The savings rate tends to rise in recessions, and the COVID-19 recession has proven no different. Even so, the magnitude of the recent rise in the savings rate has been stunning. Savings as a percentage of disposable personal income rose from 7.2 percent in December 2019 to a record high of 33.7 percent in April 2020. Although the savings rate has since retraced some of this rise, it remained at 13.6 percent as of October 2020—higher than its peak in any recent recession and nearly twice its pre-recession level. Have Americans increased their savings to guard against future income risks, or to fuel future spending once the pandemic recedes?

The savings rate can increase through one of two mechanisms: consumption falling relative to income or income rising relative to consumption. However, the dynamic linkages between savings, consumption, and income are more complicated than this arithmetic might suggest. Because one person’s spending is another person’s income, a rise in the savings rate due to falling consumption does not necessarily imply that accumulated savings will lead to future consumption growth. For example, an increase in the savings rate that coincides with a drop in aggregate consumption might lead to a drop in aggregate income, further dampening future spending. The coronavirus crisis may have well prompted this type of cautionary pullback in consumption as households became more reticent to spend. However, unprecedented government transfer payments in response to the pandemic have the potential to drive both savings and future consumption higher. As transfer income rose amid lockdowns and forbearance periods, the savings rate may have temporarily been pushed higher. If this transfer income is eventually spent, then the savings rate could normalize amid higher future consumption and, perhaps, higher future income should this stimulus increase growth. Therefore, understanding the motives behind the recent increase in the savings rate is clearly important for extracting a signal for future consumption.

To capture the dynamics between government transfers, the savings rate, and consumption, I estimate a statistical model that takes into account the lead-lag pattern that these three variables can display. Specifically, I estimate a vector autoregression (VAR) with five lags on monthly data from 1996 through 2019._ To disentangle the roles played by transfers and precautionary motives in shaping these variables, I assume that 1) transfer-induced saving simultaneously affects transfers, consumption, and the savings rate; and 2) that precautionary saving affects consumption and the savings rate despite no initial change in transfers.

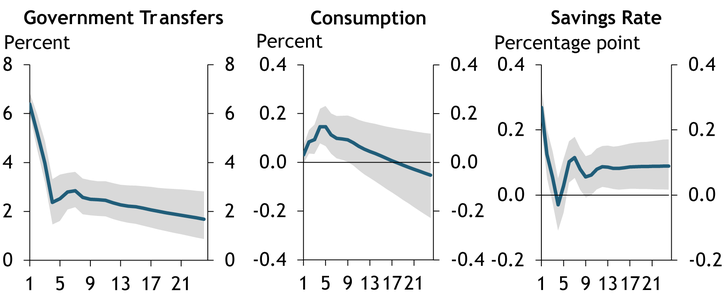

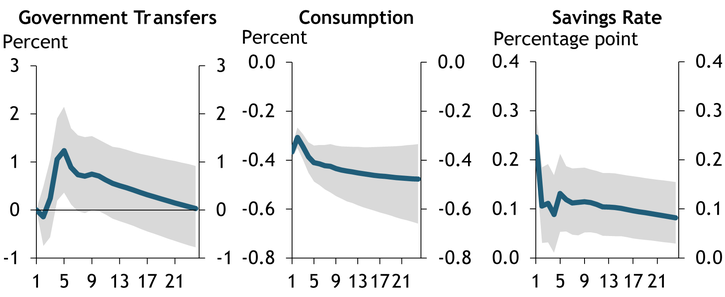

Charts 1 and 2 show the effects that these two motives to save have historically induced on consumption and the savings rate. Chart 1 shows that transfer-induced increases in the savings rate have historically led to increases in consumption, suggesting the potential for a positive correlation between the current savings rate and future spending. In contrast, Chart 2 shows that increases in the savings rate driven by precautionary motives have historically led to persistent declines in consumption. In fact, since consumption remains depressed for several years, the savings rate appears to normalize, in part, through lower future income rather than an unwinding of past savings after a precautionary increase in the savings rate. Therefore, precautionary savings can drive a negative correlation between the current savings rate and future spending.

Chart 1: Dynamic Responses to a Transfer-Induced Increase in the Savings Rate

Notes: The horizontal axis measures months since the savings rate increase. Blue lines represent the median estimated response. Gray shaded regions are 90 percent error bands.

Sources: Bureau of Economic Analysis (Haver Analytics) and author’s calculations.

Chart 2: Dynamic Responses to a Precautionary Increase in the Savings Rate

Notes: The horizontal axis measures months since the savings rate increase. Blue lines represent the median estimated response. Gray shaded regions are 90 percent error bands.

Sources: Bureau of Economic Analysis (Haver Analytics) and author’s calculations.

