Stablecoins—a type of cryptocurrency intended to maintain a stable value relative to some other asset such as U.S. dollars or Treasuries—can serve several functions. For example, stablecoins can function as trading assets or tools that facilitate the trading of other crypto assets. Stablecoins can also serve as a payment method for person to business (P2B), business to business (B2B), cross-border, and other types of payments. While the stablecoin market is broadly discussed, the roles played by stablecoins and the shares of stablecoins used in different roles are unclear. As a result, it can be difficult to determine which stablecoin industry claims are justified and where growth is really occurring.

In this Payments System Research Briefing, I estimate the distribution of stablecoins by function and make three basic observations. First, payments are still a very small part of the stablecoin ecosystem. Second, a significant portion of stablecoins are held in bridging protocols that facilitate transfer of value between different blockchain networks; the need for this operation indicates that the stablecoin ecosystem still lacks interoperability. Third, a majority of stablecoins continue to be used in crypto finance rather than moving independently, suggesting that the stablecoin ecosystem is sensitive to the fortunes of this industry.

Functions of stablecoins in the stablecoin ecosystem

I estimate how stablecoins are distributed across functions in four broad categories: (1) trading assets, (2) payments, (3) transfers, and (4) idle.

Trading assets. The category of trading assets refers to stablecoins circulating within the crypto financial system for investment-related purposes. Here, stablecoins provide liquidity to exchanges and decentralized finance (DeFi) protocols, serve as collateral in lending and borrowing applications, act as a safe haven for capital between trades, and facilitate the transfer of value, among other purposes.

Trading assets can be further divided into three subcategories: exchanges, finance, and infrastructure. First, stablecoins can provide liquidity to exchanges, which lie at the heart of crypto finance and to an extent the entire stablecoin ecosystem. These exchanges include both centralized exchanges (CEXs), where an intermediary conducts trades and provides other services, and decentralized exchanges (DEXs), where trades and other services are provided through smart contracts with no intermediaries. Exchanges not only provide custody and trading facilities but also financial services and the ability to convert one stablecoin into another, allowing value movement across different blockchains. Exchanges therefore overlap with the finance and infrastructure segments of crypto finance (Batra and others 2026).

Second, stablecoins can provide liquidity to DeFi protocols, which provide financial services. A DeFi protocol is a financial service that provides peer-to-peer transactions without intermediaries. These platforms use smart contracts to automate services such as lending, borrowing, basis trading, and interest earning.

Third, stablecoins can move through infrastructure protocols to facilitate different uses. Almost all infrastructure protocols listed by DeFiLlama are bridges, which move stablecoins between different blockchains: Smart contracts lock stablecoins on one chain while minting like stablecoins on another. While all areas of the stablecoin ecosystem have infrastructure concerns, they appear to be particularly important to the area of finance, where a share of stablecoins must be used to move stablecoins across blockchains.

Payments. The payments category contains stablecoins on payment rails being used to make payments or purchases. The major use cases include peer-to-peer payments (fund transfers and cross-border remittances), consumer-to-business payments (including stablecoin credit and debit cards), business-to-business payments (especially cross-border supplier payments), and business-to-consumer payments (such as payroll).

Transfers. The transfers category captures stablecoins on blockchains being moved for non-payment purposes. These transfers tend to be high-value transactions primarily used for corporate treasury management, especially in cross-border transfers among corporate branches across countries, flows into and out of the crypto financial system, and settlement in tokenized assets and liabilities agreements.

Idle. The idle category refers to stablecoins sitting in rarely used wallets, forgotten, lost, or held as small savings. Stablecoins can be forgotten or lost when the wallets they are held in are no longer used or inaccessible due to the loss of keys, for example. Rarely used stablecoin wallets may also be a sign that the wallet and its contents are being used as a de facto fiat-denominated savings account.

Estimating stablecoin distribution across functions

Estimating the distribution of stablecoins across functions in the stablecoin ecosystem involves some guesswork. Available data on how exactly stablecoins are used and where they reside in the stablecoin ecosystem are spotty and often no more than estimates, making it difficult to provide a complete view of the stablecoin ecosystem. I use a combination of different types and sources of data to present general figures and percentages, many of which are for November 2025.

