This issue of the Tenth District Consumer Credit Report begins with an analysis of recent levels of average total consumer debt and average revolving debt in the Tenth District and the United States in light of trends over the last several quarters. To offer additional perspective, the report proceeds with an evaluation of consumer debt relative to personal income and a comparison of average consumer debt with median consumer debt. The discussion then turns to delinquency rates, which are important indicators of consumer financial stress. Finally, the special topic in this issue examines increasing delinquency rates on auto loans and credit cards.

Average Consumer Debt

Consumer debt is a critical element of financial well-being for individuals and families. When taking on debt, consumers borrow against future income. Servicing the debt (making required payments for principal and interest) not only constrains spending from future income but also limits the ability to save and may impede progress in meeting financial goals. Moreover, indebtedness is an important factor in accessing future credit, as lenders often use the debt-to-income ratio to assess a consumer’s ability to repay. Research shows consumer debt is a principal determinant of financial insecurity, and indebtedness can induce high levels of both individual and marital stress.1 Still, debt also can be used for gain. Examples are financing an education that leads to higher lifetime earnings or financing an appreciating asset, such as a home.2

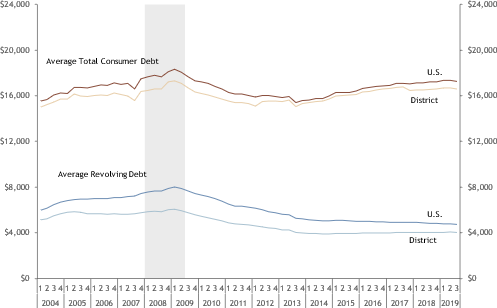

I calculate average consumer debt to provide insight into the debt burden of a typical individual in the District and the nation, or the debt burden of individuals in the aggregate. Importantly, this calculation is the average debt for those with credit reports. About 9 percent of the U.S. adult population does not have a credit report, but they often accumulate debt nonetheless through nontraditional financial institutions, such as payday lenders or pawnbrokers, or they may owe friends and family.3 The raw data for the calculations are inflation-adjusted and seasonally-adjusted. Average consumer debt in the District, measured as all outstanding debt other than installment mortgages, was $16,594 in the third quarter of 2019, compared with $17,264 nationally, both little changed from the previous quarter.4 Typically, average consumer debt is moderately lower in the District than in the nation (3.3 percent lower in the third quarter).

Households pared balance sheets immediately following the Great Recession. Both District and national average consumer debt then rose at a solid pace between 2013 and 2017. Since then, annual growth in average consumer debt has leveled off in the United States to 0.6 percent. In the District, average consumer debt has declined over the past two years at an annual rate of 0.5 percent.5

Revolving debt has declined consistently since the Great Recession (Chart 1). Revolving debt is the outstanding balance on open lines of credit, meaning that more credit is made available as debt is repaid. For most consumers, revolving debt comes from using credit cards and home equity lines of credit (HELOCs).

Consistently declining levels of revolving debt is an encouraging trend. Revolving debt has greater potential to cause problems for consumers than installment debt for several reasons (installment loans are amortized over a finite payment period with no [automatic] expansion of credit upon payment). First, revolving debt typically carries a much higher interest rate, particularly if it is unsecured (credit cards typically are unsecured, while HELOCs are secured). In the third quarter, the average annual percentage rate (APR) on credit cards was 15.1 percent, compared with 5.3 percent for a 48- or 60-month new auto (installment) loan.6 Second, payments on revolving loans often are structured in a way that can lead to an exceedingly long repayment period.7 Third, increased revolving debt may lead to a higher credit utilization rate (debt relative to credit limit), which lowers credit scores.8 Finally, while installment loans usually finance appreciating or long-lived assets, revolving credit often finances depreciating assets or consumables.

Chart 1: Outstanding Consumer Debt per Consumer and Revolving Debt per Consumer

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; U.S. Bureau of Labor Statistics; HAVER Analytics; staff calculations.

