The Kansas City Fed's Community Development staff assessed how economic conditions affect lower-income communities and the broader development ecosystem in Nebraska. We expected Nebraskans to mention issues like affordable housing, childcare, and jobs, and they did. That was no surprise. But people did surprise us with other thoughts on Nebraska’s community development landscape during nearly a year of meetings and more than 3,000 road miles. For example, we were surprised to hear that a major challenge facing lower income households was lack of awareness of available programs. To address that, nonprofit leaders statewide told us they wanted to break down their silos and work more intentionally together.

Rachael Surmick, assisted by Marisa Martinez, engages residents of Nebraska City in a conversation about challenges and opportunities. Both Surmick and Martinez are community development advisors with the Kansas City Fed.

The purpose of the year-long project was to identify the challenges and opportunities facing lower income communities across the state. The assessment was based on interviews and roundtable discussions with more than 100 people working in the community development field.

We conducted the assessment in alignment with the Kansas City Fed’s mission to serve the public by promoting economic and financial stability—recognizing community development as an important pathway to achieving that goal.

Our Bank’s community development team works to promote economic development and public understanding that supports growth in all communities, including those in low- to moderate-income and rural communities.

This article first describes the approach used in the assessment and explains why we chose to use those methods. It then provides relevant definitions and context before explaining the several key themes that emerged:

- Community capacity

- Financial capacity

- Housing affordability and preservation

- The intersection between transportation and workforce participation.

People mentioned many community development challenges; however, these four themes were discussed by most participants.

What does “low- to moderate-income” look like in Nebraska?

We frequently refer to low- to moderate-income (LMI) communities and households. A handful of measures are used to define LMI communities. The Community Reinvestment Act (CRA), a foundational piece of community development legislation passed in the late 1970s, encourages financial institutions to help meet the credit needs of communities in which they do business, including LMI neighborhoods. The CRA uses 80% or below of area median income (AMI) to define moderate-income and 50% or below for lower income. External LinkFederal Poverty Guidelines can also be a good measure for identifying lower income households.

Participants in the O’Neill roundtable pose for a selfie with Rachael Surmick.

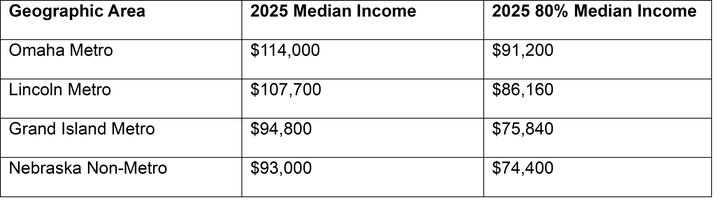

In Nebraska, the federal government subdivides the states into four geographic areas to define median income: the Omaha metropolitan area, the Lincoln metropolitan area, the Grand Island metropolitan area, and the Nebraska non-metropolitan area.

The federal poverty level gives a sense of the number of residents considered low-income. In 2025, the federal poverty level for a family of four was $32,150. In Nebraska, approximately 12% of families live at or below 150% of the federal poverty level, or $48,225. This figure rises to 13.8% of families in Omaha and 12.6% of families in Lincoln._

To put both measures in perspective, here are some jobs Nebraskans hold and their annual mean wage:_

- Childcare workers: $29,260

- Fast food cook: $29,060

- Computer user support specialists: $59,240

- Child, family, and school social workers: $53,940

- Elementary school teachers: $59,920

- Medical records specialists: $54,580

- Pest control workers: $42,390

- Automotive service technicians and mechanics: $51,950

- Architectural and engineering managers: $135,650

- Personal financial advisor: $126,990

How did we approach this study in Nebraska?

This exploration leveraged qualitative research methods to learn directly from people serving lower-income communities and working in the community development field across Nebraska. This allowed us to gather myriad perspectives of people working in affordable housing, digital access, early childhood care, economic development, philanthropy, small business development, social services, and workforce development.

We used a blend of appreciative inquiry and asset-based community development approaches._ These approaches build upon existing community strengths to address challenges instead of focusing solely on what the community lacks.

Surmick invites Nebraska City participants to share what’s working in their community.

How did we use key informant interviews?

We used key informant interviews to gather detailed information from some 50 individuals across the state. Of those individuals, 27% came from non-metro Nebraska, 41% from the Lincoln and Lancaster County area, and 32% from the Omaha metropolitan area.

Each interview consisted of at least three questions:

- What do you see as some of the key challenges facing low- to moderate-income households that your organization serves across Nebraska?

- Where are there opportunities to increase the economic well-being of low- to moderate-income households and communities in Nebraska?

- What issues do you wish we (in the general sense) were talking about more because they are not discussed enough?

Additional questions included:

- What strengths currently exist that support lower income communities?

- What are the priority challenges and opportunities affecting lower income communities?

