Since December 2020, the Federal Open Market Committee (FOMC) has provided guidance that it would continue to increase the size of its balance sheet “until substantial further progress has been made toward the Committee’s maximum employment and price stability goals” (Board of Governors 2020). In September 2021, the Committee indicated that some of these conditions have been met and that “a moderation in the pace of asset purchases may soon be warranted” (Board of Governors 2021). As economic conditions in the United States continue to improve, the Committee is likely to pursue discussions on how to return monetary policy to a stance consistent with normal economic conditions—including, perhaps, whether to adjust its policy tools in the same order as the previous policy normalization.

During the previous policy normalization following the Great Recession, the FOMC first slowed the pace of large-scale asset purchases (LSAPs) in 2013, then raised the federal funds rate above the effective lower bound in 2015, and finally started reducing the balance sheet in 2017. However, alternative orderings were possible, then and now.

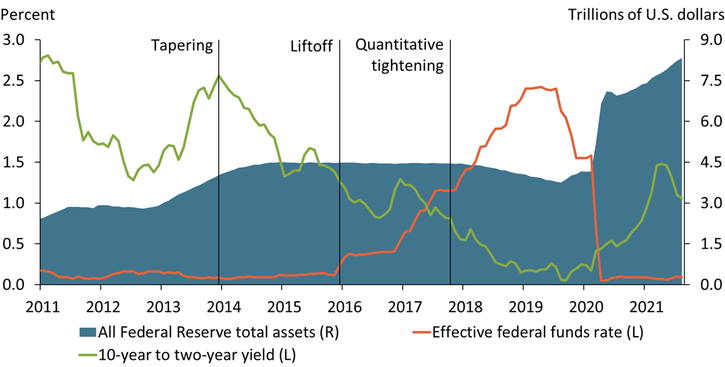

As a policy tool, the expansion of the Federal Reserve’s balance sheet through LSAPs is thought to primarily operate by depressing longer-term interest rates. Therefore, one potential consequence of raising the interest rate before reducing the size of the balance sheet is a flattening or inversion of the yield curve, in which long-term nominal interest rates fall to levels near or below that of short-term nominal interest rates. During the 2015–19 period of normalization, the yield curve flattened and occasionally inverted, likely attributable in part to the conduct of monetary policy, including the sequence of normalization. Chart 1 shows that the slope of the yield curve (green line) declined through much of the normalization period, increasing only in bursts. Notably, the slope of the yield curve continued its downward march unabated from 2017 through early 2020, when normalization was in full swing and the FOMC was steadily raising the effective federal funds rate (orange line). Because movements in the federal funds rate do not fully pass through to longer-term interest rates, raising the federal funds rate mechanically flattens the yield curve, holding other things constant.

Chart 1: In 2015–19, Raising the Policy Rate before Reducing the Balance Sheet Flattened the Yield Curve

Note: Green line shows the spread between the 10-year and two-year nominal interest rates, a proxy for the slope of the yield curve.

Source: Board of Governors of the Federal Reserve System (Haver Analytics).

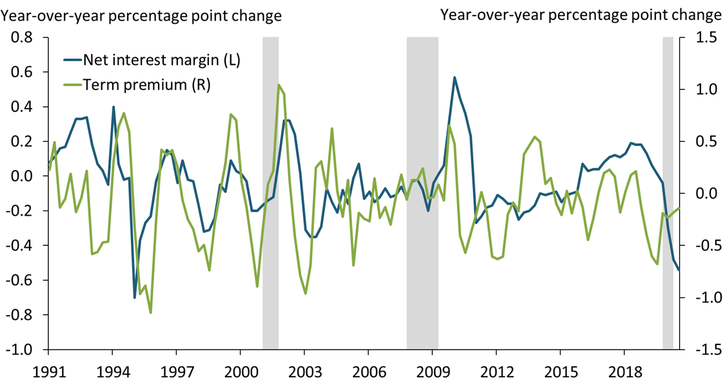

A flat or inverted yield curve may signal pessimism about the economic outlook. More importantly, however, it can also materially affect firms that profit from the spread between short- and long-term interest rates, such as banks and investment funds. Banks, for example, pay a short-term interest rate on deposits and receive a long-term interest rate from the loans they make. When the yield curve is inverted and long-term interest rates fall below short-term interest rates, this strategy becomes unprofitable. Chart 2 shows that a fall in term premiums (green line), which compensate banks for taking on interest rate risk, is historically associated with a decrease in banks’ net interest margins (blue line), contributing negatively to bank profitability and net worth._ A fall in expected future short-term interest rates has the opposite effect of raising net interest margins.

Chart 2: Falling Term Premiums Decrease Bank Net Interest Margins

Notes: Gray bars denote National Bureau of Economic Research (NBER)-defined recessions. We use the term premium on a five-year zero coupon bond.

