The Great Recession led to substantial declines in asset values and investment returns, placing the funding levels of some state pensions in the spotlight. State pension funds rely on investment returns to fund future payments to retired employees, and the low returns during the Great Recession led many to question whether assumptions about investment returns for state pensions were set too high. Indeed, some studies suggest pensions are vastly underfunded.i,ii The solvency of state and local pensions is important for the regional economy due to the sizable share of employees that relies on pension income and the cost of pension funds to state and local governments. This issue of the Rocky Mountain Economist analyzes the importance of state pension funds and their current funding levels in the Rocky Mountain States.

Understanding State Pension Plans and Their Importance in the Rocky Mountain States

Pension plans differ from other retirement plans in that most pensions are defined benefit plans, in which the employer is primarily responsible for ensuring the plan has enough funding to pay its employees a defined amount during retirement. These plans are more common among government agencies. In contrast, most retirement plans offered by private sector employers are defined contribution plans, in which the employer, employee, or both pay into a fund that is invested and paid out to the employee upon retirement. The key difference is that in a defined benefit plan, the amount paid out is determined by various factors such as years of service and wage at retirement, whereas a defined contribution plan will pay out whatever has been contributed to the account plus any earned investment return. Most private institutions have switched over time to a defined contribution plan, but many government agencies still offer employees a defined benefit retirement pension.

State and local employees covered by a pension make up a large share of the total workforce and population in the Rocky Mountain States. The share of the total population that is current employees entitled to a pension in the future, former employees entitled to a pension upon retirement, or former employees currently receiving a pension is about 8 percent in Colorado and New Mexico and almost 12 percent in Wyoming. In other words, about one in 10 Rocky Mountain State residents depends on some form of state or local pension. In some cases, these individuals will receive a pension instead of Social Security payments, increasing their reliance on pension funds.

The funding of state and local pensions has become an important issue, as their ability to pay current and future retirees recently has been questioned. These funds rely heavily on investment returns, and the dismal market returns during the Great Recession led to deterioration in the funding levels of many pension funds. In addition to investment returns, state and local pension plans are jointly funded by both employees and the government agencies that employ them. As of 2015, the share of state and local governments’ total annual contributions to pensions in Colorado, New Mexico and Wyoming was 65.3 percent, 56.7 percent and 49.7 percent, respectively; employee contributions make up the remainder. Contributions by employers and employees and investment returns are the primary sources of pension funding.iii

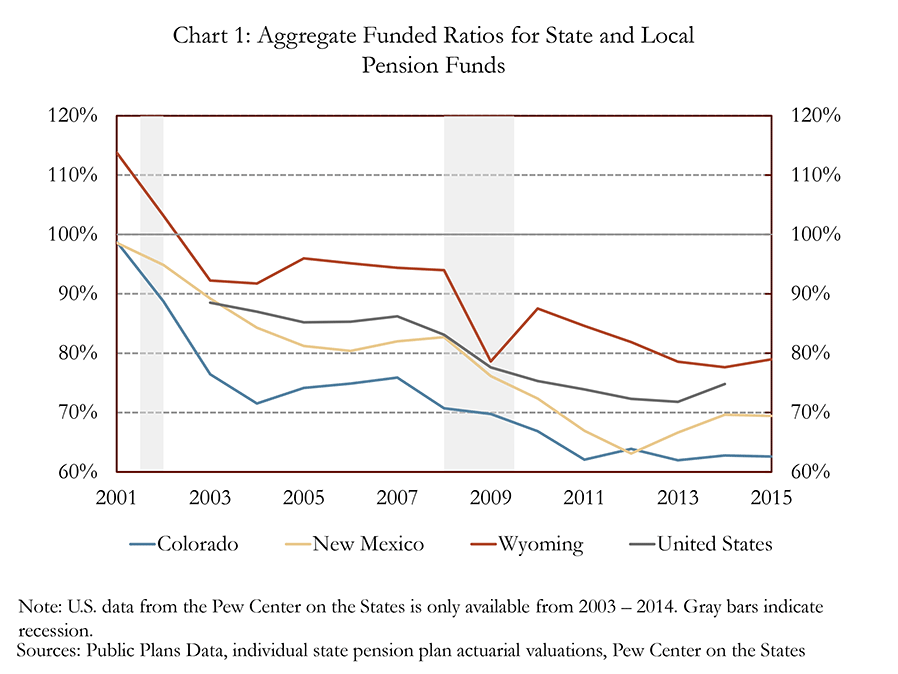

For governments to determine how much they should contribute annually to fully fund pensions, they first must approximate the assets they will need in the future to cover future payments, also known as liabilities. One common measure of the solvency of a pension fund is the “funded ratio,” which measures whether there will be enough assets to cover expected pension payments to retirees in the future. A funded ratio of 100 percent indicates there are enough assets (assuming actual investment returns equal expected returns and that other model assumptions hold) to cover expected future pension liabilities. A funded ratio below 100 percent indicates a shortfall is likely. Chart 1 shows the aggregate funded ratio from 2001 to 2015 for the major state and local pension funds in the Rocky Mountain States and United States.iv

