Colorado, which opened recreational stores in January 2014, has the longest-running legalized marijuana market in the United States. Since stores opened, Colorado’s marijuana sector has exhibited rapid growth of firms, total sales, tax revenues and employees. However, the strong growth of marijuana sales and new business entrants began to slow in 2017 and 2018, suggesting the industry may be moving into a more mature stage of development. However, because sales are up sharply this year, it may be too soon to declare the marijuana sector’s growth has slowed permanently. This issue of the Rocky Mountain Economist provides an update on the economic impacts of the marijuana industry in Colorado and evaluates signs of maturation within this industry nearly six years after the first recreational marijuana storefronts opened.

The State of the Cannabis Industry in the Nation

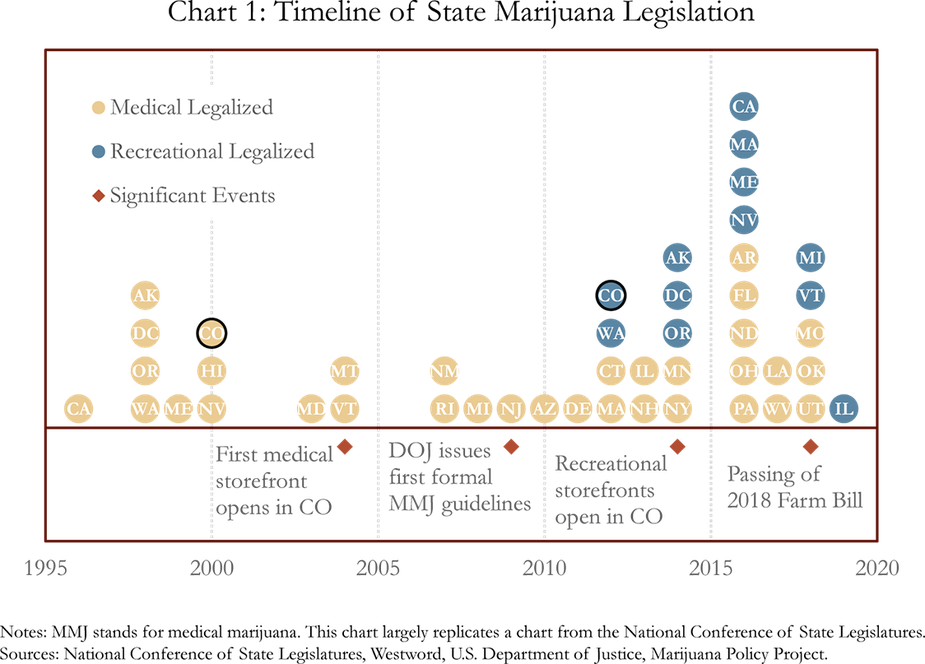

Historically, the legality of cannabis—a generalized term used to describe the plants from which both marijuana and industrial hemp are derived—has evolved over time in the United States. In the late 1800s, industrial hemp was a common crop, grown predominantly in Kentucky.i However, opposition to the plant grew in the early 1910s as individual states slowly began to ban cannabis and the federal government put restrictions on the plant through the Uniform State Narcotic Drug Act in 1935 and the Marihuana Tax Act of 1937.ii With the exception of a brief campaign in the early 1940s to boost hemp production to create goods needed for World War II efforts, cannabis remained heavily restricted until it was made federally illegal in 1970.iii

Despite being illegal at the federal level, California in 1996 became the first state to legalize medical marijuana.iv Marijuana legislation initially was slow to expand across the United States. In recent years, however, states have been adopting legislation to create legal marijuana markets at a rapid pace (Chart 1).v This coincided with changes in enforcement policy from the U.S. Department of Justice (DOJ). Starting in 2009, the DOJ began to issue guidance to defer marijuana regulation and enforcement to states that had legalized medical marijuana, which helped establish confidence in the sustainability of the industry.vi,vii As of 2019, 33 states and the District of Columbia have legalized medical marijuana and 11 states and the District of Columbia have legalized recreational marijuana.viii Other states have decriminalized the first-time possession of small quantities of marijuana or legalized the limited sale and use of low-THC CBD oil, a non-psychoactive product from the cannabis plant often used for medical purposes.ix

Industrial hemp remained illegal federally until late 2018, when the 2018 Farm Bill legalized it with regulation and oversight from the U.S. Department of Agriculture (USDA). While some states had authorized industrial hemp pilot programs for research through the 2014 Farm Bill, hemp growers were subject to strict regulations and were not offered federal support such as crop insurance. Starting in 2020, farmers in states that have received USDA approval will be allowed to grow industrial hemp for production purposes as long as the final hemp cultivation contains less than 0.3 percent THC. Any crop that exceeds 0.3 percent THC will be recognized as marijuana and therefore is federally illegal and must be destroyed under USDA guidelines.x

The next few sections of this article will discuss trends in the Colorado marijuana industry to provide an economic update on the market and evaluate any early signs of maturation.

