Farm debt at commercial banks grew further in the fourth quarter, and delinquency rates remained historically low. Farm real estate and production loans were about 7% and 3% higher than the previous year, respectively. Agricultural banks expanded both farm and non-farm lending considerably in 2022 which, together with a slowdown in deposit growth, dropped bank liquidity down from recent highs. With higher loan demand and a steep rise in interest rates, profit and capital metrics at agricultural banks improved through the end of last year.

Demand for farm lending grew in 2022 alongside substantial increases in production costs, but the outlook for the agricultural economy in 2023 remained strong. Despite persistent concerns about operating expenses, higher interest rates and intense drought in some areas, commodity prices remained elevated and continued to support profit opportunities. Strength in farm income and liquidity likely contributed to lower delinquency rates on all farm loans, which were less than just 1%.

Fourth Quarter Commercial Bank Call Report Data

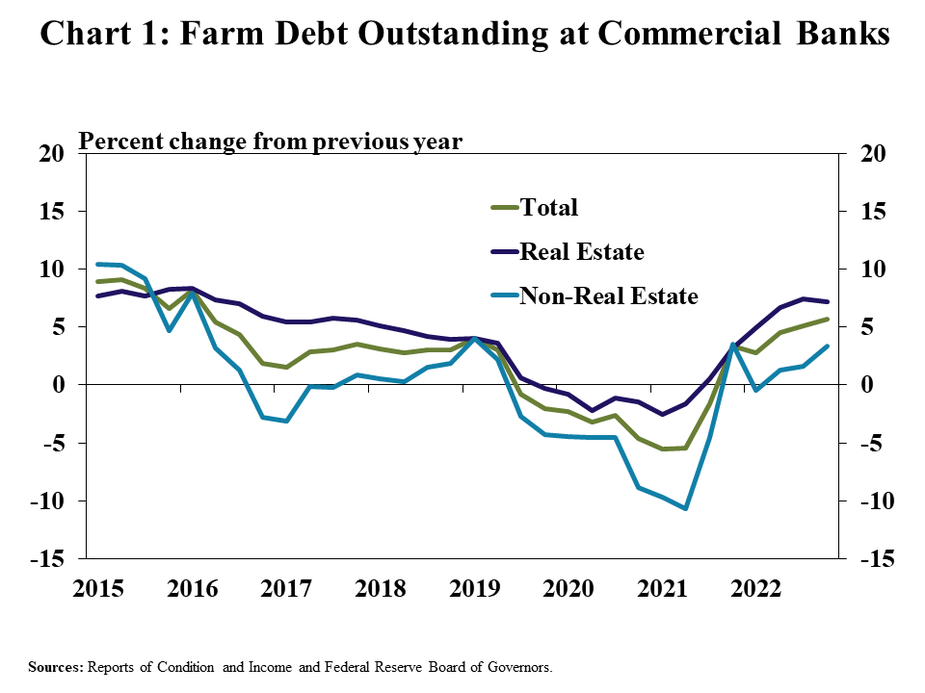

Steady growth in real estate and non-real estate farm lending pushed debt balances higher. Total farm debt increased about 6% between the fourth quarter of 2021 and the end of 2022, the fastest pace since early 2016 (Chart 1). Real estate and non-real estate loans increased at an average pace of nearly 6% and 2% during 2022, respectively.

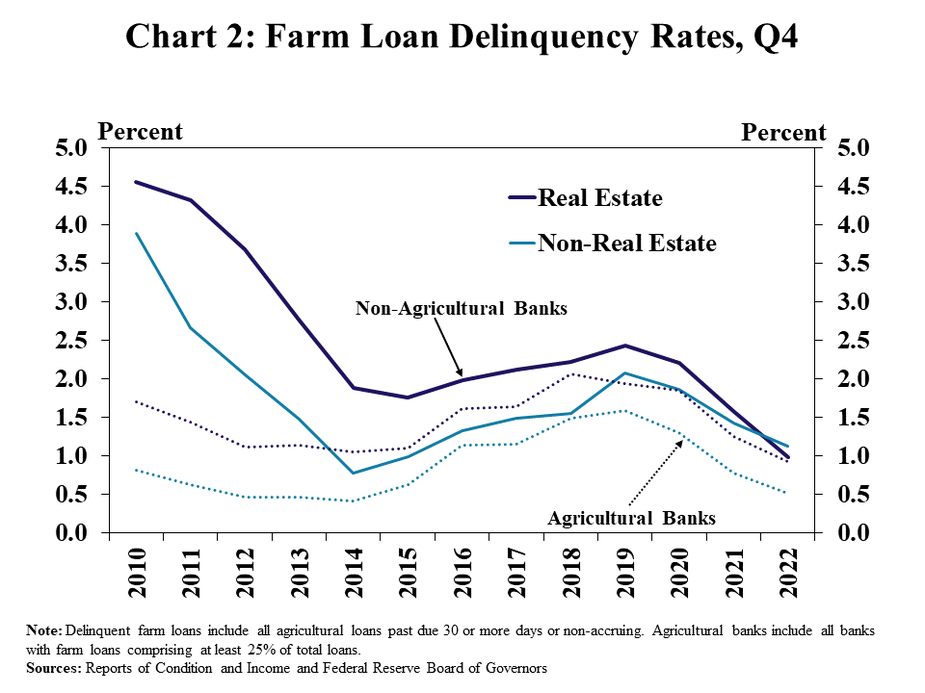

Loan performance continued to improve gradually alongside strength in farm finances despite increases in debt. Rates of delinquency on farm loans at both agricultural and non-agricultural banks during the fourth quarter edged lower for the third consecutive year (Chart 2). Strong farm income in recent years has bolstered liquidity for many producers and led to historically low rates of past dues on agricultural loans_