The funded ratios for the Rocky Mountain States were close to—or above for Wyoming—100 percent in the early 2000s. The decline in the funded ratios during the early 2000s is primarily attributable to lower investment returns after the “tech bubble” burst, although Wyoming and Colorado reduced their contributions as well. After stabilizing in the mid-2000s, funded ratios in all states declined substantially during the Great Recession. In recent years, funded ratios seem to have stabilized again but at levels well below 2001.

A stark decrease in the funded ratio during the Great Recession is not surprising. During this period, investment returns fell sharply, leaving pension funds with fewer assets than they had anticipated. Additionally, state and local government revenues decreased as tax collections diminished. Subsidy programs, such as unemployment insurance, also increased, leaving less cash available to contribute to pensions to cover investment shortfalls. The next section will discuss how much governments would need to contribute to achieve a fully funded status and how much they actually contribute to pension funds.

The Funding of State and Local Government Pension Plans

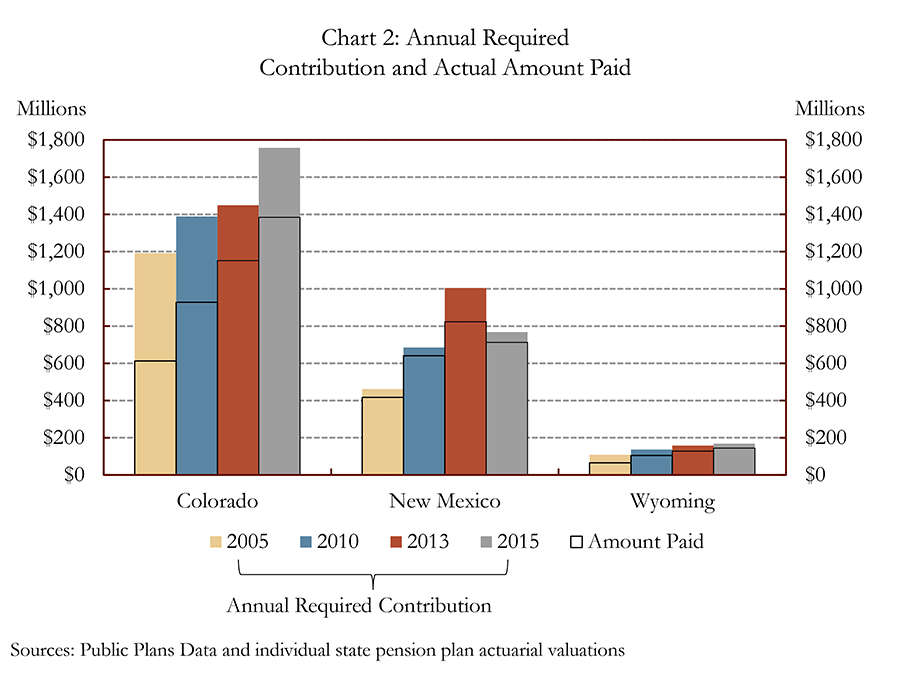

With funded ratios well below 100 percent in the United States and the Rocky Mountain States, a key consideration is what it would take to move pension plans closer to fully funded. One way to increase the funded ratio is for government employers and employees to pay enough annually to cover the normal contribution, or the present value of expected future benefits, as well as enough to make up the gap between the current and 100 percent funded ratios.v The amount contributed to the pension fund that must cover the normal contribution and the amortization of the unfunded liability is called the annual required contribution (ARC). If the entire ARC is paid annually, then the fund will move toward being fully funded. Chart 2 shows the ARC and the actual amount paid for 2005, 2010, 2013 and 2015. For the four years shown, the amount paid by each Rocky Mountain State was below the ARC. In 2015, Colorado, New Mexico and Wyoming paid 79 percent, 93 percent and 86 percent, respectively, of their ARC.

Funded ratios generally declined over the past decade, and, in turn, the contribution needed for the ARC increased in Colorado and Wyoming. New Mexico also experienced an upward trend in the ARC, but in 2015 this amount declined. Some underlying assumptions in New Mexico’s pension plans were altered in 2014, which slowed the growth of future liabilities. For example, the expected pace of payroll growth was lowered from 4 percent to 3.5 percent. The changes to these underlying assumptions, along with stronger-than-expected returns on assets in 2014, decreased the expected future payments to retirees, thereby increasing the funded ratio in Chart 1 and lowering the ARC in Chart 2.