Marijuana Sales and Business Activity in Colorado

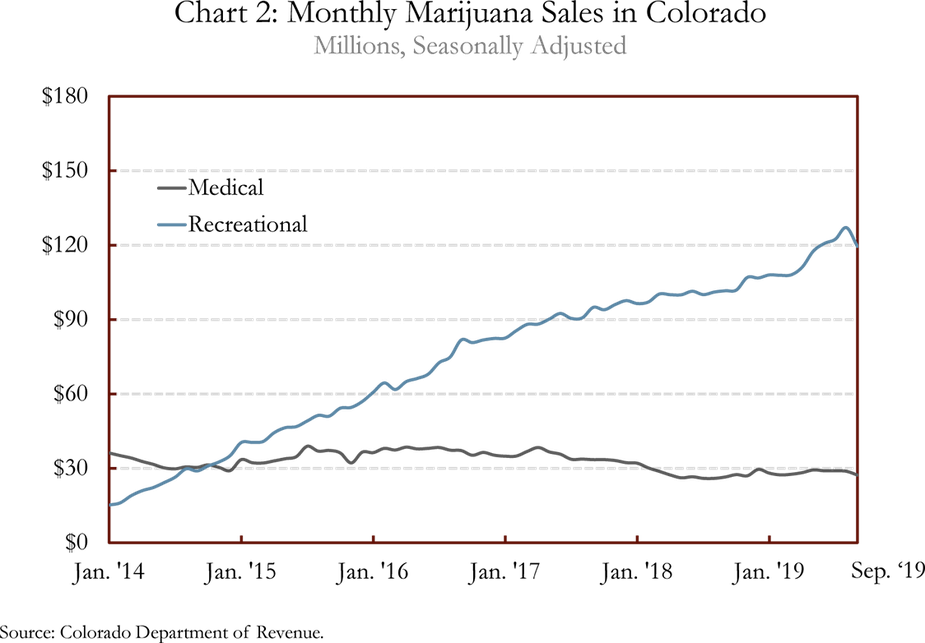

Marijuana sales boomed in Colorado starting in early 2014 with the opening of the first recreational storefronts.xi The marijuana industry experienced substantial growth in recreational sales through mid-2017, with sales doubling twice between 2014 and 2016 (Chart 2). Medical sales grew slightly during this same period, but remained relatively flat compared with the rapid growth seen in the recreational market. Medical sales peaked toward the end of 2016, while recreational sales continued to rise. However, the pace of growth in recreational sales slowed from year-over-year changes above 100 percent in early 2015 to below 20 percent in the latter part of 2017 before reaching a low of about 7 percent growth in the fall of 2018.

This slowdown in recreational marijuana sales coupled with slowly declining medical marijuana sales initially indicated that the market potentially was reaching a steady state level of demand. However, beginning in April 2019, sales for both medical and recreational marijuana picked up. Recreational marijuana sales surged through the late summer months this year and reached an all-time peak in monthly sales in August, resulting in a year-to-date increase of 16.1 percent compared with the previous year.xii Medical marijuana sales also gained slightly this year and year-over-year growth was positive in April for the first time since late 2016. While this level of monthly sales was not sustained in September 2019 for recreational or medical marijuana, total marijuana sales remained well above year-ago levels. Despite this rebound in sales growth, year-over-year sales growth of about 16 percent year-to-date in 2019 is much lower than the growth rates experienced in the first few years of legalized sales, and indicates growth in sales is moving toward a more sustainable, yet still robust, path.