Sources: Federal Reserve Bank of St. Louis (FRED), NBER, Bloomberg, Paul (2021), and Kim and Wright (2005).

Reductions in bank profitability due to yield curve inversion can bring about conditions that make future recessions more likely. Banks that fund long-term assets with short-term liabilities—often smaller banks and community banks—may respond to a flattening or inversion of the yield curve by tightening lending standards and reducing new lending. Smaller firms and individuals may, in turn, find it more difficult to access bank financing, causing them to scale back investment or consumption spending. In the longer run, a drop in core bank profitability increases the relative value of noninterest income, disproportionately the domain of larger banks. With smaller firms facing tighter credit markets, larger firms with access to bond and equity markets benefit, thereby encouraging consolidation and reducing competition.

An inverted yield curve can also engender economic fragility by encouraging banks to take greater risks for a few reasons. First, a reduction in bank profitability weakens banks’ incentives to screen and monitor new loans, which increases risk-taking. Second, a reduction in bank profitability may threaten banks’ commitments on target returns and managers’ compensation schemes, leading banks to take more risks to meet these commitments. Financial intermediaries such as money market funds or life insurance and pension funds may exhibit similar risk-taking. Thus, a flat yield curve has the potential to reduce risk premiums demanded by investors broadly across asset classes, posing risks to financial stability.

Would starting to normalize the balance sheet before the federal funds rate help to steepen the yield curve relative to patterns observed in 2015–19? The balance of evidence suggests that policies that reduce the balance sheet—also known as quantitative tightening (QT)—should lead to less flattening. Evidence from Smith and Valcarcel (2021), for example, suggests that QT raises term premiums more than short-term interest rates, steepening the yield curve on net. Moreover, D’Amico and Seida (2020) find that balance sheet policies move targeted maturities similarly across time within quantitative easing (QE) and across QE/QT. In the absence of short-term interest rate hikes, these results imply that QT would have steepened the yield curve relative to what we observed during the previous normalization.

Two factors could work to prevent a reduction of the balance sheet from increasing long-term yields and steepening the yield curve. First, other large, advanced economies look set to continue adding monetary stimulus even as conditions in the United States support normalization, as was the case in 2015–19. Thus, slow foreign growth is likely to continue to depress long-term yields going forward, which provides another incentive to increase term premiums before hiking short-term interest rates. Second, the shape of the yield curve will also be determined in part by Treasury issuance. Borrowing needs may fall as COVID-19-related government relief spending subsides and lawmakers work to raise revenue (instead of issuing debt) for multi-year spending plans for infrastructure and social programs—and bond issuance may fall accordingly. This decreased issuance would also weigh down long-term yields.

Overall, evidence from the normalization of monetary policy after the Great Recession highlights that the order in which policymakers normalize monetary policy matters. The sequence of normalization from 2015 through 2019 appears to have contributed to flattening in the yield curve, which can generate financial conditions that make future downturns more likely. Reducing the balance sheet before raising interest rates might forestall yield curve inversion in future normalizations.

Endnotes

-

1 Interest rate risk describes the potential for loss of investment resulting from a change in interest rates. Because the bank business model relies on the structure of the yield curve, banks are continually exposed to changes in interest rates. The term premium is the amount by which the long-term yield exceeds the short-term yield, or in basis points, the compensation for long term exposure to interest rates versus continuous short-term exposure.

References

Board of Governors of the Federal Reserve System. 2021. “External LinkFederal Reserve Issues FOMC Statement.” Press release, September 22.

———. 2020. “External LinkFederal Reserve Issues FOMC Statement.” Press release, December 16.

D’Amico, Stefania, and Tim Seida. 2020. “External LinkUnexpected Supply Effects of Quantitative Easing and Tightening.” Federal Reserve Bank of Chicago, working paper no. 2020-17, July.

Kim, Don, and Jonathan Wright. 2005. “External LinkAn Arbitrage-Free Three-Factor Term Structure Model and the Recent Behavior of Long-Term Yields and Distant-Horizon Forward Rates.” Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series Paper No. 2005-33, August.

Paul, Pascal. 2021. “External LinkBanks, Maturity Transformation, and Monetary Policy.” Federal Reserve Bank of San Francisco, working paper no. 2020-07, September.

Smith, A. Lee, and Victor J. Valcarcel. 2021. “External LinkThe Financial Market Effects of Unwinding the Federal Reserve’s Balance Sheet.” Federal Reserve Bank of Kansas City, working paper no. 20-23, April.

Karlye Dilts Stedman is an economist and Chaitri Gulati is a research associate at the Federal Reserve Bank of Kansas City. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author