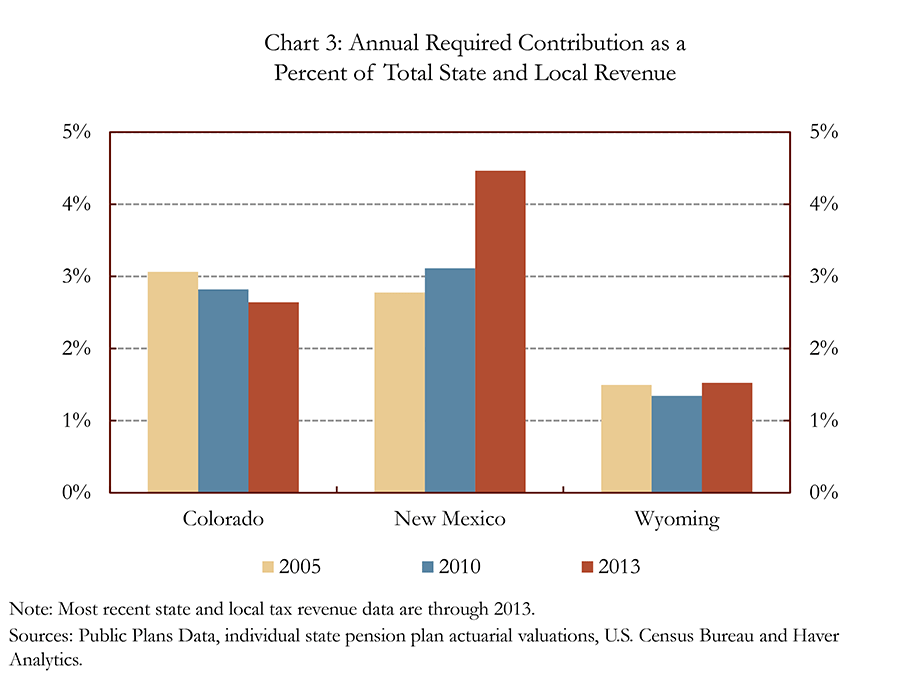

As funded ratios have declined and actual payments have increased, it is important to consider the implications for state and local budgets. One way to examine this trend is to look at how much incoming state and local government revenue is needed to move pension plans toward fully funded status. Chart 3 shows the ARC as a percent of total state and local government revenue in Colorado, New Mexico and Wyoming. It is common for both employees and employers to contribute to pension funds and employee contributions are included as part of the revenue for state and local governments. The share of revenue needed to fund pensions has held relatively stable in Colorado and Wyoming in recent years as total revenue has increased at about the same pace as the ARC. However, payments to pension funds could represent a potentially larger risk to the budgets of Rocky Mountain States if required pension contributions grow at a faster pace than total government revenue.

How do Underlying Assumptions Affect Pension Solvency?

The funded status of pensions and the ARC needed to move them toward fully funded status rely on many assumptions. Among factors that affect the amount paid to employees during retirement are salary earned prior to retirement, years of service and age at retirement. It is difficult to calculate expected benefit payments, or pension liabilities, over the life of an employee because it relies on underlying assumptions that are likely to change. These factors include mortality rates, wage growth, job tenure, cost of living adjustments and inflation. If assumptions about these factors underestimate payments, government must cover the extra costs out of pocket when the payment is due. In contrast, if liabilities are overestimated, then the funded status today would be higher than is currently estimated.