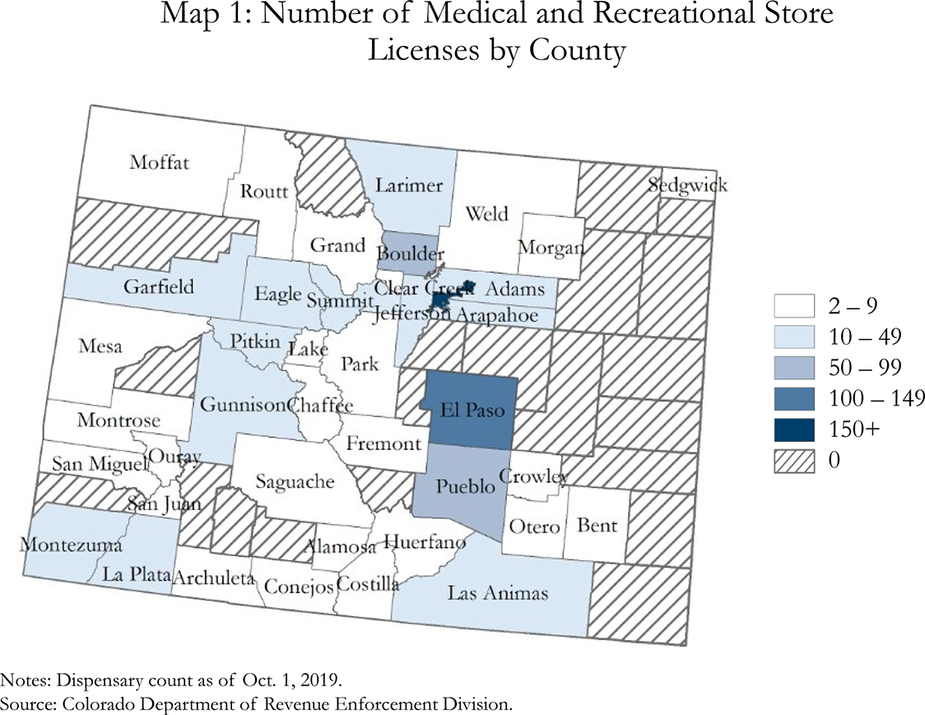

Marijuana storefronts historically have been concentrated in Front Range counties (Map 1).xiii Since legalization, Denver County has had the highest number of medical and recreational storefronts in the state, estimated to be over 330 as of October. El Paso County has the next highest number with just over 120 stores.xiv Outside the Front Range, marijuana storefronts more frequently are found in counties with resort destinations such as Garfield County, which has just under 30 stores as of October, one-third of which are in Glenwood Springs. Though not typically viewed as a resort destination, Trinidad, in Las Animas County, also has a particularly high concentration of marijuana storefronts. Despite a population of just over 8,000, the city has an estimated 30 stores—most of which sell recreational marijuana—as of October.xv Due to Trinidad’s close proximity to Colorado’s southern border, the city’s marijuana industry is believed to have been boosted by interstate tourism, particularly from New Mexico and Texas.xvi

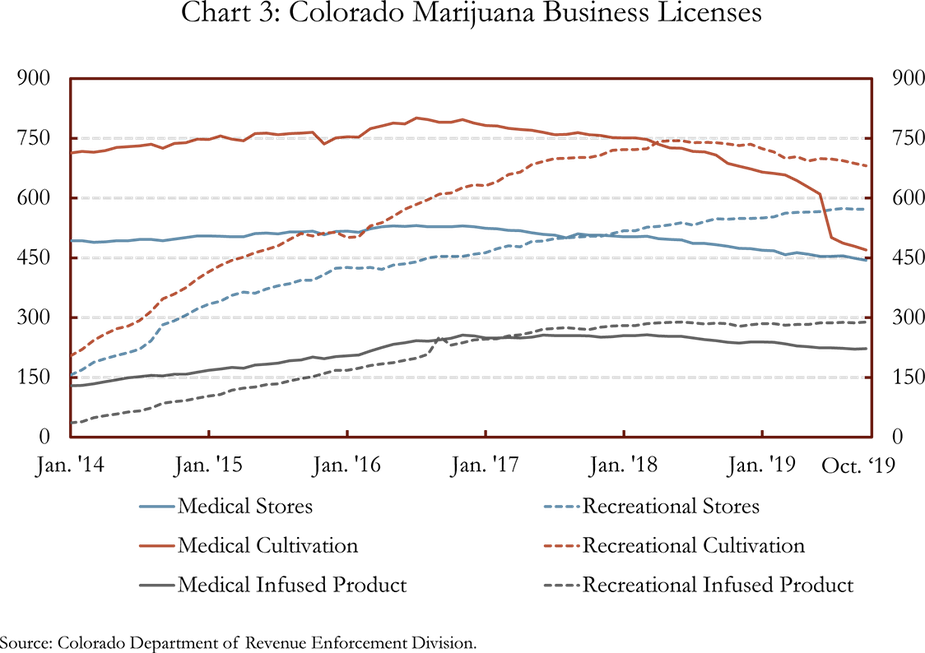

Similar to sales, licensing of marijuana businesses increased rapidly in the first few years after legalizing recreational marijuana, only to begin slowing more recently (Chart 3). Overall, the number of business licenses declined 9.6 percent in October compared with year-ago levels, with a majority of this drop driven by a decline in medical business licenses. Licenses for medical storefronts and cultivation began to decline after reaching peaks in mid-2016, while licenses for manufacturing medical-infused products began to decline in early 2018. Though recreational licensing has not seen the same large declines experienced by the medical industry, the number of licenses for storefronts and cultivation both have started to drop, while licenses for manufacturing infused products flattened out in recent months.

