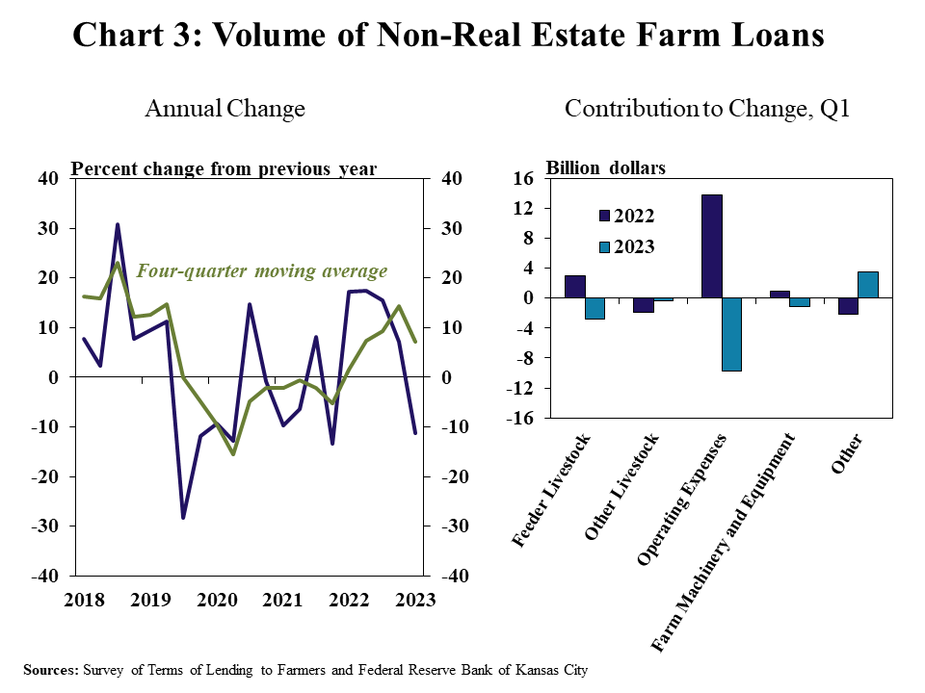

Growth in farm lending activity at commercial banks was limited in the first quarter of 2023 as interest rates climbed higher. Alongside additional increases in the federal funds rates, interest rates on farm loans rose sharply. The rapid rise has shifted the range of rates offered to borrowers upward considerably. Non-real estate farm loan volumes decreased about 10% from the previous year in the first quarter of 2023, following average growth of 15% in 2022. Lending activity was pushed down by fewer new loans and smaller-sized operating loans.

The outlook for farm finances remained favorable alongside elevated commodity prices, but higher interest rates, increased production costs and drought remained key ongoing concerns. Remarkably strong farm income during recent years has bolstered liquidity for many producers and supported historically strong farm loan performance. The availability of credit at agricultural banks remained ample and while higher expenses could increase borrowing needs for some operations, substantially higher interest costs could also put downward pressure on demand for credit.

First Quarter National Survey of Terms of Lending to Farmers

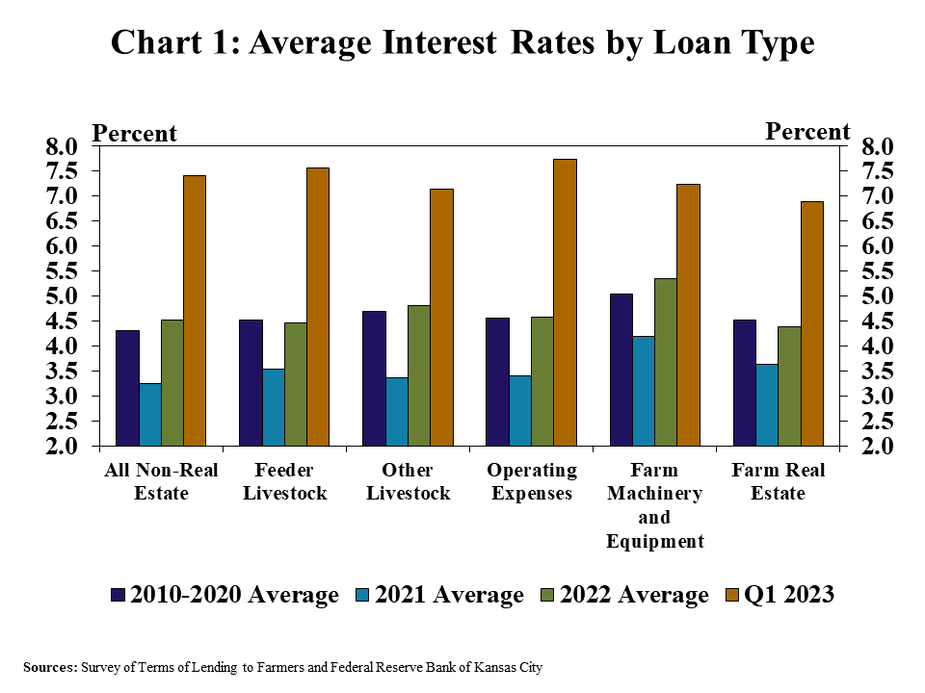

Interest rates on agricultural loans rose alongside further increases in benchmark rates. The average rate charged on all types of farm loans increased for the fifth consecutive quarter and reached the highest level since 2007 (Chart 1). Rates on both non-real estate and real estate loans have risen quickly and were nearly 4.5 and 3.5 percentage points higher than the end of 2021, respectively.