Notes: Data are inflation-adjusted using the Consumer Price Index and seasonally adjusted using the Census Bureau's X11 procedure. Excludes first mortgages and junior installment mortgages. Gray bar indicates recession.

Perspectives on Consumer Debt

Average consumer debt is an informative indicator of the debt burden facing the typical consumer, but it is not the only indicator. For additional perspective, I consider consumer debt from two alternative angles: consumer debt relative to per capita income over time and median debt relative to average debt.

Debt relative to income is a signal of ability to pay. In the July issue of the Tenth District Consumer Credit Report, the special topic compared average debt to median household income across geography. For example, while average consumer debt in Colorado consistently is the highest in the District, household income also is the highest, suggesting that higher average consumer debt in Colorado ($18,998 in the third quarter) is not necessarily more burdensome in the aggregate than the relatively low level of average consumer debt in other District states. Indeed, the analysis suggested the aggregate burden roughly is the same in Colorado and Kansas (where average debt was $15,280 in the third quarter). In this issue, I compare average consumer debt to per capita income over time for the District and the nation.

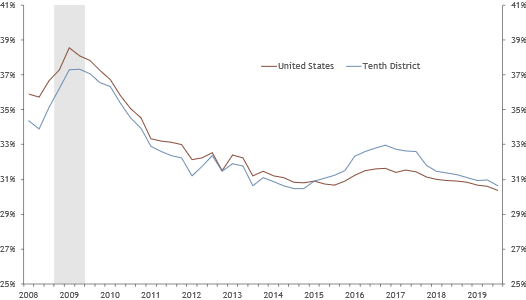

Chart 2 shows average consumer debt divided by per capita personal income (debt-to-income ratio) for the District and the nation since the first quarter of 2008. Income and debt are distributed differently across the population. Thus, the typical consumer in terms of debt is very unlikely to be the typical consumer in terms of income. Still, the pattern of average debt relative to per capita income provides insight on the ability of consumers to pay on average.

Chart 2: Average Consumer Debt as a Share of Annual Per Capita Income

Notes: Missouri receives a 30.5 percent weight and New Mexico receives a 70.3 percent weight in the District calculations. Consumer debt excludes first mortgages and junior installment mortgages. Data are seasonally adjusted using the Census Bureau's X11 procedure. Gray bar indicates recession.

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; U.S. Census Bureau; U.S. Bureau of Economic Analysis; HAVER Analytics; staff calculations.

The debt-to-income ratio has moved roughly in tandem for the District and the nation. Debt to income rose sharply before the Great Recession when it peaked at 37.3 percent in the District and 38.5 percent nationally. Following the Great Recession, income growth was modest, but consumer debt declined substantially, driving down the debt-to-income ratio in both the District and the nation to 30.9 percent by the first quarter of 2015. The debt-to-income ratio then declined on a modest path nationally and was 30.4 in the third quarter of 2019. The District diverged from the nation between 2015 and 2017. The debt-to-income ratio rose to 33 percent in the District while remaining flat nationally. The divergence was due entirely to a fall in per capita income growth in the District relative to the nation. Growth in average consumer debt was roughly the same. Adjusted for inflation, per capita income growth was flat to negative in the District while increasing moderately in the nation. Economic growth weakened somewhat nationally during the period, but more so in the District, due in part to its greater reliance on the then-troubled energy and agriculture sectors.

The debt-to-income ratio in the District since has aligned more closely with the national ratio. Per capita income grew moderately faster in the District over the last two years, but more importantly, annual growth in consumer debt was significantly greater nationally (0.6 percent, adjusted for inflation) than in the District (‒0.5 percent). In the third quarter, the debt-to-income ratio in the District was 30.7 percent.

