The banking landscape has substantially evolved throughout the modern banking era, with everchanging structure including the size, complexity, and makeup of banking organizations. Even amidst industry shifts, community banks have remained vital providers of reliable access to credit and other financial services.

The Federal Reserve Bank of Kansas City is responsible for the supervision of the most community state-member banks of any Federal Reserve District. As such, Kansas City Reserve Bank staff leverage close relationships with community banks in supporting the Federal Reserve System’s key mission areas, including on the Federal Open Market Committee.

The following sections explore the unique characteristics and importance of community banks, as well as aggregated data on banking trends and financial performance.

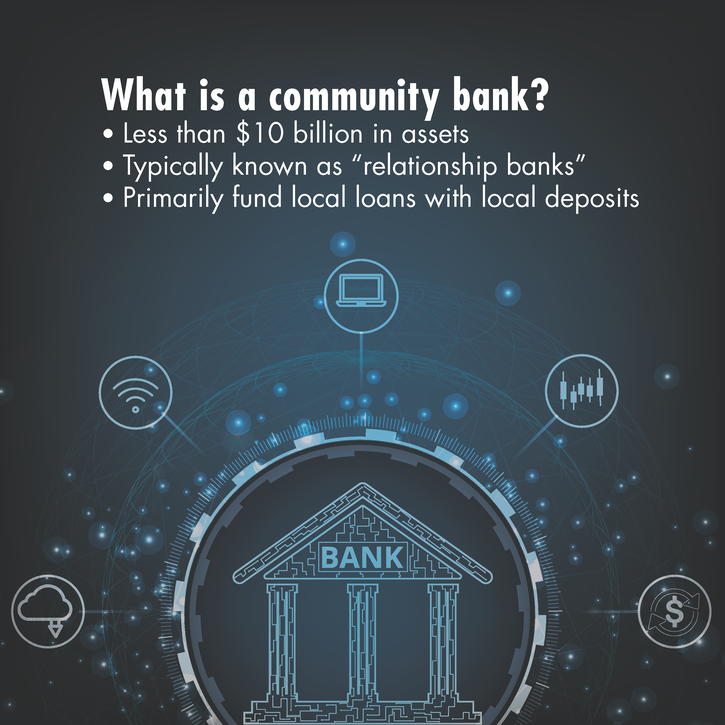

What is a community bank?

Banks are typically delineated by the volume of total assets on their balance sheets, with the following regulatory thresholds:

- Community banks: Less than $10 billion

- Regional banks: Between $10 billion and $100 billion

- Large banks: Over $100 billion

Community banks are often known as “relationship bankers.” Community banks serve businesses and consumers throughout the country, in both rural and urban areas, and are leading providers of credit to small businesses, often with strong relationships in their communities. At the core, community banks primarily rely on relationship lending, funding local loans with local deposits. Conversely, regional and large banks tend to have more reach, or a larger geographic footprint, than community banks. Benefits of scale typically allow these institutions to offer a broader array and greater complexity of products and services than community banks.

The balance sheets of community banks are generally more traditionally structured than those of larger banks given the nature of offerings and investments. Community banks rely more on net interest income and less on noninterest revenue sources.

Why are community banks important?

Community banks serve an important purpose in the community and broader economy. Given community banks’ focus on relationship banking, they can offer personalized service and maintain greater connection to their customers. Community bankers are able to develop relationships, understand the needs of customers, and maintain vast knowledge of their local market. Community banks are typically locally owned and managed and are staffed by individuals that live in the communities they serve. This contributes to the health of the local economy through employment and provides close connections and understanding of community needs. In serving local markets, community banks have a heavily vested interest in the success of their communities. Given a primary purpose of a community bank is to serve the credit needs of the community, these activities facilitate the growth and prosperity of local businesses.

Community banks have proven to be crucial to the availability of credit. In particular, community banks are outsized providers of credit to agricultural and commercial borrowers, including during periods of economic stress—as demonstrated by the relative stability of small banks’ business lending during the global financial crisis (GFC), and the significant role they played in intermediating emergency relief funds during the COVID-19 pandemic._ As the lender of choice for many small businesses, community banks ensure our local economies continue to thrive by meeting businesses’ essential financial needs. Community banks have also continually demonstrated an ability to understand the unique challenges households and businesses face in their communities.

How many community banks are there?

The total number of commercial banks nationwide has decreased significantly in the modern banking era, with more than 14,000 banks in the 1980s to only around 4,000 banks today. Much of the decline is reflected in fewer community banks with less than $100 million of assets. In addition, fewer new (de novo) banks are being formed.

As the financial system evolves and the industry continues to see consolidation, the market share of the largest banks continues to increase. Today, assets of the five largest commercial banks represent almost half of total banking assets, up from less than 15 percent in 1990. At the same time, the market share of community banks has declined, now at under 15 percent of total assets as of year-end 2023. In effect, the industry today is bifurcated between a small number of very large banks with significant nonbanking activities and thousands of community banks with more traditional banking practices.

Despite economic, demographic, and technological challenges, community bankers are committed to remaining relevant in the industry and broader economy. Community banks have proven resilient with a business model that emphasizes relationship development and strong community connections, a lasting foundation even amid changing consumer and business behavior. Still, many industry leaders have noted that community bankers must continue to adapt to the changing landscape with strategies to stay relevant and competitive, such as adopting new technologies and planning for succession.

Further Community Bank Resources:

As a supervisor of a large number of community banks, the Federal Reserve Bank of Kansas City is uniquely positioned to be a key provider of community bank analysis to the public, including such publications as the External LinkCommunity Banking Bulletin, which provides insights on trends or activities of primary interest to the community banking industry. As a complement to this work, the External LinkBank Summary Statistics dashboard is provided to promote better understanding of the population, trends in activity, and financial performance of community banks.

Research:

- External LinkCommunity Banks' Ongoing Role in the U.S. Economy, Federal Reserve Bank of Kansas City Economic Review (2021) │Economic Review, Second Quarter 2021

- External LinkFormer President Esther George Reflects on Her 40-Year Career at the Fed and the Importance of Community Banks │Community Banking Connections, Second Issue 2022

- External LinkFormer President Esther George: Why Community Banks Matter │April 6, 2017

- External LinkFormer President Thomas Hoenig: Are Community Banks Important? │March 18, 2010

- External LinkFormer President Thomas Hoenig: Oral Statement before the United States House of Representatives Subcommittee on Oversight and Investigations │August 23, 2010

- External LinkGovernor Bowman: Advancing Our Understanding of Community Banking │October 1, 2019

- External LinkGovernor Bowman: Defining a Bank │October 1, 2019

- External LinkPresident Jeff Schmid: Opening Remarks at A Workshop on the Future of Banking │April 2, 2024

- External LinkThe Case for the Community Banking Business Model: Lessons Learned from COVID-19 │Community Banking Connections, Second Issue 2022

- External LinkThe Role of Community Banks in the US Economy, Federal Reserve Bank of Kansas City Economic Review (2003) │Economic Review, Second Quarter 2003

References

Introductory remarks by Mr Jerome H Powell, Member of the Board of Governors of the Federal Reserve System, at the Community Banking Research and Policy Conference, co-sponsored by the Federal Reserve System and Conference of State Bank Supervisors, St. Louis, Missouri, 23 September 2014.

George, Esther. 2022. “President Esther George Reflects on Her 40-Year Career at the Fed and the Importance of Community Banks.” Federal Reserve System, Community Banking Connections, Second Issue. Available at https://www.communitybankingconnections.org/articles/2022/i2/esther-george-interview

Hoenig, Thomas M. “Oral Statement of Thomas M. Hoenig President Federal Reserve Bank of Kansas City.” Subcommittee on Oversight and Investigations United States House of Representatives. 23 Aug. 2010, Overland Park, KS.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.