While declining business licenses may be indicative of a maturing market, a recent flurry of merger and acquisition activity may impact licensing numbers in the months to come. New legislation in Colorado loosened restrictions on out-of-state investment in marijuana businesses effective Nov. 1, 2019, which has sparked new cash flow for existing businesses.xvii This new cash flow, coupled with additional business-friendly legislation, such as allowing social consumption of marijuana in licensed spaces, suggests the number of marijuana businesses has the potential to expand despite recent declines in licenses.xviii

Recent Trends in Employment in the Colorado Marijuana Industry

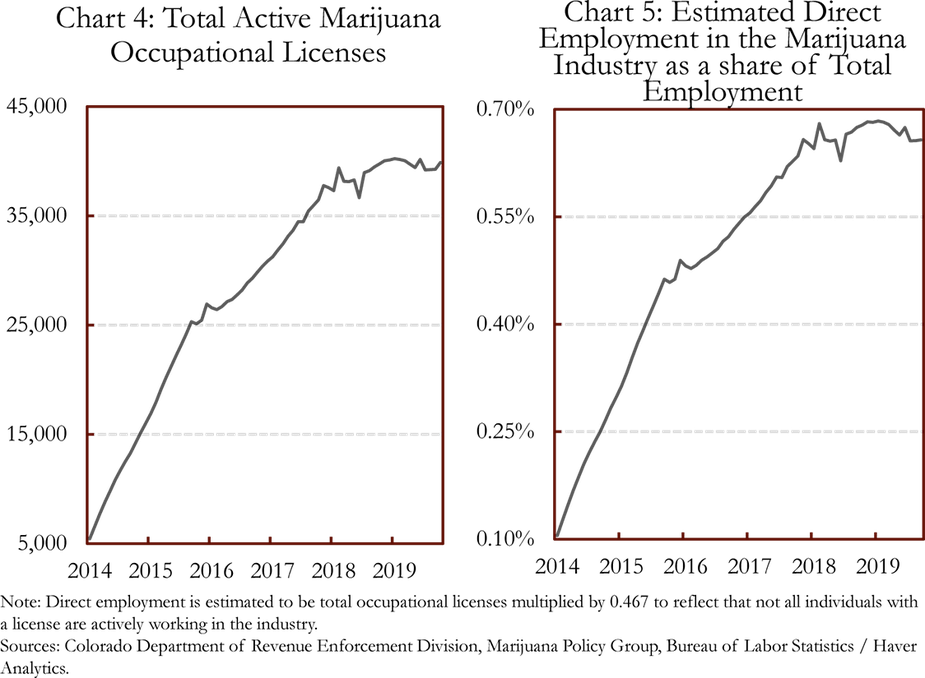

Along with California and Washington, Colorado is estimated to have one of the largest shares of marijuana employment in the United States with just under 40,000 active occupational licenses as of October (Chart 4).xix Despite declining marijuana business licensing, occupational licensing in the Colorado marijuana industry mostly has been unchanged since late 2018.xx However, the components of total occupational licensing have begun to shift. Support occupational licensing, which includes over 60 percent of occupational licenses, began to decline slightly in year-over-year terms starting in July, while key occupational licensing has continued to increase.xxi Employees with support occupational licenses typically represent entry-level staff marijuana positions, most commonly budtenders within dispensaries, while key occupational licenses are required for individuals who work in operational or managerial positions. A decline in licenses for support staff alongside rising key occupational licenses may imply that marijuana hiring is shifting more toward higher-skilled positions like store managers or master growers. However, employees are allowed to choose either license so it also may be that employees are opting for the key occupational license to increase their chance of promotion despite not being in a manager position.xxii

Not all individuals with an occupational license are working actively in the marijuana industry, and the Marijuana Policy Group estimates that direct employment in the sector is 0.467 times the number of occupational licenses. Using this estimate, direct employment in the marijuana industry comprised about 0.67 percent of total employment in Colorado in October, very similar to the 0.68 percent in October 2018 (Chart 5).xxiii,xxiv In the first few years after recreational marijuana stores opened, new jobs in the industry made up between 3 and 8 percent of all new jobs in Colorado each year. In recent years though, job growth in the industry has slowed and other industries in the state are growing much more quickly. This recent relative stability of the marijuana sector’s contribution to total employment in Colorado is not surprising given the decline in total business licenses over the past year. Looking ahead, sharp employment growth in the marijuana industry is unlikely without an increase in business licensing and creation of new job openings.xxv