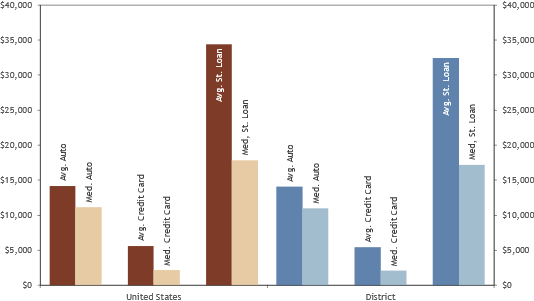

Another way to gain perspective on consumer debt is to compare average debt with median debt. Median consumer debt for the District in the third quarter was $10,543, meaning half of individuals (with credit reports) had consumer debt less than $10,543; for the other half, consumer debt was greater than $10,453. Median debt is considerably lower than average consumer debt in the District ($16,594). Similarly, median U.S. consumer debt was $10,839, compared with an average debt of $17,264. The gap between average and median debt is especially large for student loan debt. Average student loan balance, which was $34,383 in the first quarter of 2019 nationally ($32,434 in the District) (Chart 3), is widely reported, but the median shows that half of all student loan borrowers had student loan balances under $17,820 ($17,180 in the District). Median auto loan balance and credit card balance are also significantly smaller than their averages.

Chart 3: Average and Median Debt Balance, Third Quarter 2019

Notes: Average Balance is for those with an account. Some credit cards have zero balances.

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; staff calculations.

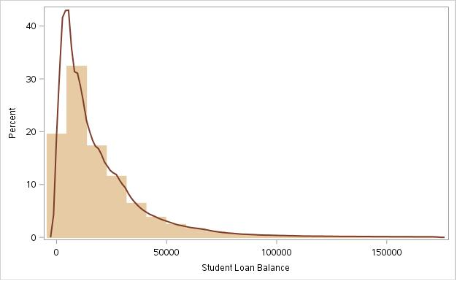

The reason average debt is so much greater than median debt is that there are a relatively small number of consumers who have very large individual debt balances. By contrast, the balances of consumers with a debt balance below the average tend to bunch together near the average. Large individual debt balances pull up the average, but not the median. Chart 4 illustrates this asymmetry by showing the national distribution of student loan balances. The distributions of auto loan and credit card balances are also similarly skewed, but to a lesser degree than student loan balances.

Chart 4: Distribution of Student Loan Balances, U.S., Third Quarter 2019

Notes: Note: Each bar in the histogram (light khaki) represents 5 percent of outstanding student loan balances for those with credit reports; thus, the histogram has 20 “bins.” The brown line is a kernel density estimate. It is a non-parametric, smooth representation of the likely population distribution derived from the CCP/Equifax sample. As the number of bins increases to the number of observations, the histogram looks increasingly like the kernel density estimate. Created using individual consumers’ aggregate student loan balance and the SGPLOT procedure in SAS.

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax.

Delinquency

Delinquency is the most salient indicator of financial distress, and there can be significant repercussions. Credit delinquency is a fundamental determinant of credit standing as viewed by financial institutions, and delinquency is the most critical factor in computing credit scores.9 Thus, delinquencies make accessing additional credit much more difficult, and many consumers have problems accessing credit. In the Federal Reserve Board’s Survey of Household Economics and Decision-Making (SHED), roughly 23 percent of those who applied for credit in the year preceding the survey data were denied credit, and 8 percent were offered less than requested.10 Finally, delinquency is a precursor to debt in collections, which can lead to the sale of the debt to third-party collectors.11 Third-party collectors often use more aggressive collection tactics than the original lenders. Debt in collections also can lead to the loss of property through civil judgments or bankruptcy and the loss of potentially attractive financial opportunities.

I construct measures of delinquency using the share of consumers with at least one account in the credit category (such as credit cards) who are 90 days or more past due on at least one account in that category.12 Thus, if a consumer has four credit card accounts, and one is delinquent while the others are current, the consumer is considered delinquent. As a result, the delinquency rates in this report generally are higher than those determined by the share of delinquent accounts or the share of outstanding balances that are delinquent.13 Moreover, I include severely derogatory accounts in the delinquency rate, which in some cases include charged-off debt. Financial institutions generally do not include charged-off debt in their internal delinquency calculations and therefore typically report lower delinquency rates.

