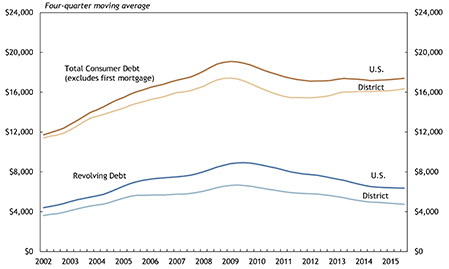

Tenth District average consumer debt, which for this report includes all outstanding debt other than first mortgages and is presented as a four-quarter moving average, inched up in the first quarter of 2015 (Chart 1).1 The uptick continued a consistent increase in District consumer debt since early 2012 and helped produce a modest overall increase of 4.7 percent since the first quarter of 2012. For the quarter, average consumer debt in the District was $16,163, up $730 from its post-recession low. National average consumer debt of $17,280 remained well above the District level. Average revolving debt in the District continued to slip, reaching $4,837, about $1,840 (28 percent) below its recession-era peak. Revolving debt is the sum of balances on open lines of credit—largely credit cards, but also equity lines of credit and other financial products. Rising total debt and declining revolving debt imply that installment debt (total debt less revolving debt) has increased significant.

Chart 1: Outstanding Consumer Debt and Revolving Debt per Consumer

Much of the growth in installment debt can be traced to two components: student loans and auto loans. Average District student loan debt for those with student loan debt increased 73 percent in the past 10 years and 3.7 percent in the past year to $26,037 (Chart 2). Average U.S. student loan debt for those with student loan debt was $27,587 in the first quarter, up 4.2 percent from a year ago and 76 percent over 10 years. The relatively rapid rise in average student loan debt is not a recent phenomenon, as the rate of increase has been fairly steady for many years. Robust growth in average student loan debt is attributable to many factors. The most important of these are rising operating costs for higher education institutions and reductions in student aid, especially grant aid.2

New auto sales dropped sharply during the recession and early in the recovery, significantly increasing the average age of automobiles in use. The aging fleet of existing autos and latent demand for new autos produced a spike in sales over the last two to three years, resulting in a significant increase in auto debt.3 Total outstanding auto debt in the United States in the last year increased 11 percent, from $875 billion to $968 billion.4 From the 2009 trough of the recession, the number of auto loans outstanding has increased 7.7 percent, and the average balance of outstanding auto loans has increased 17.0 percent. In the first quarter, average auto debt for those with auto debt was $17,094 in the District and $16,086 in the nation overall (Chart 2).

Chart 2: Outstanding Auto and Student Loan Debt per Borrower

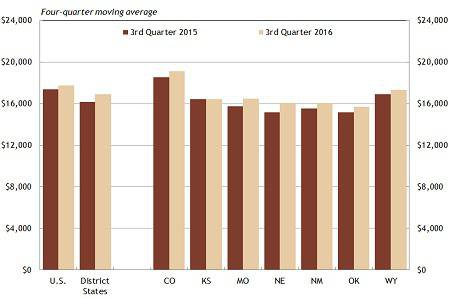

Average consumer debt varied significantly across District states, from $14,875 in Nebraska to $18,605 in Colorado (Chart 3). Coloradans consistently carry more debt than consumers in other District states, due largely to a higher cost of living—especially for housing—and above-average incomes. Consumer debt tends to move with both cost of living and income. Likewise, Nebraskans and Oklahomans typically carry relatively low debt. Lower average consumer debt in New Mexico mostly can be attributed to recent struggles in the state economy. Historically, consumer debt in New Mexico has been about on par with the District average. New Mexico consumer debt has picked up recently, increasing 3.1 percent since the fourth quarter of 2013.