Tax Collections in the Marijuana Industry

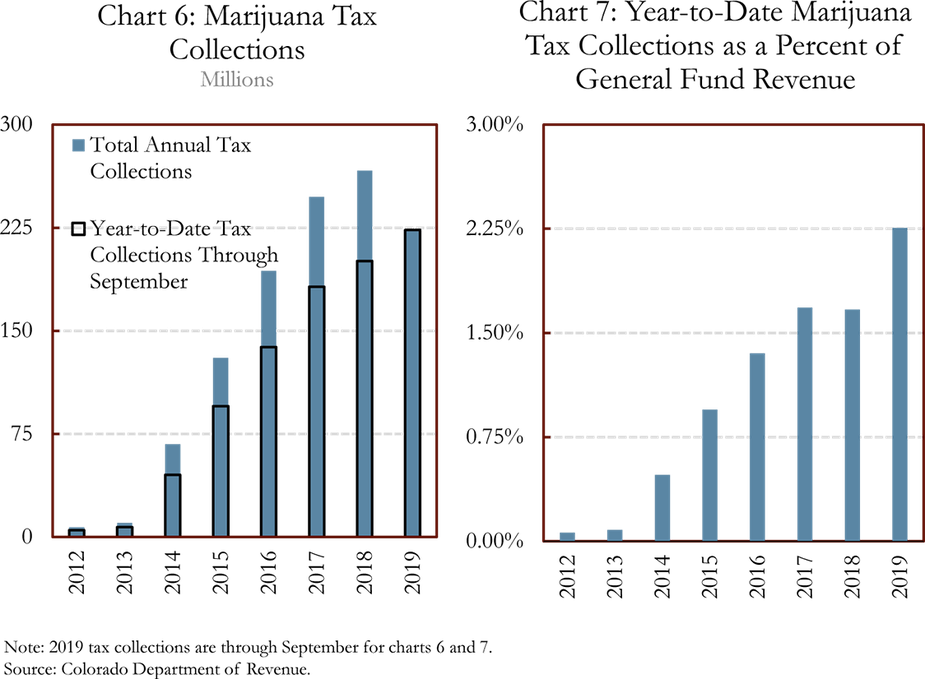

Since the legalization of recreational marijuana in Colorado, taxes imposed on the recreational sector have been substantially higher than those on the medical sector.xxvi Sales of both medical and recreational marijuana are subject to the regular 2.9 percent state sales tax. In addition, recreational sales face a 15 percent special sales tax and a 15 percent excise tax at the wholesale level.xxvii Additional local sales tax may apply on both sectors. Of the taxes collected from the special sales tax, 90 percent goes to the state government and the remaining 10 percent is redistributed to local governments. In general, tax collections from marijuana are distributed to a marijuana cash fund, the state general fund, school construction, a public schools fund and local governments.xxviii

In line with marijuana sales, tax collections have increased substantially each year since legalization, with tax collections growing faster than sales in 2017 due to an increase in recreational marijuana tax rates (Chart 6).xxix Tax collections through September were 11.3 percent above collections in 2018, making 2019 the first year since 2015 to have an increase in the rate of tax growth over the previous year. This increase in tax collections helped Colorado surpass $1 billion in total marijuana tax collections as of May 2019 since legalization in January 2014. Compared with general tax collections, year-to-date marijuana tax collections through September were about 2.3 percent of total general fund revenues in Colorado, an increase from 1.67 percent in 2018 (Chart 7). Though most marijuana tax collections do not go into the general fund, this comparison shows the relative scale of marijuana tax receipts to general tax collections.xxx

As marijuana tax collections in Colorado closely follow trends in marijuana sales, any maturation in sales may be reflected in tax collections. After a slowdown in the growth rate of tax collections in 2018, marijuana tax collections this year have increased more sharply. Thus, similar to sales, tax collections seemed to be showing some signs of maturation in the industry in 2018, but this year indicates the state is not yet seeing a consistent slowdown. That said, economists at the Colorado Legislative Council indicate they are skeptical that the current fast pace of growth in tax collections from marijuana can be sustained in the longer run.xxxi

Potential Costs of Marijuana Legalization

This article primarily has focused on the economic effects of the marijuana industry by measuring sales, taxes and similar metrics that mostly are straightforward to quantify. However, there also are potential costs from marijuana legalization such as those on health, crime and public welfare that are more difficult to measure. These factors also may affect the local economy and the general quality of life within a community, and therefore, are important to discuss despite the difficulty of quantifying their effects.xxxii