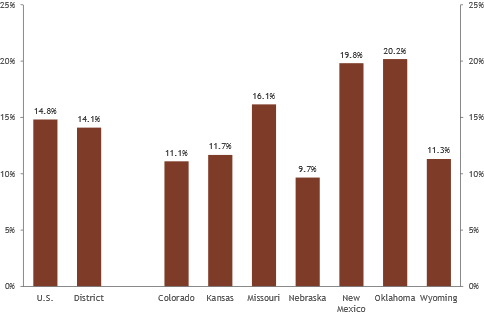

In the third quarter, 14.1 percent of District consumers were delinquent on at least one credit account, compared with 14.8 percent of consumers nationally (Chart 5). Auto loans, credit cards and student loans together account for the large majority of consumer debt (installment mortgages are the largest component of total debt). Delinquency rates on most types of debt have fallen over the last three years, but delinquencies on credit cards and auto loans have been increasing steadily.

Chart 5: Consumer Credit Delinquency Rates

† "Any Account" is the share of all consumers who have at least one open credit account and at least one past due credit account and includes accounts not otherwise reported in the chart. For all other categories, the delinquency rate is the share of consumers with at least one account in that category who have at least one account 90 or more days past due in that category. For example, the credit card delinquency rate is the share of all consumers with at least one credit card who have at least one credit card 90 or more days past due. Delinquency rates include charge-offs.

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; staff calculations.

The calculated student loan delinquency rate in Missouri dropped sharply (6 percentage points from the second to third quarters in 2019), suggesting there may be a problem with the data, which we are investigating.14 Subtracting Missouri, the District student loan delinquency rate still fell sharply, to 14.4 percent from 16 percent a year ago. Greater take-up of federal income-based repayment plans likely is a significant factor in the drop in student loan delinquency rates. In the first quarter of 2016, there were 4.5 million student loan borrowers enrolled in income-based repayment programs. The number of enrollees increased to 7.1 million by the first quarter of 2018 and 7.6 million by the first quarter of 2019.15

Delinquencies on mortgages have continued to fall. In the District, 0.9 percent of mortgages (first mortgages and non-revolving junior liens) were 90 or more days past due, essentially unchanged from a year ago. The national mortgage delinquency also was little changed compared with a year ago at 1.2 percent. HELOC delinquencies remain exceptionally low, also dropping 0.1 percentage point in the District and nationally to 0.5 percent and 0.7 percent, respectively.

Delinquency rates vary significantly by District state (Chart 6). In the third quarter, the share of consumers who were delinquent on at least one open account ranged from 9.7 percent in Nebraska to 20.2 percent in Oklahoma. Oklahoma has higher delinquency rates across the board. For example, the student loan delinquency rate is 18 percent, (down significantly from 20.3 percent in the previous quarter), compared with 14.4 percent in the District. Auto and credit card delinquencies in Oklahoma are 11.2 percent and 9.7 percent, respectively, compared with District delinquency rates of 8 percent and 7.7 percent, respectively. Higher delinquency rates in Oklahoma may reflect a softening economy due in large part to a troubled energy sector. The New Mexico economy was late into the recovery and just recently has begun to see substantial growth, which may, in part, explain relative high delinquency rates in that state.

Chart 6: Delinquency on Any Account, District States, Third Quarter, 2019

Notes: At least 90 days past due. "Any Account" is the share of all consumers who have at least one open credit account and at least one past due credit account and includes accounts not otherwise reported in the chart. Missouri and New Mexico data are for the Tenth District portion of the state only.

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; staff calculations.

Summary

Recently, District consumers have curtailed borrowing, following significant increases since 2013. Nationally, growth in inflation-adjusted average consumer debt has decelerated significantly to a modest annual rate of 0.6 percent, but average consumer debt has declined at an annual average of 0.5 percent in the District. Average levels of revolving debt have continued to fall.