The strongest data are in the trading asset category. DeFiLlama’s Stablecoins Tracker, specifically its report, “Token Usage – USDT, USDC, USDE, USDS,” shows the total number of these stablecoins sitting in the 2,455 crypto finance-related protocols that DeFiLlama tracks (DeFiLlama 2025). USDT (Tether), USDC (Circle), USDE (Ethena), and USDS (Sky Dollar) are the top four stablecoins in circulation, making up over 90 percent of all stablecoins. Taken together, they serve as a good proxy for the entire stablecoin market. According to their data on November 14, 2025, the total stablecoin market cap was $300.5 billion, with $146.6 billion in stablecoins used in DeFi and other finance protocols. Thus, I estimate 48.8 percent of all stablecoins are used as a trading asset.

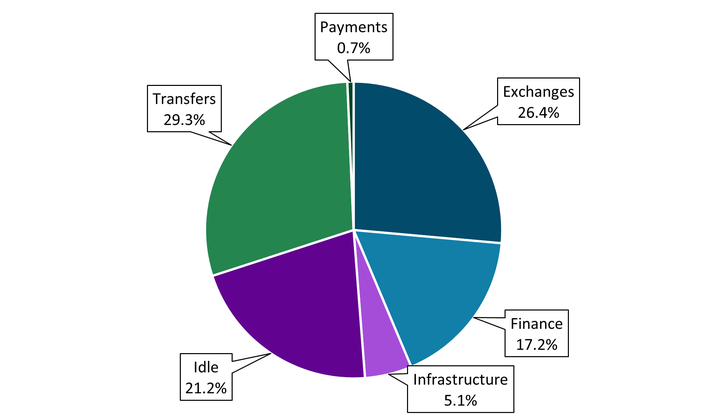

To break down the trading asset function into exchanges, finance, and infrastructure, I use the first 500 protocols in the same DeFiLlama report, as these protocols hold 99.9 percent of all tracked stablecoins used in the crypto finance area. These three subcategories’ shares of all stablecoins are shown in Chart 1: The dark blue area shows the share of exchanges, 26.4 percent; the light blue area shows the share of finance, 17.2 percent; and the light purple area shows the share of infrastructure, 5.1 percent._

Chart 1: Share of stablecoins by function

Sources: DeFiLlama (2025), Lurie (2024), Yim and others (2025), and author’s calculations.

Unlike trading assets, data on the other three categories—payments, transfers, and idle—are scarce; therefore, I make some assumptions to estimate the shares of these categories. A 2024 Forbes study estimated the shares of stablecoins as 40 percent trading assets, 30 percent idle, and 30 percent transfers and payments combined (Lurie 2024). Because Forbes’s estimated share of the trading asset category is fairly close to DeFiLlama’s data (40 percent versus 48.8 percent), I assume Forbes’s estimated shares of the other two categories are roughly accurate, with some modification.

Yim and others (2025) report an increase in the adoption of stablecoins for transfers and payments since 2024, suggesting that the proportion of stablecoins used for these functions may not have declined; however, the increased number of stablecoin transactions in transfers and payments does not necessarily imply an increase in the proportion of stablecoins used in these functions, either. Therefore, I assume that the combined share of transfers and payments remains the same 30 percent as Forbes’s estimate. To estimate the percentages of stablecoins used in transfers and in payments, I use the stablecoin payment transaction volume of $10.2 billion reported for August 2025 (the latest month available) in Yim and others (2025). I apply a velocity of money equation to calculate the number of stablecoins required for this payment transaction volume._ I obtain $2.0 billion, which is equivalent to 0.7 percent of all stablecoins (see the dark green area in Chart 1). Subtracting this figure from the percentage figure of 30 percent for transfers and payments combined results in a 29.3 percent share of transfers (light green area in Chart 1). While no data on the size of the transfers category exists, the large share of stablecoins used for transfers is plausible, as transfers consist mainly of high-value movements into and out of DeFi protocols and for internal treasury applications (Ved 2026; Ingham 2026).

