominated stablecoins as an alternative policy option.

In March 2020, the Bank of England set out seven potential benefits of a retail CBDC._ However, in January 2022, the United Kingdom’s parliament committee concluded that they “have yet to hear a convincing case” for a retail CBDC (Economic Affairs Committee 2022). The committee argued that while a retail CBDC may provide some advantages, it would also present significant challenges. The committee also argued that a CBDC could not be designed to support the seven stated benefits equally well and that alternative solutions might pose fewer risks. The committee recommended that the Joint Taskforce (created by Bank of England and HM Treasury) identify the most significant long-term problem it believes a CBDC may solve when it publishes the use cases for a possible CBDC in 2022 and compare CBDCs against alternative means of achieving the same aim.

Conclusion

Several EMDEs have implemented CBDCs primarily to promote financial inclusion and improve their payments systems. Several advanced economies have made significant progress in assessing the case for a retail CBDC; though a few have identified motivations for implementing a CBDC, most have not found a compelling case to do so.

Many other central banks are still at an early stage in exploring motivations for a retail CBDC, including the Federal Reserve, which recently published a report aiming to foster a public discussion with CBDC stakeholders on the potential benefits and risks of CBDCs (Board of Governors of the Federal Reserve System 2022). Through research and public dialogue, these central banks may increasingly identify motivations for a retail CBDC or scenarios in which a retail CBDC may be warranted. The motivations and scenarios will likely vary across countries, as each country has a unique set of opportunities and challenges in its economy and payment system.

Endnotes

-

1 Retail (or general-purpose) CBDCs are available for public use (like cash), while wholesale CBDCs are mainly for use by financial institutions to settle interbank accounts. In 2020, around 90 percent of central banks that had engaged in CBDC work focused either on retail CBDCs only or on both retail and wholesale CBDCs.

-

2 The International Monetary Fund’s World Economic Outlook classifies countries into advanced economies, emerging markets, and developing economies, using various criteria including per capita income level, export diversification, and degree of integration into the global financial system (International Monetary Fund 2022).

-

3 Data are not available for the ECCU. In India, although 80 percent of the adult population had a bank account in 2017, only 52 percent of bank account holders used the account in 2016. In China, Mexico, and Nigeria, the share of bank account holders who used the account is much higher (around 80 percent).

-

4 See Auer and others (2022) for other design features of CBDCs intended to address barriers to financial inclusion.

-

5 A government inquiry into the need for a CBDC is currently underway in Sweden, with findings due November 30, 2022.

-

6 Five scenarios are related to core central bank functions, and two scenarios are related to the broader objectives of the European Union.

-

7 These potential benefits are: (1) supporting a resilient payments landscape, (2) avoiding the risk of new forms of private money creation, (3) supporting competition, efficiency, and innovation in payments, (4) meeting future payment needs in a digital economy, (5) improving the availability and usability of central bank money, (6) addressing the consequences of a decline in cash, and (7) enabling better cross-border payments.

References

Auer, Raphael, Holti Banka, Nana Yaa Boakye-Adjei, Ahmed Faragallah, Jon Frost, Harish Natarajan, and Jermy Prenio. 2022. “External LinkCentral Bank Digital Currencies: A New Tool in the Financial Inclusion Toolkit?” World Bank Group and Bank for International Settlement Financial Stability Institute Insights on Policy Implementation, no. 41, April.

Bache, Ida Wolden. 2020. “External LinkCentral Bank Digital Currency and Real-Time Payments.” Speech at Finance Norway’s Payments Conference, Norges Bank. November 5.

Bank of Canada. 2020. “External LinkContingency Planning for a Central Bank Digital Currency.” February 25.

Bank of England. 2020. “External LinkCentral Bank Digital Currency: Opportunities, Challenges and Design.” Discussion paper. March.

Bank of Jamaica. 2021. “External LinkBOJ Prepares for Central Bank Digital Currency.” CBDC Information Press Release, March 22.

Bank of Japan. 2020. “External LinkThe Bank of Japan’s Approach to Central Bank Digital Currency.” October 9.

Bindseil, Ulrich, Fabio Panetta, and Ignacio Terol. 2021. “External LinkCentral Bank Digital Currency: Functional Scope, Pricing and Controls.” European Central Bank Occasional Paper Series, no. 286, December.

BIS (Bank for International Settlements), Committee on Payments and Market Infrastructures, Innovation Hub, International Monetary Fund, and World Bank Group. 2021. “External LinkCentral Bank Digital Currencies for Cross-Border Payments: Report to the G20.” July.

Boar, Codruta, and Andrews Wehrli. 2021. “External LinkReady, Steady, Go? Results of the Third BIS Survey on Central Bank Digital Currency.” Bank for International Settlements, BIS Papers no. 114, January.

Board of Governors of the Federal Reserve System. 2022. “External LinkMoney and Payments: The U.S. Dollar in the Age of Digital Transformation.” January.

Central Bank of The Bahamas. 2019. “External LinkProject Sand Dollar: a Bahamas Payments System Modernization Initiative.” Public Updates, December 24.

Central Bank of Nigeria. 2021. “External LinkDesign Paper for the eNaira.”

Eastern Caribbean Central Bank. 2021. “External LinkFirst Digital EC Currency (DCash) Transaction Completed Successfully.” February 18.

ECB (European Central Bank). 2020. “External LinkReport on a Digital Euro.” October.

Economic Affairs Committee. 2022. “External LinkCentral Bank Digital Currencies: A Solution in Search of a Problem?” House of Lords, January 13.

Gkritsi, Eliza. 2021. “External LinkChina, Hong Kong Enter Second Phase of Cross-Border Digital Yuan Trials: Report.” CoinDesk, December 9.

International Monetary Fund. 2022. “External LinkWorld Economic Outlook (WEO), Frequently Asked Questions.” April 19.

———. 2019. “External LinkThe Bahamas.” IMF Country Report no. 19/201, July.

Laidley, Andrew. 2022. “External LinkThe Cost of Being Unbanked.” Jamaica Observer, February 3.

Lowe, Philip. 2021. “External LinkPayments: The Future?” Address to the Australian Payments Network Summit 2021, Reserve Bank of Australia, December 9.

MAS (Monetary Authority of Singapore) Economic Policy Group. 2021. “External LinkA Retail Central Bank Digital Currency: Economic Considerations in the Singapore Context.” November.

Mastercard. 2021. “External LinkMastercard and Island Pay Launch World’s First Central Bank Digital Currency-Linked Card.” Press Release, February 17.

People’s Bank of China. 2021. “External LinkProgress of Research and Development of E-CNY in China.” July.

Rodríguez, Victoria. 2022. “External LinkComparecencia ante el Senado de la Repúblic (in Spanish).” Speech before the Senate Finance Committee, Bank of Mexico, April 21.

Shankar, T Rabi. 2021. “External LinkCentral Bank Digital Currency – Is This the Future of Money.” Keynote address at the webinar organized by the Vidhi Centre for Legal Policy, New Delhi, July 22.

Söderberg, Gabriel. 2019. “External LinkThe E-Krona – Now and for the Future.” Sveriges Riksbank, Economic Commentaries, no. 8, October.

World Bank Group. 2017. “External LinkThe Global Findex Database 2017 (Data).”

Fumiko Hayashi is a policy and research advisor at the Federal Reserve Bank of Kansas City. Ying Lei Toh is an economist at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Fumiko Hayashi

Vice President