Debt-to-income ratios show a significant deleveraging by individuals, and presumably families, following the Great Recession. Despite a temporary divergence upward by the District in 2015-17, District and national debt-to-income ratios are closely aligned, continue to fall modestly, and currently are at historically low levels. Median debt balances are significantly smaller than average balances. Medians may be more representative of the typical consumer than average balances, depending on how the analyst wants to address the reality that some consumers have very large balances.

While average consumer debt loads have remained in check, delinquency rates in some categories warrant further monitoring. In particular, while delinquency rates have fallen for most forms of credit, they are rising steadily for auto loans and credit cards. Declining student loan delinquency rates could, at least in part, be a result of policy. Further, interest rates remain near historically low levels. Rising delinquencies eventually could spill over into other types of credit, which again bears close monitoring.

In This Issue: Auto and Credit Card Delinquencies

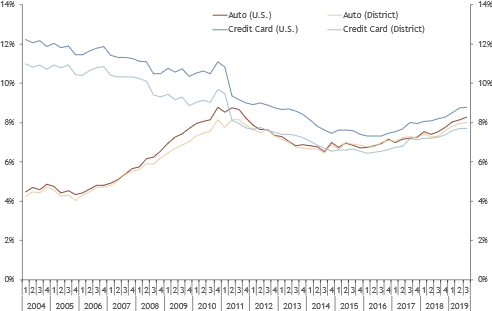

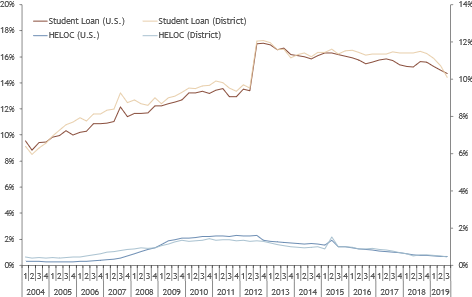

Delinquency rates for auto loans and credit cards have continued to increase, despite overall healthy economic indicators in the United States, such as a tight labor market and moderate growth in personal income. More striking is that auto and credit card delinquencies have been increasing as delinquency rates for other forms of credit have declined. Chart 7 shows the trends in auto and credit card delinquencies for the last 15 years, while Chart 8 shows the countervailing trends for student loans and HELOCs.

The patterns in auto and credit card delinquencies were dramatically different pre-recession. Delinquencies on auto loans began to climb well before the Great Recession, rising from 4 percent in the District in 2005 to its peak of 8.1 percent in 2011 (Chart 7). In contrast, credit card delinquencies began declining at least by 2004 as auto delinquencies were increasing. Auto and credit card delinquencies then began to move in tandem following the recession, first falling but then, by 2016, steadily increasing.

Chart 7: Auto Loan and Credit Card Delinquency Rates

Notes: At least 90 days past due. The delinquency rate is the share of consumers with at least one account in that category who have at least one account 90 or more days past due in that category. Delinquency rates include charge-offs. Data were seasonally adjusted using the Census Bureau's X11 procedure.

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; U.S. Census Bureau; staff calculations.

Chart 8: Student Loan and HELOC Delinquency Rates

Notes: At least 90 days past due. The delinquency rate is the share of consumers with at least one account in that category who have at least one account 90 or more days past due in that category. Delinquency rates include charge-offs. Data were seasonally adjusted using the Census Bureau's X11 procedure.

Sources: Federal Reserve Bank of New York Consumer Credit Panel/Equifax; U.S. Census Bureau; staff calculations.

The credit card delinquency rate in the District was 7.7 percent in the third quarter, its highest level in seven years. One year ago, the credit card delinquency rate was 7.3 percent, and in the third quarter of 2016, it was 6.5 percent. Nationally, the credit card delinquency rate increased to 8.8 percent from 8.2 percent a year earlier and 7.3 percent in the third quarter of 2016.