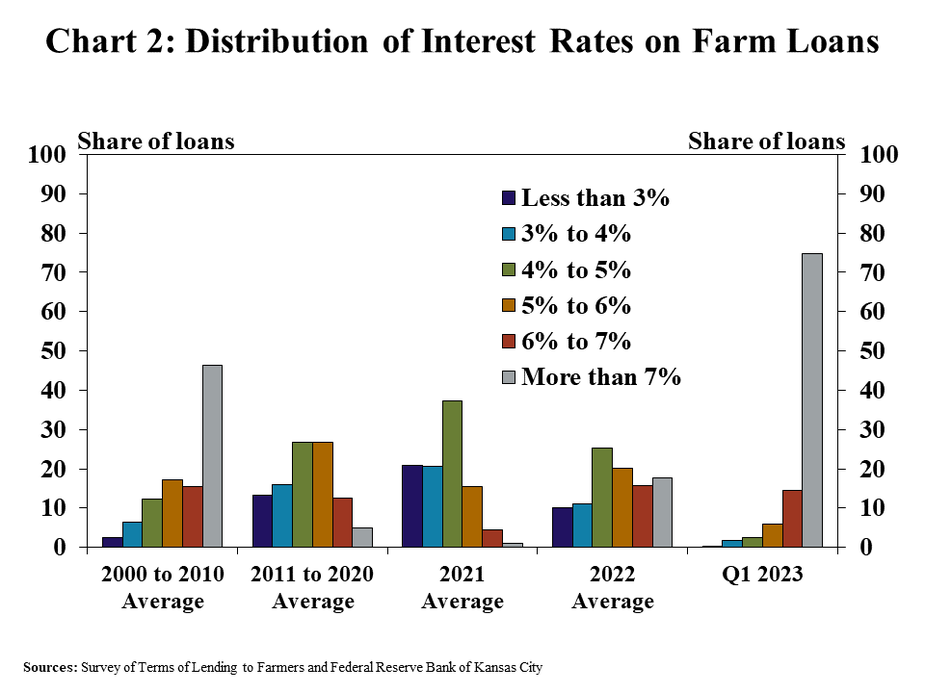

The range of interest rates available to borrowers has also shifted rapidly. In contrast to the average over the past two decades, three fourths of new loans in the first quarter had an interest rate above 7% (Chart 2). In comparison, more than half of farm loans had rates below 5% on average from 2011 through 2020.

As interest rates increased, non-real estate farm lending at commercial banks declined in the first quarter of 2023 according to the Survey of Terms of Lending to Farmers. The volume of non-real estate farm loans decreased about 10% in the first quarter and most of the decline was attributed to operating loans (Chart 3). While costs for farmers remained elevated, the price of some key inputs such as fertilizer and fuel were notably lower than a year ago and likely reduced credit needs for some producers.

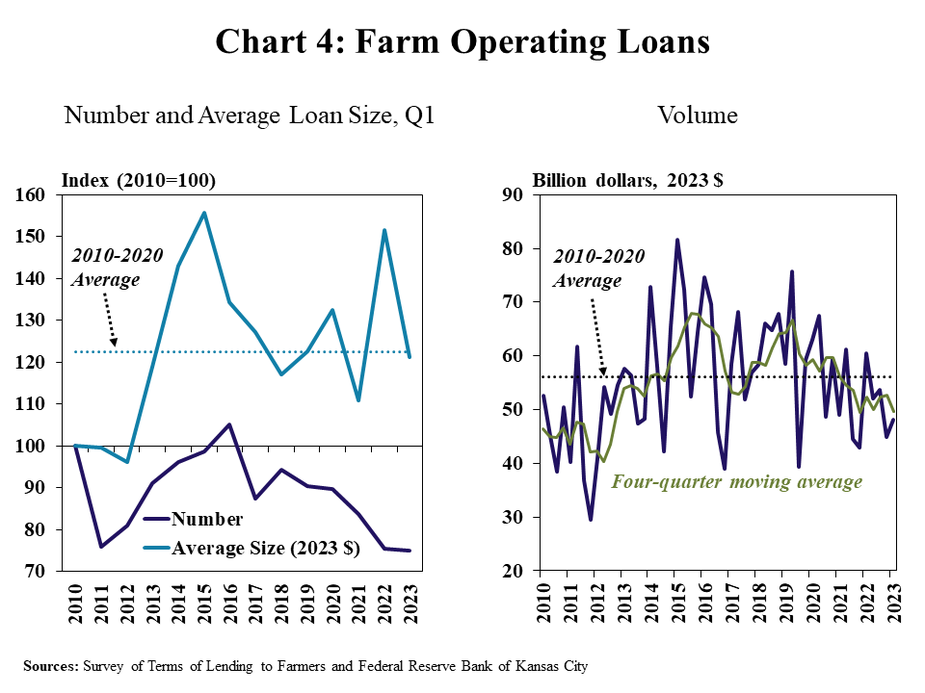

A fewer number of loans and a lower average size reduced lending for operating expenses. The average size of operating loans decreased from a year ago and was near the recent average while the number of loans remained at a historic low (Chart 4). The softening in lending activity kept total operating loan volumes about 15% below the average over the past decade.

Data and Information

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Tables

About the National Survey of Terms of Lending to Farmers

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy