In mid-March, the Federal Open Market Committee cut the benchmark interest rate to near zero, reviving debates over negative interest rate policy in the United States. At the core of this debate is uncertainty about whether negative interest rates would generate the desired expansionary effects on the economy. Although the Federal Reserve controls the nominal interest rate, the real interest rate—the nominal interest rate minus expected inflation—is what affects investment and consumption. For example, households are more likely to spend today if the cost of borrowing a dollar falls (that is, if the nominal rate declines), other things equal, or if they think an item will be more expensive in the future (that is, if their inflation expectations rise), other things equal. As a result, the effects of changes in nominal interest rates—and, thus, the potential effects of negative interest rates—depend partly on inflation expectations.

To highlight the role of inflation expectations in determining the real interest rate, Table 1 shows the real interest rate’s response to changes in the nominal interest rate during different policy environments. The first two columns represent a typical easing cycle during the 1990s or early 2000s, prior to the financial crisis. Column 1 shows typical pre-crisis monetary policy during a boom: the nominal interest rate is well above zero at 6 percent and inflation expectations are at 2 percent, resulting in a real rate of 4 percent. Column 2 shows the typical pre-crisis response during a recession: policymakers cut nominal rates substantially from 6 percent to 1 percent and inflation expectations remain anchored at 2 percent, resulting in a real rate of −1 percent. In this environment, the high nominal rates during expansions give policymakers enough space above the zero lower bound to effectively control real rates during recessions.

Table 1: Real Interest Rate Response to Changes in Nominal Interest Rate

Notes: Hypothetical real interest rates are calculated as nominal interest rates minus inflation expectations. Columns 5 and 6 show recessionary responses with negative interest rate policy (NIRP).

Source: Authors’ calculations.

However, the policy environment changed after the 2008 financial crisis. Column 3 of Table 1 shows typical monetary policy during a post-crisis boom: although inflation expectations remain well anchored at 2 percent, the nominal rate is at 2 percent instead of 6 percent. This lower nominal interest rate relative to the pre-crisis boom means policymakers have less space to achieve a large decline in the nominal rate in the event of a recession (assuming the nominal rate is unable to fall below zero, as was historically believed to be true). Indeed, Column 4, which illustrates monetary policy during a post-crisis recession, shows that cutting nominal rates to zero with anchored inflation expectations only results in a 2 percentage point decline in the real rate.

Over the last decade, several countries have taken their nominal rates below zero, showing that negative interest rate policy is possible; however, it is unclear where the true lower bound lies. Theoretically, rates can go as negative as policymakers wish (Agarwal and Kimball 2019). Practically, Switzerland and Denmark have cut their policy rates to the lowest level of any economies so far: −0.75 percent. We therefore consider the effect of reducing the nominal rate to −1 percent.

Columns 5 and 6 of Table 1 show the resulting effects on the real rate when the nominal rate is not constrained by the zero lower bound. In Column 5, which assumes inflation expectations remain at 2 percent, the real rate falls to −3 percent, 3 percentage points lower than its level before the recession (Column 3). Although this reduction is greater than the 2 percentage point reduction achieved while policy was constrained by the zero lower bound (Column 4), it is still short of the 5 percentage point reduction in the real rate achieved before the crisis (Column 2 compared with Column 1). Column 6 shows that if inflation expectations rise from 2 percent to 4 percent, the real rate declines by the full 5 percentage points to −5 percent._ Together, these examples illustrate that a negative interest rate policy in line with what other countries have attempted must raise inflation expectations to provide the expansionary power available prior to the 2008 financial crisis.

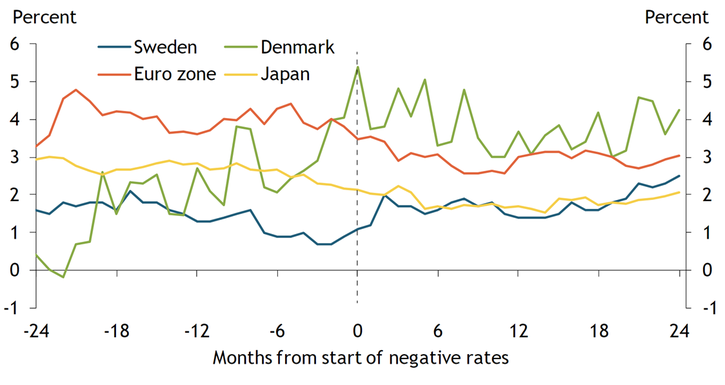

However, inflation expectations have declined following the introduction of negative rates in other countries, suggesting this expansionary power may be difficult to achieve._ Chart 1 shows household inflation expectations for Sweden (blue line), Denmark (green line), the euro zone (orange line), and Japan (yellow line) in the 24 months before and after the introduction of negative interest rates. Although inflation expectations can be measured in many ways, we use household surveys because they have been shown to best proxy for the inflation expectations of price setters when estimating the Phillips curve._

Chart 1: Inflation Expectations during Periods of Negative Interest Rate Policy

Source: Coibion, Gorodnichenko, and Ulate (2019).