Given the increase in stablecoin holders and active addresses for stablecoins, it is probable that the percentage of stablecoins that are idle—that is, held in inactive wallets—has decreased since 2024 (Godbole 2024; RWA.xyz 2025). To offset the increase in the share of trading assets from Forbes’s 40 percent estimate to the 48.8 percent obtained from DeFiLlama data, I assume that the share of idle stablecoins decreases from Forbes’s estimate of 30 percent to 21.2 percent (dark purple area in Chart 1).

Key insights from the estimated results

The estimates from the previous section offer three insights into the stablecoin ecosystem.

First, payments are still a very small part of the world of stablecoins, accounting for less than 1 percent of all stablecoin use. Here, payments defined in the traditional sense of B2B, P2P, and so on, have yet to live up to the promise of explosive growth proclaimed by many since the passage of the GENIUS act in July 2025. However, the use of stablecoins in payments is undoubtedly growing.

Second, more than 5 percent of stablecoins are tied up in the infrastructure of the stablecoin ecosystem, primarily bridges, indicating that interoperability problems exist. In fact, given the many infrastructure services provided by exchanges, the portion of stablecoins devoted to the machinery required to move tokens across chains and facilitate stablecoin usage may be understated.

Third, although stablecoins are widely believed to have the potential to operate independently of crypto finance, nearly half of all stablecoins continue to be used in crypto finance, including exchanges, finance, and infrastructure protocols, with CEXs and DEXs playing major roles. Overall, the large role played by crypto finance in the stablecoin ecosystem also suggests that the entire ecosystem is sensitive to the vagaries of crypto finance, rising and falling with the market.

Endnotes

-

1 The percentage of stablecoins sitting in exchanges is largely corroborated by CryptoQuant, which had the figure at 24.8 percent on November 14, 2025, a 1.6 percent difference from that calculated in this briefing (CryptoQuant 2025).

-

2 Yim and others (2025) put the stablecoin payments transaction volume at $10.2 billion. Meanwhile, Visa (2025) estimates the total monthly adjusted transaction volume for all stablecoin transactions to be $1.5 trillion. This adjusted number removes transactions that are not “organic” transactions like bots, double counting, and high-frequency trading. I first calculate the overall velocity for all stablecoins: Velocity = Transaction Volume / Money Supply = $1500 billion / $300.5 billion = 4.99. Then I use this velocity to calculate the money supply needed to sustain a payments transaction volume of $10.2 billion: Money Supply = Transaction Volume / Velocity = $10.2 billion / 4.99 = $2.0 billion.

Article Citation

Noll, Franklin. 2026. “What Are Stablecoins Used for Today? Estimating the Distribution of Stablecoins.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, April 10.

References

Batra, Inderpreet, Max Zevin, Ankit Mathur, Cláudio Quitete, Carlos Bravo, and Dawson Li. 2026. “External LinkStablecoin Payments: The Truth Behind the Numbers.” Boston Consulting Group, January.

CryptoQuant. 2025. External LinkAll Stablecoins(ERC20): Exchange Reserve - All Exchanges. Accessed November 14.

DeFiLlama. 2025. “External LinkStablecoins Tracker: Token Usage – USDT, USDC, USDE, USDS.” Accessed November 14.

Godbole, Omkar. 2024. “External LinkNumber of Stablecoin Holders Nears 100M Mark, Data Show.” CoinDesk, April 24.

Ingham, Lucy. 2026. “External LinkFXC Buyer’s Guide: Stablecoin Payments Infrastructure.” FXC Intelligence, February.

Lurie, Mark. 2024. “External LinkStablecoins: What Are They Used For?” Forbes, March 29.

RWA.xyz. 2025. “External LinkStablecoin Metrics: Active Addresses.” Accessed November 14.

Ved, Tanay. 2026. “External LinkThe Curious Case of USDC on Base.” Talos, February 18.

Visa. 2025. “External LinkStablecoin Transactions.” Visa Onchain Analytics Dashboard, accessed November 14.

Yim, Anthony, Andrew Van Aken, Nic Carter, Wyatt Khosrowshahi, Rob Hadick, and Omar Kanji. 2025. External LinkStablecoin Payments from the Ground Up. Part 2: Fall Update. October.

Franklin Noll is a lead payments specialist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author