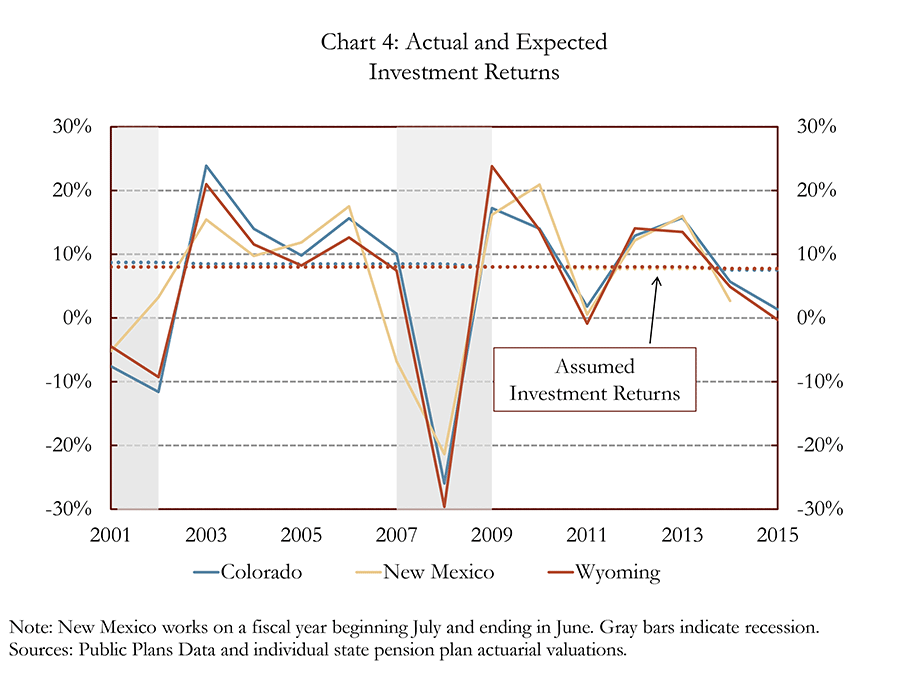

The funded status and ARC also depend crucially on each fund’s projected investment return on assets. Chart 4 shows actual and expected returns from 2001 to 2015 for pensions in the Rocky Mountain States. The path of actual returns was similar in Colorado, New Mexico and Wyoming, with each state experiencing similar losses and gains around the last two recessions. Pension funds have lowered their expected returns (dashed lines) since the early 2000s. In 2011 and 2014, New Mexico and Wyoming, respectively, each reduced expected returns from 8 percent to the current level of 7.75 percent. Colorado reduced its expected return three different times from 2001 to 2015 including a reduction from about 8.7 to 8.5 percent in 2003, from 8.5 to 8 percent in 2009 and from 8 to 7.5 percent in 2014. From 2005 to 2015, 59 of the 91 state and local pension plans across the United States that reported an investment return decreased their expected return.vii The average of actual returns from 2001 to 2015 was lower than states’ expected returns. The average actual return for Colorado, New Mexico and Wyoming was 6.5 percent, 5.8 percent and 5.8 percent, respectively during this time period.

The investment return assumption can vastly change the present value of future pension liabilities. A higher assumed return leads to higher funded ratios, while a lower return leads to a lower funded ratio. A study from the Center for State and Government Excellence indicates a 1 percent decrease in the discount rate (or investment return) would lead to an increase in liabilities of about 12.5 percent, and thus a 12.5 percent decrease in the funded ratio.viii Funded ratios for Colorado, New Mexico and Wyoming would be lower if actual returns in the coming years equal their average return since 2001 of 6.5 and 5.8 percent instead of their expected returns.

Conclusion

State and local government pension plans cover a large share of the Rocky Mountain States’ workforce and population, and the funded ratio of many of these plans has moved lower since 2001. The solvency of these funds is important not only to state and local pensioners but also taxpayers of the Rocky Mountain States. To calculate the money needed today to cover future pension payments, states must make many assumptions such as the investment return on their assets. If actual investment returns are lower than assumed returns, pension plans will not be funded at levels that are currently anticipated and will require additional contributions or changes to payments to avoid default. Over the past decade, Colorado, New Mexico and Wyoming have lowered their assumed investment returns. These lower assumed returns have moved assumed returns closer to historical averages of actual returns, but also have increased the annual contribution needed to move funds closer to being fully funded.

Endnotes

i Urahn, Susan K. et al. “The Trillion Dollar Gap: Underfunded State Retirement Systems and the Roads to Reform.” Rep. Washington, D.C.: Pew Charitable Trusts, 2010. Web.

ii Novy-Marx, Robert, and Joshua D. Rauh, “Public Pension Promises: How Big Are They and What Are They Worth?” Journal of Finance, Oct. 8, 2010.

iii State & Local Government Finance, United States Census Bureau.

iv Colorado pensions refer to the Colorado Municipal, Colorado School, Colorado State, Denver School and Denver Employee pension funds. New Mexico pension fund refers to the New Mexico PERA managed-funds and the New Mexico Educational fund. Wyoming pension fund refers to the Wyoming Public Employees’ pension fund.

v To make up lost ground between the current funded ratio and 100 percent, governments will make small payments above and beyond the normal cost to slowly increase the funded ratio to 100 percent. This is referred to as the amortization of the unfunded accrued liability. Typically governments amortize these payments over 30 years.

vi Since Colorado is referring to many different plans, the investment return is the asset-weighted average of each plan’s expected return.

vii External Linkwww.publicplansdata.org.

viii Munnell, Alicia, and Jean-Pierre Aubry. “The Funding of State and Local Pensions: 2015-2020,” Issue brief. Boston: Center for State and Local Government Excellence, 2016. Web.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Alison Felix

Senior Policy Advisor