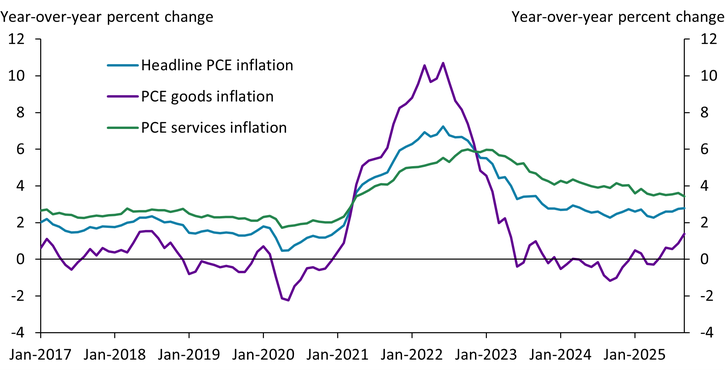

Inflation started to rise in early 2021 and was slow to decline after its peak in 2022. During the COVID-19 pandemic, supply chain disruptions and increased demand for goods put upward pressure on prices. This pandemic-related shock on goods-sector inflation proved temporary: Chart 1 shows that after peaking in mid-2022, goods inflation (purple line) rapidly declined. However, aggregate inflation, which includes both the goods-producing sector and the services-producing sector, has declined more slowly and remains above the Federal Reserve’s 2 percent target (blue line).

Chart 1: Aggregate inflation has persisted since 2022

Sources: U.S. Bureau of Economic Analysis (Haver Analytics) and authors’ calculations.

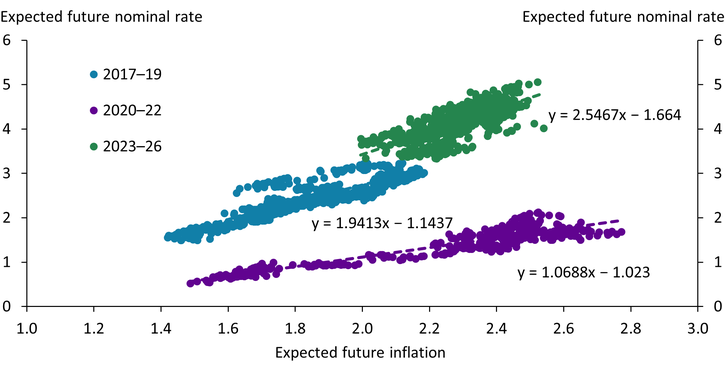

While inflation may persist if the economy experiences a persistent shock, it may also persist if monetary policymakers ignore—or delay responding to—an inflation shock judged to be temporary._ Financial markets do not necessarily distinguish between a tepid response to a temporary shock and a tepid response to inflation overall when they adjust their inflation expectations. Indeed, Bocola and others (2024) show that during the post-COVID inflationary period, financial markets perceived that the Federal Reserve’s response to inflation had weakened. To gauge how market perceptions of the Federal Reserve’s policy responses have changed over time, they construct an “inflation feedback parameter.”

This parameter captures financial markets’ estimates of how much policymakers should change the interest rate in response to a 1 percentage point deviation from the central bank’s inflation target. Chart 2 plots the daily market-based measure of expected future inflation on the horizontal axis and the market-based measure of the expected future nominal interest rate on the vertical axis, with the slope illustrating the inflation feedback parameter. When expected future inflation increased by 1 percentage point during the 2017–19 timeframe (blue dots), markets expected nominal interest rates to move up by 1.9 percentage point; however, in 2020–22 (purple dots), the same increase in expected future inflation led markets to expect only a 1.1 percentage point increase in nominal rates. In other words, the inflation feedback parameter shifted down from 2017–19 to 2020–22 and the slope became flatter as financial markets came to expect a weaker response to inflation. In 2023–26 (green dots), the parameter became steeper after the Federal Reserve hiked the federal funds rate and kept monetary policy tight, leading financial markets to perceive a stronger response to inflation.

Chart 2: Financial markets’ perceptions of the policy response to expected inflation shifted down and flattened in 2020–22

Sources: Bocola and others (2024) and authors’ calculations.

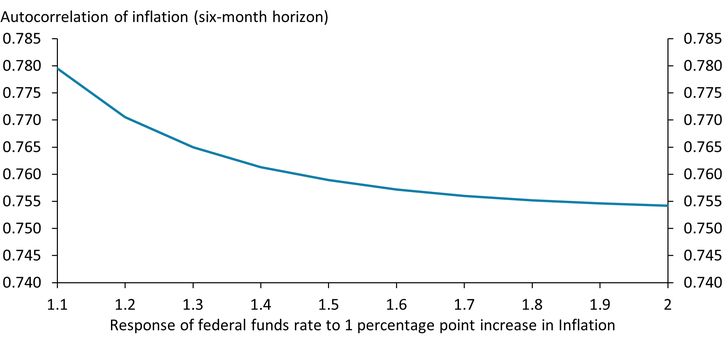

Shifts in the inflation feedback parameter can affect inflation persistence. Doh and Yang (2023) estimate that when markets expect a change in inflation to yield a smaller policy rate change, then current inflation is more correlated with future inflation, prolonging inflationary effects. Chart 3 shows that a weaker interest rate response to inflation increases inflation persistence. The correlation measure isolates the contribution of a shift in monetary policy to changes in inflation persistence and does not assume any change in the persistence of shocks, so the chart shows changes in inflation persistence solely as an outcome of monetary policy.

Chart 3: A weaker interest rate response to inflation increases inflation persistence

Sources: Doh and Yang (2023) and authors’ calculations.

Sargent and Williams (2025) argue that if policymakers treat low inflation persistence as a given “input” to monetary policy—rather than an outcome of the policy response—they may underestimate the persistence of inflation after a shock they believed to be temporary. However, if this muted response to inflation is embedded in the private sector’s inflation expectations, then inflation persistence is likely to rise. Accordingly, policymakers may need to recognize inflation persistence as an outcome of a well-calibrated monetary policy to avoid prolonging the inflationary effects of a temporary shock. The persistent rise and slow decline in inflation during the post-COVID period provides a real-world example of this risk.

Endnotes

-

1 The oil price shock driven by the Organization of Petroleum Exporting Countries in the 1970s is an example of a persistent shock.

Article Citation

Doh, Taeyoung, and Stephen Vasiljevic. 2026. “Inflation Persistence as an Outcome of Monetary Policy.” Federal Reserve Bank of Kansas City, Economic Bulletin, February 6.

References

Bocola, Luigi, Alessandro Dovis, Kasper Jørgensen, and Rishabh Kirpalani. 2024. “External LinkBond Market Views of the Fed.” National Bureau of Economic Research, working paper no. 32610, June.

Doh, Taeyoung, and Choongryul Yang. 2023. “External LinkShocks, Frictions, and Policy Regimes: Understanding Inflation after the COVID-19 Pandemic.” Federal Reserve Bank of Kansas City, Research Working Paper no. 23-16, December.

Sargent, Thomas J., and Noah Williams. Forthcoming. “External LinkRationalizing Fed Interest Rate Decisions in the 2020s.” Journal of Political Economy: Macroeconomics.

Taeyoung Doh is a senior economist at the Federal Reserve Bank of Kansas City. Stephen Vasiljevic is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Taeyoung Doh

Senior Economist