Chart 3: Outstanding Consumer Debt per Consumer

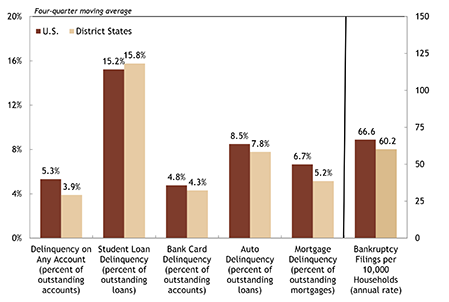

The overall credit delinquency rate in the first quarter in the District of 3.9 percent was significantly lower than the U.S. rate of 5.3 percent (Chart 4). The difference comes from much lower mortgage delinquency rates in District states. In particular, the foreclosure rate in the District was 1.0 percent in the first quarter, compared to a foreclosure rate of 1.5 percent for the nation as a whole.5 With the exception of student loan delinquencies, late bills were less common in District states than in the nation overall across all forms of debt. Auto and student loan delinquencies continued to increase at a moderate pace in the first quarter of 2015, while bank card delinquencies decreased.

Chart 4: Consumer Delinquency Rates

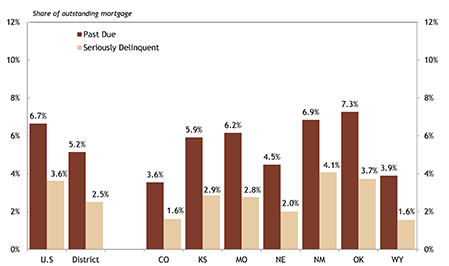

District mortgage delinquency rates continued a downward trend and remained below national rates in the first quarter (Chart 5). The District past due mortgage rate in the quarter was 5.2 percent, down from 5.8 percent one year ago. The seriously delinquent rate, which includes all mortgages 90 or more days past due or in foreclosure, was 2.5 percent, down from 2.9 percent one year earlier. U.S. serious delinquencies are consistently higher, but the difference is due mostly to a higher U.S. foreclosure rate. The past due rate for the nation over the last year fell from 7.8 percent to 6.7 percent.

Chart 5: Mortgage Delinquencies

In This Issue: Developments in the Mortgage Market

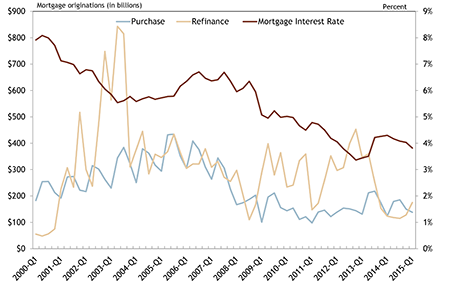

Mortgage lenders originated $313 billion in first-lien home loans in the first quarter, a 27 percent increase over the first quarter of 2014.6 About 56 percent of these mortgage originations were for refinancing.7 Refinancing activity varies significantly by quarter. Most of this volatility arises from the sensitivity of refinancing to mortgage rates. When mortgage rates drop, especially if the drop is sharp, refinance originations typically surge. In the first quarter of 2011, when the national average contract mortgage rate ranged from 4.6 percent to 4.8 percent, refinance originations totaled $148 billion (Chart 6).8

In the fourth quarter of 2012, when the national average contract mortgage rate was as low as 3.3 percent, refinance originations increased sharply to $453 billion, an increase of more than 200 percent from the first quarter of 2011. Those who refinanced home mortgages in the first quarter of 2015 are expected to jointly save more than $1.4 billion in interest costs over the first 12 months of their loans.9 In 2013 and 2014, those who refinanced home mortgages during the year are expected to save an estimated $20 billion and $5 billion, respectively, in interest payments over the first 12 months of their loans.10

Mortgages originated for purchase generally are much less volatile. Survey research suggests that borrowers are more sensitive to down payment requirements and recent changes in household wealth than they are to mortgage interest rates.11 Mortgages originated for home purchases have been steady following the housing collapse that precipitated the 2008 financial crisis. Originations for home purchase were $138 billion in the first quarter, modestly lower from the first quarter of 2014.12

Chart 6: Mortgage Originations (Purchase and Refinance)