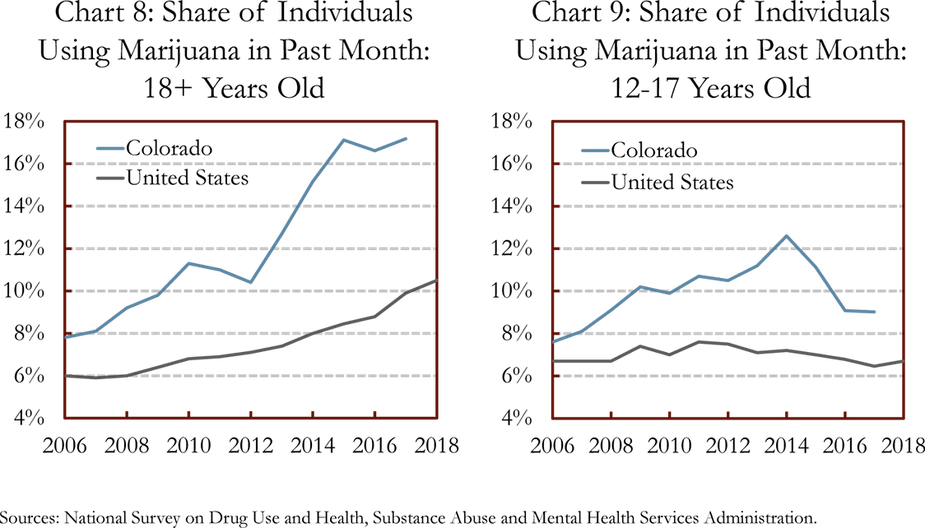

The National Survey on Drug Use and Health provides information on marijuana usage and shows that reported marijuana usage in Colorado consistently has been higher than the national average, both pre- and post-recreational legalization (Charts 8 and 9).xxxiii While reported usage increased sharply in Colorado after the legalization of recreational marijuana for both age groups of 18+ and 12 to 17, it recently dropped below pre-legalization levels in 2016 and 2017 for those ages 12 to 17.xxxiv,xxxv The heaviest user age group is ages 18 to 25 where 29.6 percent of respondents report having used marijuana in the past 30 days as of 2017.xxxvi

Crime related to marijuana as measured by marijuana offenses has fallen over the last six years by about half, due largely to a significant drop in marijuana possession offenses. Omitting possession offenses, marijuana-related crime has increased slightly from 1,416 offenses in 2012 to 1,582 in 2017.xxxvii Additionally, the number of DUI summons issued by Colorado State Patrol involving marijuana, which includes marijuana by itself or with other drugs or alcohol, increased 5 percent from 684 summons in 2014 to 719 in 2017, however, this is down slightly from its peak of 780 summons in 2016.xxxviii A separate report has shown that traffic deaths in Colorado when a driver tests positive for marijuana, either marijuana alone or in conjunction with other drugs or alcohol, has increased more than 150 percent from 75 deaths in 2014 to 115 in 2018 (18.2 percent of total traffic fatalities in 2018), which is down slightly from its peak level of 138 deaths in 2017.xxxix

Despite the legalization of marijuana in Colorado, there still are signs of black market activity within the state. Marijuana investigative seizures by Colorado task forces have increased from 425 pounds in 2014 to 12,150.2 pounds in 2018, down slightly from its peak of 14,691.9 pounds in 2017. In addition, the United States Postal Inspection Service has noted a rise of parcels containing marijuana from Colorado mailed to other states of 207 parcels before legalization in 2013 to 1,009 parcels in 2017.xl

It is important to continue to highlight that Colorado’s legalization of marijuana, as well as that of other states as mentioned earlier in this article, conflicts with federal law. This continues to create challenges for marijuana businesses, including access to the payment and banking systems. xli

Conclusion

While Colorado’s marijuana industry continues to expand, economic indicators in this sector are showing early signs of nearing a longer-term equilibrium. Though there still is room for growth, demonstrated by a spike in recreational marijuana sales during the summer months of 2019, the industry is unlikely to see rapid expansion in employment and business formation comparable to the growth during the first few years after legalization. That said, there are factors that may influence the pace of industry growth in Colorado, such as changes in marijuana legislation at the state and federal levels. While it is unclear if marijuana ever will be legalized at the federal level, a 2019 survey released by Pew Research Center showed that an estimated two-thirds of adults in the United States support the legalization of marijuana, up from just one-third of adults at the turn of the century.xlii This change in public perception represents a growing acceptance of the industry despite its potential costs.

