The Federal Reserve has a clearly defined dual mandate to achieve price stability and ensure full employment. But successfully fulfilling this mandate requires policymakers to gauge two unobservable variables: the natural rate of interest that would achieve both stable inflation and full employment, and the unemployment rate consistent with full employment. Most estimates of the natural rate of interest, known as r*, and the natural unemployment rate, u*, rely on quarterly data. However, r* and u* may respond to much more frequent and sudden news about underlying economic conditions.

To provide more timely estimates of r* and u*, we introduce the KC Fed Model-Based Natural Rate of Interest and Natural Unemployment Rate. Our measure of r* follows Lubik and Matthes (2015), who estimate a quarterly proxy for r* by forecasting the real policy rate five years ahead (additional methodological details are available in the technical appendix). Unlike Lubik and Matthes, however, our monthly model of r* replaces real output growth with the unemployment rate._ We extend the Lubik and Matthes method to generate u* for each month, using the five-year-forward forecast of unemployment. Forecasting five years ahead allows our measures to avoid incorporating any economic shocks causing unemployment, inflation, and monetary policy to temporarily deviate from their mandate-consistent values.

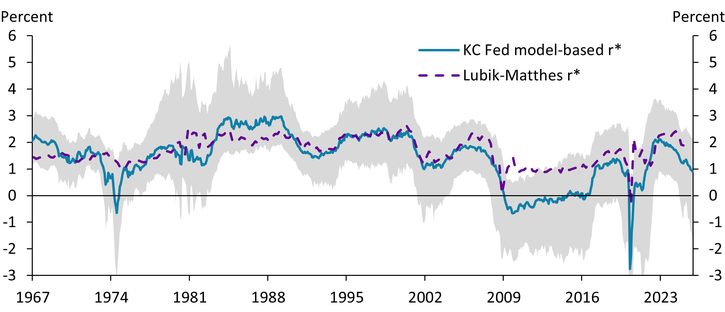

Chart 1 plots our measure of r* along with the Lubik-Matthes measure. From 1967 through the 2007–09 global financial crisis (GFC), the two series track closely, and the Lubik-Matthes series lies within our natural rate’s 68 percent credible set. However, the series diverge from the onset of the Great Recession until the pandemic. Both measures show r* fell in 2009 after the GFC, suggesting that monetary policy was less expansionary than implied by rates alone. However, the unemployment rate was slower to recover than real GDP growth, causing our r* (blue line) to fall even more than the Lubik-Matthes measure. Because the Federal Reserve’s dual mandate includes achieving full employment, our lower estimate of r* may have been more informative for policymakers at the time.

Chart 1: KC Fed Model-Based Natural Rate of Interest (r*) Compared with Lubik-Matthes

Notes: Blue line is the median of estimates of the five-year-ahead forecast of the real federal funds rate from 100,000 simulations. Gray shaded area shows the upper and lower bounds for 68 percent of estimates from these simulations. Estimates cover January 1967 through November 2025.

Sources: Federal Reserve Bank of Richmond and authors’ calculations.

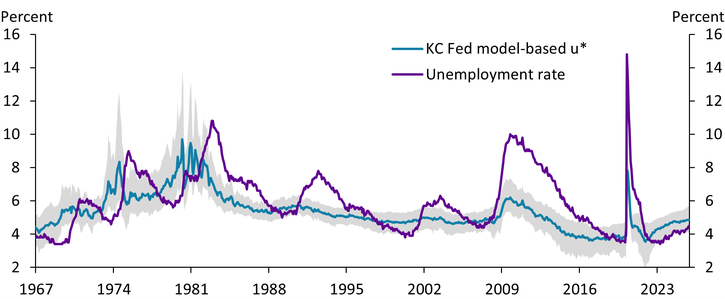

Our monthly measure of u*—the unemployment rate consistent with full employment—provides further evidence that labor markets remained slack following the GFC. Indeed, Chart 2 shows that while our u* measure (blue line) increased at the onset of the GFC, unemployment (purple line) increased significantly more. For the following decade, a gap persisted between the two measures despite low policy rates, suggesting the labor market remained loose even as growth recovered._

Chart 2: KC Fed Model-Based Natural Unemployment Rate Compared with Current Unemployment Rate

Notes: Blue line is the median of estimates of the five-year ahead forecast of the unemployment rate from 100,000 simulations. Gray shaded area shows the upper and lower bounds for 68 percent of estimates from these simulations. Estimates cover January 1967 through November 2025.

Sources: U.S. Bureau of Labor Statistics (Haver Analytics) and authors’ calculations.

More recently, our measure of u* suggests that while labor markets were initially slack at the onset of the pandemic in 2020, they tightened quickly over the next two years. In fact, our estimate suggests that unemployment was below its natural rate by mid-2022, when labor markets were tighter than at any time since the late 1990s. Notably, inflation had increased to levels not seen in decades at this point. By mid-2023, the unemployment rate had increased and entered the credible set of u*, and inflation moderated.

The Federal Reserve is tasked with setting interest rates to achieve price stability and full employment. Determining whether the economy is at full employment and what policy rate balances the two sides of the dual mandate is complicated by frequent changes in the economy that affect the natural unemployment rate and natural rate of interest. Our monthly measures of r* and u* are jointly estimated from a flexible statistical model and will provide policymakers a timely signal of changes in these critical unobservable variables.

Download Materials

Click here to view the KC Fed Model-Based Natural Rate of Interest and Natural Unemployment Rate.

Endnotes

-

1 Importantly, in periods such as the 2010s, output growth recovered significantly faster than unemployment while inflation remained below target, which affects our estimates of how tight labor markets and monetary policy were in that decade.

-

2 This dynamic is shared by other recent estimates of u*, such as the stable-price unemployment rate estimated by Bok and Petrosky-Nadeau (2022).

Article Citation

Glover, Andrew, and Johnson Oliyide. 2026. “Introducing New Monthly Estimates of the Natural Rate of Interest and Natural Unemployment Rate.” Federal Reserve Bank of Kansas City, Economic Bulletin, February 2.

References

Bok, Brandyn, and Nicolas Petrosky-Nadeau. 2022. “External LinkEstimating Natural Rates of Unemployment.” Federal Reserve Bank of San Francisco, Economic Letter, no. 2022-14, May.

Lubik, Thomas A., and Christian Matthes. 2015. “External LinkCalculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches.” Federal Reserve Bank of Richmond, Economic Brief, no. 15-10, October.

Andrew Glover is a research and policy advisor at the Federal Reserve Bank of Kansas City. Johnson Oliyide is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Andrew Glover

Research and Policy Advisor