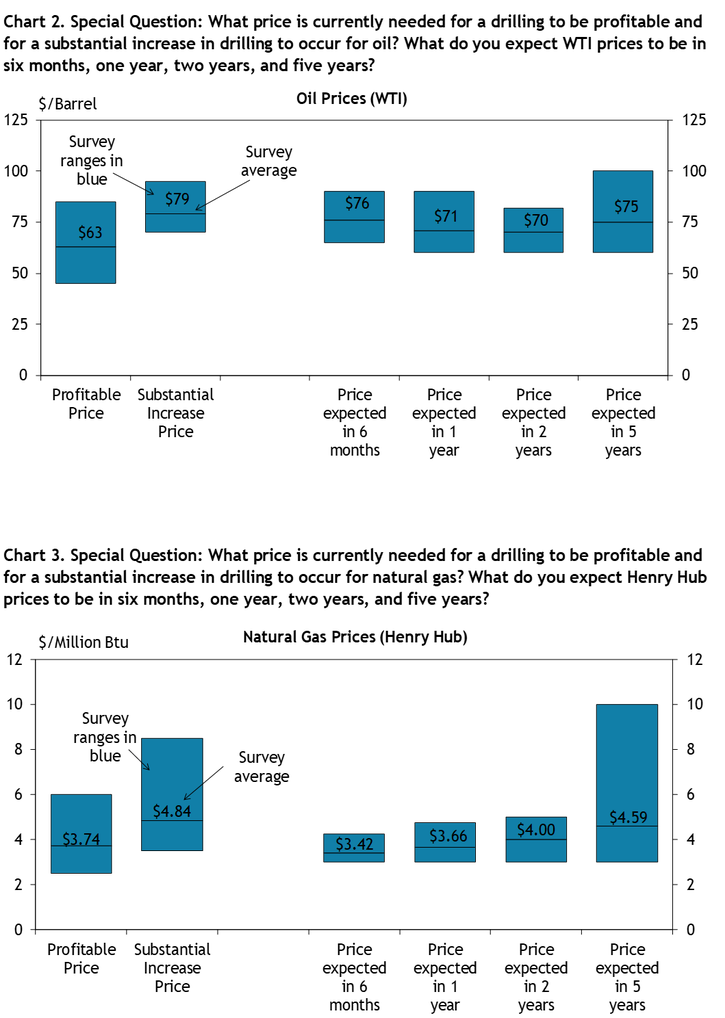

First quarter energy survey results showed that Tenth District energy activity was unchanged, but future expectations were substantially higher than last quarter. Firms reported that oil prices needed to be on average $63 per barrel for drilling to be profitable, and $79 per barrel for a substantial increase in drilling to occur. Natural gas prices needed to be $3.74 per million Btu for drilling to be profitable on average, and $4.84 per million Btu for drilling to increase substantially.

Summary of Quarterly Indicators

Tenth District energy activity was unchanged in the first quarter of 2026, as indicated by firms contacted between Mar. 16, 2026, and Mar. 31, 2026 (Tables 1 & 2). The quarter-over-quarter drilling and business activity index was 0 in Q1, up from -39 in Q4 and from -16 in Q3 (Chart 1). All quarter-over-quarter indexes were positive and up from last quarter, except for the access to credit index at -3. The revenues and profits indexes increased to their highest readings since Q2 2022, each at 31.

Drilling activity also was flat from this time last year, with the year-over-year drilling/business activity index rising from -50 to 0 in Q1. All year-over-year indexes increased and posted positive readings, except for capital expenditures which changed from -39 in Q4 to -9 in Q1. Employment levels and access to credit increased from last year, both posting readings of 13.

Six-month expectations increased substantially in Q1 amid higher oil prices, with the drilling activity, revenues, profits, and capital expenditures indexes all posting readings at or above 25. The expected drilling activity index grew from -19 to 25 and expected revenues from -22 to 35. Despite higher oil prices, the average firm only expects WTI oil to be $76/barrel in the next six months, below the $79/barrel price the average firm reports needing to support a substantial increase in drilling.