In the third quarter of 2019, the delinquency rate on auto loans was 8 percent in the District, up sharply from 7.3 percent one year earlier and 6.5 percent in the third quarter of 2016. The same pattern is evident nationally, but more stark. The third quarter 2019 delinquency rate was 8.3 percent, up from 7.5 percent one year ago and 6.9 percent in the third quarter of 2016. Auto delinquency rates in both the District and the nation are close to their recession-era peaks, which were 8.2 percent and 8.7 percent, respectively, in the second quarter of 2011.

Although trends in credit card and auto delinquencies are very similar post-recession, the stories behind the trends are in some ways quite different.

The increase in credit card delinquencies may be driven in part by an increased presence of younger borrowers in the credit card market, who, as a group, have higher delinquency rates.16 The CARD Act (2009) limited credit card marketing and issuance to college students, which drove participation in the credit card market by younger borrowers to just 41 percent in 2012.17 Subsequently, as lending standards were relaxed, participation has increased to 52 percent. Since 2016, the delinquency rate for young borrowers, based on share of balance 90 or more days past due, has increased from 6.9 percent to 8.1 percent (expressed as percent of total balance).18 The comparable delinquency rate was 6.1 percent for those ages 30-39 and 5.2 percent for those ages 40-49 in the first quarter.

Another potential factor in increased credit card delinquencies is that interest rates have been increasing in recent years.19 This increase might be an unintended consequence of the CARD Act if issuers raised interest rates on credit cards to make up for forgone fees, which could make debt management more challenging. Research suggests that about 50 percent of credit cards saw an increased interest rate in the year following the CARD Act.20

Developments in the subprime market may also be a factor. Compared with the immediate post-recession period, lending standards have eased, particularly for private label (such as retailers’) cards.21 On average, fewer credit cards are held now than in past years, but it is primarily prime (credit score 660-720) and super prime (credit score above 720) consumers who are holding fewer cards.22 Cardholding has increased for subprime consumers and now is near pre-recession levels. Finally, the credit card repayment rate has increased, but largely due to prime+ cardholders paying off balances in full, using their credit cards largely to accrue rewards.23 Repayment rates for subprime cardholders have declined.

The recent rise in credit card delinquencies has been driven largely by private-label credit cards, such as those issued by retailers. While delinquencies on private-label cards have increased significantly, delinquencies on general-purpose cards (typically bank-branded MasterCard or Visa cards, American Express, etc.) have been fairly steady, increasing very modestly.24

As with credit cards, younger borrowers are much more likely to be delinquent on auto loans, and delinquencies on auto loans by young people have been steadily increasing.25 Some attribute this problem to the proliferation of student loan debt. But unlike credit cards, auto loan originations to this group have grown much more slowly than for other age groups.26

From a macroeconomic perspective, auto loans may be more difficult to manage than credit cards. While the economy remains strong with the unemployment rate at historical lows (3.5 percent in November), wage growth has not materialized to the degree it often does during economic recovery. In the face of an economic shock, one may be able to manage credit card debt by paring payment to their minimum, while installment loans like auto loans have fixed payments.27 Ideally minimum payment would be a short-term approach until a more sustainable budget could be developed. The usual minimum payment is 1-3 percent of the balance. Assuming a minimum payment of 2 percent of the outstanding balance and an interest rate of 15.1 percent, it would take almost 28 years to repay a $5,000 balance, even in the absence of additional borrowing.28