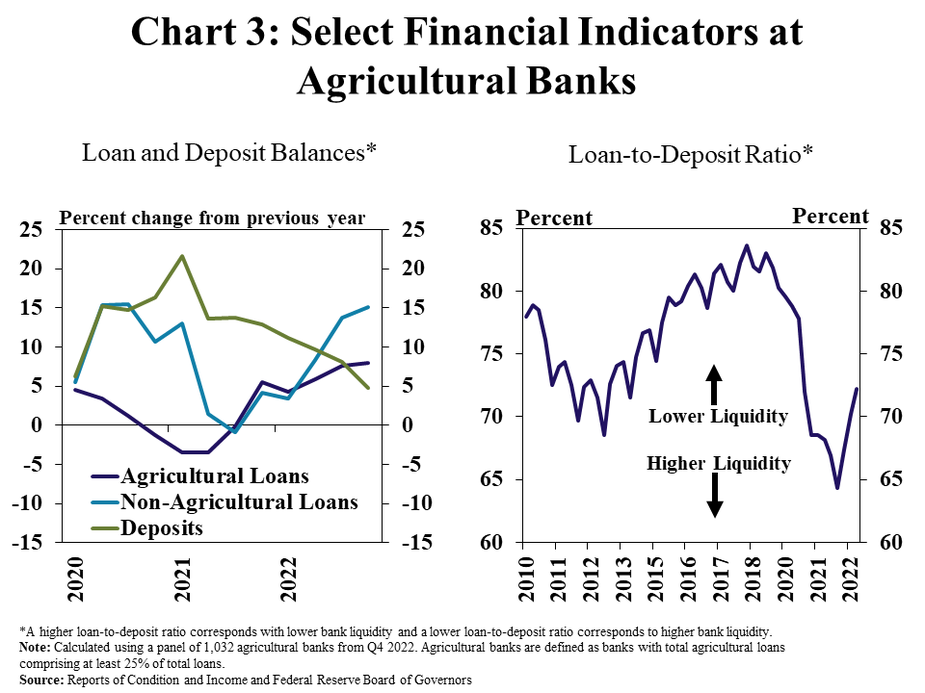

Notable increases in farm and non-farm lending led to a moderation in liquidity at agricultural banks. Loan balances grew considerably faster than deposit balances at banks most concentrated in agricultural lending at the end of 2022 (Chart 3). Demand for both agricultural and non-agricultural lending at farm banks grew throughout the year as deposit growth stabilized, and the loan-to-deposit ratio increased from multi-decade lows.

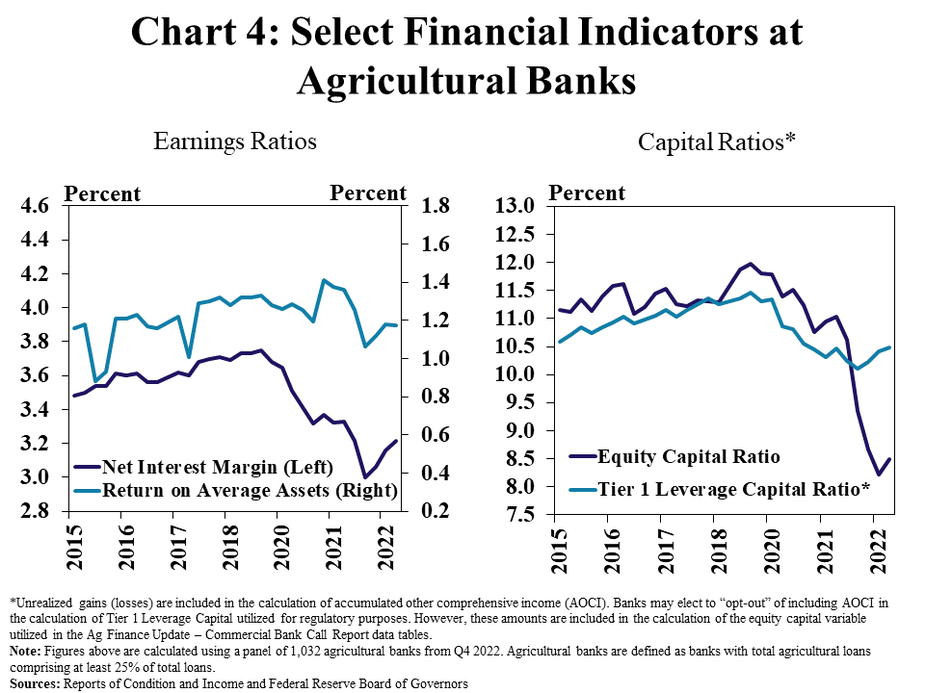

Growth in lending and higher interest rates contributed to improvement in financial performance at agricultural banks. Following steady contractions in recent years, profits at agricultural banks increased in 2022 alongside an increase in net interest margins (Chart 4). Higher earnings also supported a gradual rise in capital reserves throughout the year, despite some ongoing pressure from unrealized losses associated with securities holdings.

Endnotes

-

1 According to the External LinkUSDA Farm Sector Income Forecast, net farm income rose 8% in 2022 from the previous year after growing 43% in 2021. Similarly, working capital (a measure of farm liquidity) on U.S. farms rose by more than 40% in 2021 compared with the previous year and remained steady in 2022.

Data and Information

Commercial Bank Call Report Historical Data

Commercial Bank Call Report Data Tables

About the Commercial Bank Call Report Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Cortney Cowley

Assistant Vice President and Oklahoma City Branch Executive