Only Sweden, “the poster child for negative interest rate success,” saw inflation expectations rise after introducing negative interest rate policy (Bryan 2016). Swedish inflation expectations have been the best-case scenario for negative interest rate policy: they trended down from 2012 through 2014 and almost immediately turned up in 2015 after negative rates were introduced. This rise in inflation expectations amplified the effect of Sweden’s negative interest rate policy on real rates, consistent with the country’s relatively strong growth and realized inflation after the introduction of negative rates.

Although Denmark, like Sweden, is a Scandinavian member of the European Union that maintains its own currency, its inflation expectations after imposing negative rates look starkly different. Denmark’s Nationalbank first set a negative overnight deposit rate in July 2012, after which inflation expectations trended down for a year. As a result, Danish inflation expectations failed to amplify the decline in real rates and likely worked against the expansionary effects of negative interest rate policy.

Inflation expectations also declined after negative rates were introduced in the euro zone. The European Central Bank’s deposit rate has been negative since June 2014, making the euro zone the largest economy to conduct negative interest rate policy so far. Inflation expectations remained flat or even declined for the following two years, again likely limiting the expansionary effects of negative interest rate policy.

Inflation expectations also fell after negative rates were introduced in Japan, the most recent country to implement negative interest rate policy. Japan provides an especially interesting case study because previous evidence suggests Japan is in an expectations-driven liquidity trap—in such a trap, producers expect low demand and cut their prices, thereby causing higher real interest rates and low demand due to disinflation._ Glover (2019) shows that if a recession is caused by an expectations-driven liquidity trap, negative interest rates are almost certainly contractionary and decrease inflation expectations. Consistent with that theory, the yellow line in Chart 1 shows that household inflation expectations continued to fall immediately after the Bank of Japan introduced negative interest rates in January 2016.

This result parallels the previously documented decline in market-based measures of medium-run inflation expectations following the Bank of Japan’s introduction of negative rates (Christensen and Spiegel 2019). Although negative rates may not have caused Japan’s inflation expectations to fall, the country’s low inflation expectations were nevertheless unable to reduce real rates beyond the nominal rate’s decline to −0.1 percent.

In the United States, the federal funds rate is now effectively at zero, making further reductions impossible without going negative. However, inflation expectations have fallen in most countries that have used negative interest rates, suggesting the policy may not be as expansionary as proponents hope.

Endnotes

-

1 De Groot and Haas (2020) provide an example of how negative rates could cause inflation expectations to rise. They show that the tendency for nominal rates to change slowly means that negative rates maintain an expansionary policy stance even after a recession ends.

-

2 We cannot identify the path that inflation expectations in these countries would have taken without negative rates. These case studies are results-oriented and simply examine whether inflation expectations have provided an expansionary boost to negative interest rate policy.

-

3 Coibion and Gorodnichenko (2015) show the power of household survey expectations in estimating Phillips curves for the United States. Similarly, Coibion, Gorodnichenko, and Ulate (2019) show that household inflation expectations affect realized inflation in a broad sample of countries, including those with negative rates.

-

4 Aruoba, Cuba-Borda, and Schorfheide (2018) estimate time-varying probabilities of both the United States and Japan being in an expectations-driven liquidity trap. Their estimated probability for Japan is typically 100 percent for the 2000–15 period.

References

Agarwal, Ruchir, and Miles S. Kimball. 2019. “External LinkEnabling Deep Negative Rates to Fight Recessions: A Guide.” International Monetary Fund, working paper 19/84, April.

Aruoba, S. Borağan, Pablo Cuba-Borda, and Frank Schorfheide. 2018. “External LinkMacroeconomic Dynamics near the ZLB: A Tale of Two Countries.” The Review of Economic Studies, vol. 85, no. 1, pp. 87–118.

Bryan, Bob. 2016. “External LinkThere’s Only One Country in the World Where Negative Interest Rates Are Working.” Business Insider, April 12.

Christensen, Jens H. E., and Mark M. Spiegel. 2019. “External LinkAssessing Abenomics: Evidence from Inflation-Indexed Japanese Government Bonds.” Federal Reserve Bank of San Francisco, working paper 2019-15, October.

Coibion, Olivier, and Yuriy Gorodnichenko. 2015. “External LinkIs the Phillips Curve Alive and Well After All? Inflation Expectations and the Missing Disinflation.” American Economic Journal: Macroeconomics, vol. 7, no. 1, pp. 197–232.

Coibion, Olivier, Yuriy Gorodnichenko, and Mauricio Ulate. 2019. “External LinkIs Inflation Just Around the Corner? The Phillips Curve and Global Inflationary Pressures.” AEA Papers and Proceedings, vol. 109, pp. 465–69, May.

de Groot, Oliver, and Alexander Haas. 2020. “External LinkThe Signalling Channel of Negative Interest Rates.” Centre for Economic Policy Research, discussion paper no. DP14268, January.

Glover, Andrew. 2019. “Negative Nominal Interest Rates Can Worsen Liquidity Traps.” Federal Reserve Bank of Kansas City, Research Working Paper no. 19-07, October.

Andrew Glover is a senior economist at the Federal Reserve Bank of Kansas City. Emily Pollard is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Andrew Glover

Research and Policy Advisor