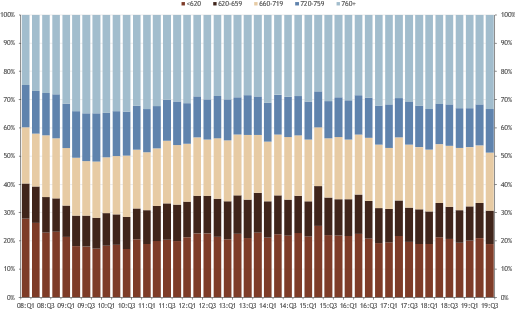

Also, as with credit cards, development in the subprime market have influenced rising delinquency rates. Auto debt continues to climb, due largely to new originations. During the housing boom that preceded the financial crisis, as mortgage debt grew, subprime borrowers entered the market at increasing rates, making up a larger share of the market. The reverse has been true in the auto loan market, where prime borrowers are making up an increasing share of all borrowers (Chart 9). In the last two years, the share of auto loan balances held by subprime borrowers fell from 19.7 percent to 18.9 percent.29 However, while delinquency rates on prime borrowers have held steady or increased only modestly, delinquency rates for subprime borrowers have increased significantly.30 The increased share of auto loans going to prime borrowers has only partially offset the increase in delinquency rates among subprime borrowers. Thus, while the subprime share of total outstanding auto loan balance is near a record low, subprime delinquencies appear to be driving the overall increase in auto loan delinquency rates.31

Chart 9: Share of Total Auto Balance by Credit Scores

Sources: Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit [datafile]; staff calculations.

Summary

While delinquency rates for most credit types continue to decline, delinquency rates on auto loans and bank cards have climbed significantly in the last two to three years, and at an increasing rate. Several factors are at play. Youth have higher rates of default, which some attribute to increasing student debt loads. But while young people have entered the credit card market in increasing numbers, their share of aggregate auto loan balance has been declining. Thus, higher delinquency rates for young people are likely more a factor in rising credit card delinquencies than auto loan delinquencies. The subprime market may be driving delinquencies. In the credit card market, subprime borrowers are attaining new credit more quickly and repaying them more slowly than prime+ borrowers. In the auto loan market, although the subprime share of auto loan balance and originations has declined, the decline is not sufficient to offset rising delinquency rates among subprime borrowers. While higher delinquencies have not materialized in other credit types, the significantly higher delinquency rates for autos and credit cards indicate some individuals and families are struggling to meet debt obligations. Delinquencies on other credit types bear watching to see if they too begin to turn upward.

Endnotes

-

1 [1] Annamaria Lusardi, Olivia S. Mitchell and Noemi Oggero, 2018, “External LinkThe Changing Face of Debt and Financial Fragility at Older Ages,” American Economic Review Papers and Proceedings, vol. 108, no. 2, pp. 407–411; Luisa Anderloni, Emanuele Bacchiocchi and DanielaVandone, 2012, “External LinkHousehold Financial Vulnerability: An Empirical Analysis,” Research in Economics, vol. 66, no. 3, pp. 284‒296; Lucia F. Dunn and Ida A. Mirzaie, 2016, “External LinkConsumer Debt Stress, Changes in Household Debt, and the Great Recession,” Economic Inquiry, vol. 54, no. 1, pp. 201‒214.

[2] The return to education varies significantly by individual, depending on many factors. See Judith E. Scott-Clayton, 2016, “External LinkEarly Labor Market and Debt Outcomes for Bachelor’s Degree Recipients: Heterogeneity by Institution Type and Major, and Trends Over Time,” CAPSEE Working Paper, Columbia University, Teachers College, Community College Research Center, Center for Analysis of Postsecondary Education and Employment. Homeownership is not always wealth-creating because house prices can fall. See Jordan Rappaport, 2010, “The Effectiveness of Homeownership in Building Household Wealth,” Economic Review, Federal Reserve Bank of Kansas City, vol. 95, no. 4, pp. 35‒65.

[3] Caroline Ratcliffe, Signe-Mary McKernan, Brett Theodos and Emma Kalish, 2014, External LinkDelinquent Debt in America, Urban Institute, July.

[4] Beginning with this issue, I split joint accounts for all account types; that is total balance = (total balance of individual accounts) + (1/2)(total balance of joint accounts). I also subtract junior installment mortgages from total debt in calculating consumer debt and remove U.S. territories (American Samoa, the Federated States of Micronesia, Guam, the Marshall Islands, the Northern Mariana Islands, Puerto Rico, Palau, the U.S. Virgin Islands and U.S. Minor Outlying Islands). These changes reduce average consumer debt by about $1,000 from the balance that would result if I did not split joint accounts or subtract off junior installment mortgages. Finally, beginning with this issue, I seasonally adjust the data before calculating the statistics presented in the report using the X11 procedure from the U.S. Census Bureau. Previously statistics were presented as four-quarter moving averages. The statistics in this report are therefore not directly comparable with statistics in previous reports.