Chart 1. Drilling/Business Activity Indexes

Skip to data visualization table| Quarter | Vs. a Quarter Ago | Vs. a Year Ago |

|---|---|---|

| Q1 22 | 29 | 52 |

| Q2 22 | 57 | 77 |

| Q3 22 | 44 | 78 |

| Q4 22 | 6 | 56 |

| Q1 23 | -13 | 17 |

| Q2 23 | -19 | -16 |

| Q3 23 | -13 | -23 |

| Q4 23 | -33 | -33 |

| Q1 24 | -13 | -26 |

| Q2 24 | -14 | -25 |

| Q3 24 | -13 | -29 |

| Q4 24 | -13 | -16 |

| Q1 25 | 6 | -18 |

| Q2 25 | -17 | -17 |

| Q3 25 | -16 | -24 |

| Q4 25 | -39 | -50 |

| Q1 26 | 0 | 0 |

Summary of Special Questions

Firms were asked what oil and natural gas prices were needed on average for drilling to be profitable across the fields in which they are active. The average oil price needed was $63 per barrel (Chart 2), while the average natural gas price needed was $3.74 per million Btu (Chart 3). Firms were also asked what prices were needed for a substantial increase in drilling to occur across the fields in which they are active. The average oil price needed was $79 per barrel (Chart 2), and the average natural gas price needed was $4.84 per million Btu (Chart 3).

Firms reported what they expected oil and natural gas prices to be in six months, one year, two years, and five years. The average expected WTI prices were $76, $71, $70, and $75 per barrel, respectively. The average expected Henry Hub natural gas prices were $3.42, $3.66, $4.00, and $4.59 per million Btu, respectively.

Firms were asked how they expect recovery rates from U.S. shale wells to increase over the next 10 years (Chart 4). A quarter (25%) of firms expect oil recovery rates from U.S. shale wells to increase significantly over the next 10 years, while 50% expect them to increase slightly, another 16% expect no change, and only 9% expect rates to decline. Slightly fewer firms (13%) expect natural gas recovery rates to increase significantly, while 55% expect them to increase slightly, and 32% expect no change.

Contacts were also asked about their expectations for Venezuelan oil production over the next 24 months compared to expectations three months ago. Half of firms (50%) expect slightly more Venezuelan oil production, 22% expect significantly more, 12% report expectations have not changed, 7% expect slightly less production, and 9% reported no opinion.

Chart 4. Special Question: Do you expect upstream firms will be able to increase oil recovery rates from U.S. shale wells over the next 10 years? How about for natural gas?

Skip to data visualization table| Category | Oil | Natural Gas |

|---|---|---|

| Yes, significantly | 25 | 13 |

| Yes, slightly | 50 | 55 |

| No change | 16 | 32 |

| Recovery rates will decline | 9 | 0 |

| No opinion/don't know | 0 | 0 |

Chart 5. Special Question: How have your expectations changed for Venezuelan oil production over the next 24 months when compared with your expectations three months ago?

Skip to data visualization table| Category | Percent |

|---|---|

| Expect significantly more | 22 |

| Expect slightly more | 50 |

| Expectations unchanged | 12 |

| Expect slightly less | 7 |

| Expect significantly less | 0 |

| No opinion/don't know | 9 |

Selected Energy Comments

“Economic and political uncertainty will have us on the sidelines.”

“Prices will likely remain elevated as long as the Strait of Hormuz is closed. Prices may remain elevated for an extended period of time.”

“Don't anticipate any changes until prices stabilize.”

“High prices for too long will destroy oil demand and prices will go below economic replacement cost. Short term profits will be higher but in the longer term, we could see some disruption due to low prices.”

“At this point we are not altering our drilling plans. We have done some sensitivity analysis on our budget. If oil prices continue to move higher, we will most likely use this as an opportunity to accelerate our debt repayment.”

“Unstable energy prices do not appear to be causing increased drilling activity as it has in past wars. Oil companies are much more measured and capital disciplined and are not reacting too quickly.”

“Higher oil prices will increase free cash flow that can be reinvested into new wells.”

“Companies are delaying expenditures.”

“Increase in oil prices will drive drilling which will add additional supply to natural gas, driving the price down.”

“In the long term, prices will revert to the norm. Short term we will see a temporary spike in oil prices. At this point, we will not change our strategy.”

“Reduced activity in the near term. Potential for greater activity later this year and over the medium term.”

“Short term price spike, some higher drilling activity in 2026 and 2027.”

“We layered in additional hedges, but left room for more should the conflict get worse.”

“We are looking to hedge more at these high prices.”

“With oil prices backward dated, we have no plans to add to hedges.”

Additional Resources

Current Release

Download Historical Data

About the Energy Survey

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Cortney Cowley

Assistant Vice President and Oklahoma City Branch Executive