Endnotes

i Thirteenth Census of the United States 1910: Volume 5. Agriculture. Retrieved from External Linkhttp://usda.mannlib.cornell.edu/usda/AgCensusImages/1910/05/01/1832/41033898v5ch07.pdf

ii NORML. Marijuana Law Reform Timeline. Retrieved from External Linkhttps://norml.org/shop/item/marijuana-law-reform-timeline

iii In 1970, cannabis was added to the newly-enacted Controlled Substances Act as a Schedule I drug, which made both marijuana and industrial hemp federally illegal. For more information, see External Linkhttps://norml.org/shop/item/marijuana-law-reform-timeline

iv Ibid.

v Warner, Joel. (2010, May 28). Medical marijuana timeline: What a long, strange trip it’s been. Retrieved from External Linkhttps://www.westword.com/news/medical-marijuana-timeline-what-a-long-strange-trip-its-been-5825542; Marijuana Policy Project (2019, October 19). 2019 Marijuana Policy Reform Legislation. Retrieved from External Linkhttps://www.mpp.org/issues/legislation/key-marijuana-policy-reform/; National Conference of State Legislatures. Marijuana Deep Dive. Retrieved from http://www.ncsl.org/bookstore/state-legislatures-magazine/marijuana-deep-dive.aspx

vi National Conference of State Legislatures. (2019, October 16). State Medical Marijuana Laws. Retrieved from http://www.ncsl.org/research/health/state-medical-marijuana-laws.aspx; Cole, James M. (2013, August 29) Guidance Regarding Marijuana Enforcement. Retrieved from External Linkhttps://www.justice.gov/iso/opa/resources/3052013829132756857467.pdf

vii Though DOJ guidance was rescinded in a January 2018 memo, legislation had been passed in 2014 to prevent federal funding from being used to prevent states from implementing and managing state medical marijuana programs. For more information, see: U.S. Department of Justice. (2018, January) Justice Department Issues Memo on Marijuana Enforcement. Retrieved from External Linkhttps://www.justice.gov/opa/pr/justice-department-issues-memo-marijuana-enforcement; Strekal, Justin. (2017, July 27). Senate Committee Passes Amendment to Protect Medical Marijuana. Retrieved from External Linkhttps://blog.norml.org/2017/07/27/senate-committee-passes-amendment-to-protect-medical-marijuana/

viii Governing. State Marijuana Laws in 2019 Map. Retrieved from External Linkhttps://www.governing.com/gov-data/safety-justice/state-marijuana-laws-map-medical-recreational.html

ix Ibid.

x The USDA provides additional information on the 2018 Farm Bill here: External Linkhttps://www.fsa.usda.gov/programs-and-services/farm-bill/index.

xi For additional information on potential costs of marijuana, see our previous Rocky Mountain Economist on Colorado’s marijuana market here: https://www.kansascityfed.org/publications/research/rme/articles/2018/rme-1q-2018.

xii In August 2019, non-seasonally adjusted recreational marijuana sales totaled $141,869,549. Total non-seasonally adjusted marijuana sales during August were $173,2019,859.

xiii Dispensary counts are estimated using current business licensing data from Colorado Department of Revenue Enforcement Division. For more information, see External Linkhttps://www.colorado.gov/pacific/enforcement/med-licensed-facilities

xiv The majority of stores in El Paso County are in Colorado Springs, which only issues business licenses to medical marijuana businesses. For more information, see External Linkhttps://www.colorado.gov/pacific/sites/default/files/Local%20Authority%20Status%20List%2001102019%20CURRENT%20VERSION.pdf

xv Population estimate as of July 1, 2018. Census Bureau.

xvi Wallace, Alicia. (2018, February 9). Recreational marijuana sales highest per capita in Colorado’s southern border towns. Retrieved from External Linkhttps://www.thecannabist.co/2018/02/09/colorado-marijuana-sales-southern-border/98669/

xvii Marijuana Business Daily. (2019, May 29) New Colorado law allows outsiders to invest in state’s marijuana industry. Retrieved from External Linkhttps://mjbizdaily.com/new-colorado-law-allows-outsiders-to-invest-in-states-marijuana-industry/

xviii Mitchell, Thomas. (2019, May 2) Marijuana Consumption and Hospitality Businesses Passes Legislature. Retrieved from External Linkhttps://www.westword.com/marijuana/colorado-legislature-approves-marijuana-cafes-lounges-and-social-use-areas-11331200

xix Flowers, Andrew. (2019, August 8). Cannabis Jobs in the U.S. Quadruple since 2016. Retrieved from External Linkhttps://www.hiringlab.org/2019/08/08/us-cannabis-jobs/; Barcott, Bruce. (2019, March 4). As of 2019, legal cannabis has created 211,000 full-time jobs in America. Retrieved from External Linkhttps://www.leafly.com/news/industry/legal-cannabis-jobs-report-2019

xx Colorado occupational licenses are valid for two years from issue date, therefore there is a lag in seeing occupational displacement due to declining business licenses.

xxi Support occupational licenses cannot be used for managerial employment whereas key occupational licenses do include managerial and supervisory positions.

xxii Starting Jan. 1, 2020, all key and support occupational licenses will be converted to a single category called an employee license. Owner licenses will remain separate. For more information, see External Linkhttps://www.colorado.gov/pacific/enforcement/med-occupational-license-industry-employees.

xxiii For more information, see Marijuana Policy Group, Light et al. The Economic Impact of Marijuana Legalization in Colorado. October 2016.

xxiv Direct employment in the marijuana industry includes employment directly in marijuana businesses, whereas indirect employment includes employment generated to support the marijuana industry, such as security services and legal services. In 2018, Leafly estimated that there were 4,723 indirect marijuana jobs in Colorado. For more information, see External Linkhttps://www.leafly.com/news/industry/legal-cannabis-jobs-report-2019

xxv Bureau of Labor Statistics, Current Employment Statistics (seasonally adjusted numbers).

xxvi For more information, see the Colorado Department of Revenue here: External Linkhttps://www.colorado.gov/pacific/tax/marijuana-taxes-file.

xxvii Ibid.

xxviii For more detail, see the Colorado Department of Education’s website here: http://www.cde.state.co.us/communications/2019marijuanarevenue

xxix Ibid.

xxx Of the 15 percent sales tax applied to recreational marijuana, 15.56 percent of the 90 percent tax collections held by the state government is retained in the general fund.

xxxi For more information, see External Linkhttps://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2019/08/forecasts-hazy-for-state-marijuana-revenue

xxxii For additional information on potential costs of marijuana, see our previous Rocky Mountain Economist on Colorado’s marijuana market here: https://www.kansascityfed.org/publications/research/rme/articles/2018/rme-1q-2018.

xxxiii There is a similar study done by the Colorado Department of Public Health and Environment, Behavioral Risk Factor Surveillance System that shows similar results. The data can be found here: External Linkhttps://www.colorado.gov/pacific/marijuanahealthinfo/brfss-data.

xxxiv It is important to note that although the average usage for 12 to 17 year olds has fallen, survey sampling issues cause these averages to have a fairly wide 95 percent confidence ban. A recent study using the same NSDUH data stated that marijuana use in 12 to 17 year olds in 2002 to 2005 fell from 10.5 percent to 9.0 percent in 2014 to 2017, however this change was not statistically significant. For more information, see: Substance Abuse and Mental Health Services Administration. Behavioral Health Barometer: Colorado, Volume 5: Indicators as measured through the 2017 National Survey on Drug Use and Health and the National Survey of Substance Abuse Treatment Services. HHS Publication No. SMA-19-Baro-17-CO. Rockville, MD: Substance Abuse and Mental Health Services Administration, 2019.

xxxv It is possible that a rise in usage following legalization was due to diminished fears over an individual self-reporting that they use an illegal drug, as survey users may have felt a higher reluctance to report usage prior to legalization.

xxxvi Colorado Department of Public Health and Environment, Behavioral Risk Factor Surveillance System: External Linkhttps://www.colorado.gov/pacific/marijuanahealthinfo/brfss-data.

xxxvii Colorado Division of Criminal Justice, Department of Public Safety. Offense/Arrest/Court Filing Data from the Colorado Bureau of Investigation, National Incident-Based Reporting System: External Linkhttps://www.colorado.gov/pacific/dcj-ors/Offense/Arrest/CourtFiling.

xxxviii Colorado Division of Criminal Justice, Department of Public Safety. Driving Under the Influence. Data from the Colorado State Patrol: External Linkhttps://www.colorado.gov/pacific/dcj-ors/driving-under-influence.

xxxix Rocky Mountain High Intensity Drug Trafficking Area. “The Legalization of Marijuana in Colorado: The Impact.” Volume 6, September 2019. Data specifically from: National Highway Traffic Safety Administration, Fatality Analysis Reporting System (FARS), 2006 – 2011 and Colorado Department of Transportation 2012-2018.

xl Ibid.

xli The Secure and Fair Enforcement Banking Act (SAFE Banking Act) was approved by the U.S. House of Representatives in September 2019, which aims to secure and broaden access to payment and banking systems for marijuana businesses. This legislation is currently pending U.S. Senate review. For more information, see: External Linkhttps://mjbizdaily.com/historic-day-us-house-passes-cannabis-banking-bill-with-strong-bipartisan-support/

xlii For more information, see: External Linkhttps://www.pewresearch.org/fact-tank/2019/11/14/americans-support-marijuana-legalization/

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author