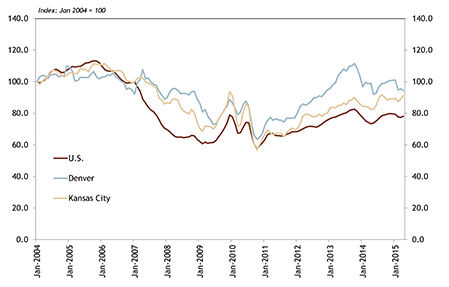

Housing market conditions also drive the origination of purchase mortgages. By October 2010, six months after the expiration of temporary homebuyer tax credits, sales of existing homes in the United States were half of the pre-crisis peak (Chart 7).13 Existing home sales in Kansas City also fell to half of their pre-crisis peak.14 In Denver, sales were off 42 percent. Three years later, existing home sales in Denver had fully recovered while Kansas City and the nation overall had made significant progress to that end. Home sales retreated in mid-2013, but have since stabilized. A limiting factor in sales of existing homes is low inventory. In March, 2015, the supply of homes for sale, measured by the number of months it would take to sell the entire inventory of homes on the market at the current sales rate, was 4.6 months, solidly in a sellers’ market. Given that U.S. sales of existing homes were down 32 percent from the pre-crisis peak, the low supply has been driven largely by low inventory rather than robust sales.

Chart 7: Existing Home Sales

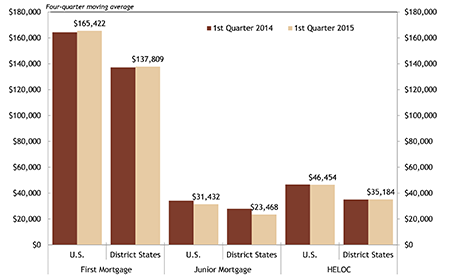

Following the pattern in sales of existing homes, mortgage debt increased sharply from 2000 through 2007 and began to increase again in mid-2012 amid rebounding home sales and home prices (Chart 8).15 The average balance on U.S. first mortgages was $165,422 in the first quarter, up 0.6 percent from the first quarter of 2014 and 33.5 percent from $135,869 in the first quarter of 2005, when sales of existing homes peaked (Chart 9). The average mortgage balance in the District followed an identical path, increasing 36 percent from $116,674 in early 2005 to $137,809. Few refinances have involved significant cash-outs since the start of the financial crisis. Although in the first quarter, 27 percent of mortgage refinances involved a loan amount that exceeded the principal refinanced by at least 5 percent, the total cash-out volume was only $7.6 billion, or 6.2 percent of aggregate refinanced originations.16 Thus, the increase in average first mortgage loan balance has come largely from new originations. Unlike the immediate pre-crisis period, however, average junior lien balance, whether installment or revolving, did not increase with first mortgages.17

Chart 8: Average Outstanding Balance on First and Junior Mortgages

Chart 9: Average Outstanding Balance on First and Junior Mortgages

Mortgage originations have increased significantly since the housing crisis. Growth in the sale of existing homes has prompted much of the increase in borrowing, but refinance activity, which can vary substantially from quarter to quarter, has been very high in some quarters, offsetting relatively low purchase originations compared to the pre-crisis period. Refinance activity is largely driven by interest rates. Fewer households own their homes than in the pre-crisis period, but the average first mortgage balance is modestly higher. Still, average first mortgage balances have moved little compared to pre-crisis growth, and secondary mortgage balances have remained stable, and in some cases, have decreased. The moderate increase in first mortgage balances likely reflects increasing home prices in many places, among other factors.

Endnotes

[1] The Tenth District includes Colorado, Kansas, the western third of Missouri, Nebraska, the northern half of New Mexico, Oklahoma, and Wyoming. In many cases in the report, data from the entire states of Missouri and New Mexico are used, in which case the label for the region is “District States.”

[2] See Kelly D. Edmiston and others, “Student Loans: Overview and Issues (Update),” Federal Reserve Bank of Kansas City, Research Working Papers 12-05, April 2013, available at https://www.kansascityfed.org/~/%20media/files/publicat/reswkpap/rwp%2012-05.pdf.

[3] Credit issues related to auto loans are discussed in detail in the third quarter, 2014 issue of the Tenth District Consumer Credit Report, available at https://www.kansascityfed.org/publicat/community/ccr/2014-3q-District-CCR.pdf.