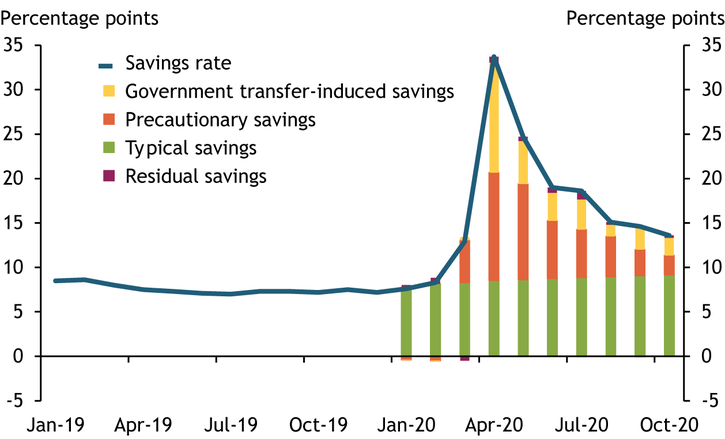

I next extend the estimation of the VAR through October 2020 to better understand how the recent increase in the savings rate might influence future consumption._ Chart 3 decomposes the recent increase in the savings rate into transfer-induced savings, precautionary savings, typical savings in the absence of these forces, and a residual._ The yellow and orange bars show that transfer-induced and precautionary savings have both contributed to the increase in the savings rate during this pandemic. However, the majority of the recent increase in the savings rate has been driven by precautionary motives. This decomposition therefore suggests that much of the recently accumulated savings is unlikely to be spent down in the near future. At best, the opposing implications for future spending from transfer-induced and precautionary motives suggest that the outlook for consumption implied by the elevated savings rate is rather murky.

Chart 3: Decomposing the Recent Increase in the Savings Rate

Sources: Bureau of Economic Analysis (Haver Analytics) and author’s calculations.

The savings rate has historically failed to predict future consumption, reinforcing the weak signal that savings provides for future spending. A standard approach to measuring the marginal predictive content of a given series is to perform a Granger causality test, which, in this application, provides an answer to the question: “given information on past consumption spending, do past values of the savings rate offer any additional information that would help to predict future consumption?” The above data used to study the dynamics between the savings rate and consumption suggest that the answer to this question is “yes.” However, this simple question overlooks the role that other factors play in shaping the future path of consumption. To capture these factors, the question can be reworded as: “given information on past consumption spending and past values of government transfers, do past values of the savings rate offer any additional information that would help to predict future consumption?” In this case, the answer then becomes “no.” Therefore, based on the marginal predictive content of various indicators, I again find little reason to expect the recent rise in the savings rate might boost future consumption spending._

As fiscal support lapses and forbearances expire, the strength of U.S. consumption is likely to be tested in the coming months. Recent increases in the personal savings rate have stirred hope that consumption will remain resilient. However, I find that such optimism may be misplaced, as past increases in the savings rate have failed to predict future consumption behavior.

An important caveat to this conclusion is that the unprecedented nature of this crisis could lead to departures from historical patterns. The sheer size and scope of recent government transfers, for example, could support spending once the pandemic recedes. However, the scarring nature of the crisis and previously unimaginable income risk could just as easily have given consumers a lasting desire to increase their liquidity buffers and guard against future income losses. After the Great Recession, for instance, Gallup surveys show a persistent increase in the share of consumers who prefer to save rather than spend (Saad 2019).

The uneven imprint of this crisis across the economy, which my aggregate analysis overlooks, could also lead to a departure from historical savings and consumption patterns. While many consumers may now have the desire to save more, only those that remain employed have the ability to actually save more. This distinction between desired and actual savings is important, as a pullback in consumption by employed households could amplify income losses for unemployed households in hard-hit sectors. This sectoral dynamic leaves little reason to be optimistic about future spending based on the elevated savings rate. In particular, if employed households are forgoing vacations and travel, forgone consumption today is unlikely to be made up in the future, creating a lasting income loss for many households.

Download Materials

Endnotes

-

1 I begin the sample in 1996 due to changes in government welfare policies around that time. Government transfers are measured by the sum of unemployment transfers and stimulus payments, and consumption is measured by personal outlays. Transfers and consumption enter the VAR in log levels. The number of lags included was based on the Akaike Information Criterion.

-

2 Extending the sample through October 2020 is necessary to complete a decomposition of the recent savings rate from the VAR residuals. However, extending the estimation sample of the VAR affects the estimated impulse response dynamics for transfer-induced savings shown in Charts 1 and 2. In particular, transfer-induced increases in the savings rate are now associated with an immediate fall in consumption, likely reflecting the fact that recent transfers occurred amid lockdown conditions that forced reductions in many services households typically consume. However, this is likely an aberration of the current period, and thus I assume that transfer-induced savings will eventually be spent. Otherwise, the decomposition in Chart 3 takes an even more pessimistic interpretation as both forces driving the savings rate higher would then portend lower future consumption.

-

3 The residual captures movements in the savings rate due to neither transfer- nor precautionary-induced savings.

-

4 Moreover, the savings rate offers no marginal predictive content for government transfers, which suggests that, even indirectly, the savings rate provides little signal for future consumption spending.

Reference

Saad, Lydia. 2019. “Expanded Minority in U.S. Say They Are Spending More.” Gallup News, May 2.

A. Lee Smith is a research and policy advisor at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author