[5] All annual growth rates in this report are compound annual growth rates. Specifically, the compound annual growth rate for some value (V) over n years is (Vt/Vt-n)1/n - 1.

[6] Federal Reserve Board of Governors. Data release G.19, “External LinkConsumer Credit.” Accessed Jan. 1, 2020.

[7] See special topic in this report, “Auto and Credit Card Delinquencies.”

[8] Fair Isaac Corp., “External LinkUnderstanding FICO Scores: What You Need to Know about the Most Widely Used Credit Scores,” and Federal Trade Commission, “External LinkCredit Scores.”

[9] Id.

[10] Federal Reserve Board of Governors, 2019, External LinkReport on the Economic Well-Being of U.S. Households in 2018, May. See also Kelly D. Edmiston, 2019, Tenth District Consumer Credit Report, Federal Reserve Bank of Kansas City, July 12. The SHED does not ask why individuals were denied credit, but presumably it was due to poor credit standing, or perhaps insufficient income in some cases.

[11] Consumer Financial Protection Bureau, 2016, External LinkStudy of Third-Party Debt Collection Organizations, July.

[12] For specifics on the calculation of delinquency rates for the Tenth District Consumer Credit Report and a comparison with other methods of calculating delinquency rates, see the December 2017 issue.

[13] Id.; in particular, delinquency rates determined as a share of outstanding debt that is overdue, as typically done in the Federal Reserve Bank of New York’s External LinkQuarterly Report on Household Debt and Credit, are lower because smaller balances are relatively more likely to be delinquent.

[14] An artificially low student loan delinquency rate would also affect the delinquency rate on any account, but only modestly. Thus, the delinquency rate on any account may be slightly higher than 14.1 percent. Nevertheless, the delinquency rate on any account has fallen significantly in the past year.

[15] U.S. Department of Education, Office of Federal Student Aid, “Federal Student Loan Portfolio, External LinkIDR Portfolio by Age.”

[16] Andrew Haughwout, Donghoon Lee, Joelle Scally and Wilbert van der Klaauw, 2019, “External LinkJust Released: Shifts in Credit Market Participation over Two Decades,” Liberty Street Economics blog, Federal Reserve Bank of New York, May 14.

[17] Id.

[18] Id.; delinquency rates based on share of outstanding balance that is past due typically are lower than those based on the share of consumers who have delinquent accounts, which is the method used in this report. The difference arises primarily because delinquency is more common on trade lines with lower balances.

[19] Consumer Financial Protection Bureau, 2019, External LinkThe Consumer Credit Card Market, August.

[20] Scott Nelson, 2018, External LinkPrivate Information and Price Regulation in the U.S. Credit Card Market, Master’s Thesis, Department of Economics, MIT. The CARD Act prohibited issuers from raising the interest rate charged on existing balances in most cases.

[21] Supra, note 19.

[22] Id.

[23] Id.

[24] Supra, note 20.

[25] Supra, note 19.

[26] Federal Reserve Bank of New York, 2019, External LinkQuarterly Report on Household Debt and Income [External Linkdatafile], third quarter; staff calculations.

[27] Kelly Anne Smith, 2019, “External LinkAuto Loan Delinquencies Surge Past Great Recession Rate,” Bankrate, Feb. 12.

[28] Supra, note 6.

[29] Melinda Zabritski, 2019, State of the Automotive Finance Market, Experian, second quarter.

[30] Supra, note 27.

[31] See Jason P. Brown and Colton Tousey, 2018, “Auto Loan Delinquency Rates Are Rising, but Mostly among Subprime Borrowers,” Macro Bulletin, Federal Reserve Bank of Kansas City, Aug. 15.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.