[4] Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit [data file], May 2015, available at External Linkhttp://www.newyorkfed.org/householdcredit/2015-q1/data/xls/HHD_C_Report_2015Q1.xlsx.

[5] Lender Processing Services Inc. [datafile].

[6] Trefis, “Q1 2015 U.S. Banking Review: Mortgage Originations,” May 26, 2015, available at External Linkhttp://www.trefis.com/stock/bac/articles/298075/q1-2015-u-s-banking-review-mortgage-originations/2015-05-26.

See also, Inside Mortgage Finance, “Mortgage Origination Volume Picked Up Speed in Early 2015; Most Lenders Report Solid Gains,” Issue 2015:16, May 1, 2015, p. 3 (Table). Starting with the first quarter of 2015, home-equity lending is not included in total originations. In 2014, 5.7 percent of originations ($71 billion) were home-equity loans. Figures for 2014 presented above are adjusted for this change by Inside Mortgage Finance, but official estimates of originations prior to the first quarter of 2015 are not being revised. Data on dollar volume of originations vary by source but generally are quite similar. For the first quarter of 2015, RealtyTrac estimated $377 billion in originations (see Tanaya Macheel, “Loan Origination Activity Down in First Quarter: RealtyTrac,” National Mortgage News, May 14, 2015, available at External Linkhttp://www.nationalmortgagenews.com/origination/). The Mortgage Bankers Association has released data showing actual total originations were $278 billion.

[7] Office of the Chief Economist, Freddie Mac, 2015 First Quarter Refinance Report, April 30, 2015, available at External Linkhttp://www.freddiemac.com/finance/pdf/RefiReport2015Q1.pdf.

[8] Federal Housing Finance Agency, Monthly Interest Rate Survey, available at http://www.fhfa.gov/DataTools/Downloads/Pages/Monthly-Interest-Rate-Data.aspx.

[9] Office of the Chief Economist, 2015 First Quarter Refinance Report.

[10] Office of the Chief Economist, Freddie Mac, 2014 Fourth Quarter & Full Year Refinance Report, February 4, 2015, available at External Linkhttp://www.freddiemac.com/finance/pdf/RefiReport2014Q4.pdf.

[11] Andreas Fuster and Basit Zafar, “The Sensitivity of Housing Demand to Financing Conditions: Evidence from a Survey,” Staff Report No. 702, Federal Reserve Bank of New York, March, 2015 (revised), available at External Linkhttp://www.newyorkfed.org/research/staff_reports/sr702.pdf.

[12] Jann Swanson, “Purchase Loan Market MIA,” Mortgage News Daily, May 14, 2015, available at External Linkhttp://www.mortgagenewsdaily.com/05132015_loan_originations.asp.

[13] For detailed information about this tax credit for home purchases, see “Tax Credits for Home Buyers,” Internal Revenue Service, FS-2010-06, January 2010, available at External Linkhttp://www.irs.gov/uac/Tax-Credits-for-Home-Buyers.

[14] Only the two largest metropolitan areas in the District were examined directly for ease in exposition. Sales in Omaha and Oklahoma City are on par with the pre-crisis peak; sales in Tulsa are about 90 percent of the pre-crisis peak (regional Realtors® associations).

[15] Home prices in the District’s major cities increased 24.9 percent between March 2012 and March 2015, the latest date for which data are available (Federal Reserve Bank of Kansas City and regional residential Realtors® associations).

[16] Office of the Chief Economist, 2015 First Quarter Refinance Report [data file], April 30, 2015, available at External Linkhttp://www.freddiemac.com/finance/docs/q1_refinance_2015.xls.

[17] A junior lien is subordinate debt, meaning that, in the case of default and foreclosure, the financial institution holding the primary (first) mortgage is compensated before others with mortgages collateralized by the property. An “installment” mortgage is amortized like a first mortgage (generally referred to as a “second” mortgage), while a revolving mortgage loan (generally referred to as a home equity line of credit, or HELOC) works much like a credit card.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.