- Who/Where do you go for resources and support?

The Nebraska City roundtable drew a crowd of people working in the community development field.

How did we use roundtable community discussions?

Organizations that support lower income communities know the barriers and challenges lower income communities face are interconnected. To capture a comprehensive view of current conditions we hosted roundtable discussions with representatives of affordable housing, workforce development, small business, social services, childcare, banking, government, philanthropy, education, and other organizations. The five roundtables were held in:

- Gering

- McCook

- Nebraska City

- O’Neill

- Wayne

Roundtable participants discussed the following questions:

- What is working to increase economic opportunities in lower income communities?

- What challenges and barriers do you see for lower income communities and households in your region?

- What would increase economic opportunities for lower income communities?

- Where are the gaps? What aren’t we talking about that needs to be part of the larger discussion?

An O’Neill roundtable participant considers where to place his stickers.

At the end of each roundtable discussion, participants had five stickers each to mark the most pressing community development issues and opportunities.

What were the most pressing community development issues and opportunities?

Findings from the key informant interviews and roundtables aligned along the following themes:

- Community capacity

- Early childhood care

- Financial capacity

- Housing

- Immigration

- Small business

- Transportation

- Workforce

An additional theme across all discussions was Nebraska’s aging, lower income population.

This article explores the topics of community capacity, financial capacity, housing, and the interconnections between transportation and workforce. While participants often mentioned small business and immigration, they were not discussed in enough detail to include.

Additionally, the Kansas City Fed has recently explored the issue of early childhood care, and it is reported on separately here._

Participants in the O’Neill roundtable choose their top five community development issues and opportunities.

Findings for each topic include the following:

- Community perspective on challenges;

- Community perspective on opportunities; and

- Community perspectives on impact. This section highlights existing programs and services that respondents feel are making a difference in their community.

The community of Wayne distinguished itself by its pristine blue water tower.

COMMUNITY CAPACITY

How did participants describe their community capacity?

One theme woven through the many conversations was the community’s capacity to address challenges for lower income communities. “Capacity” here refers to people, resource, and system capacity.

People. Rural communities across Nebraska are aging and losing population. According to the External Link6 Regions, One Nebraska initiative, facilitated in part by the Nebraska Department of Economic Development and Nebraska Chamber of Commerce and Industry, between 2010 and 2022 the average population across all counties in Nebraska’s panhandle decreased 7.6%. This lack of people limits capacity for civic engagement in smaller communities. “It’s the same five people doing all of the things,” one community member said.

Resource. We heard many concerns about the stability of funding, both from public and private sources. These concerns affect the ability of community-based organizations to meet the needs of lower-income communities in both rural and urban environments. Participants from nonprofit organizations were concerned about sustaining programs that were funded through pandemic relief funds. Other participants were concerned about shrinking public funding, separate from the cessation of pandemic relief programs.

Additionally, private philanthropy in Nebraska is in transition. Major foundations in Omaha have announced plans to spend down assets and cease funding activities in the next five to 10 years. Also, in rural communities a major transfer of wealth across generations is affecting community giving and philanthropy. According to the Nebraska Community Foundation’s 2021 Transfer of Wealth Study, more than $100 billion in generational wealth is anticipated to transfer over the next decade in Nebraska.

As one participant said, “We need a narrative change in how we collectively fund solutions.”

System. Participants identified challenges that were service level, and challenges that were systems level. We can use housing to illustrate the differences between services- and systems-level work.

Rental assistance for families facing eviction because they can’t pay their rent is an example of a service. This addresses just one part of the housing challenge. A systems-level approach, however, looks across multiple elements of the housing challenge and the many intersections across public and private sectors to create holistic solutions. Housing first policies have been proposed as an example of a systems-level solution. For example, housing first policies prioritize providing shelter for people experiencing homelessness without meeting any prerequisites for service, theorizing that housing stability was necessary to adequately address other challenges. It relies on a coordinated entry system of housing service providers working collaboratively to provide housing opportunities. It is systemic because it addresses the structural problem of how people needing housing supports gain access to that housing, rather than purely focusing on the service of providing housing supports.

Participants in the Gering roundtable consider where to cast their votes.

The dichotomy of systems- and service-level issues, one person said, was a challenge in and of itself. In explaining the many services available, particularly in urban areas, the participant said the state needed an equally significant emphasis on systems: “We are a services rich and systems poor state.” While we heard this feedback, we simultaneously heard from community members in rural areas who said they were challenged to find services.

Community members also reported a lack of program awareness, both from lower income families needing support and from other organizations looking for referral options.

Despite the challenges cited by participants, they saw opportunities to increase community capacity by leveraging regional collaboration and advancing public-private partnerships.

Community capacity: What is having an impact?

When asked what was working to support lower income communities, people often mentioned collaboration using the collective impact model. Collective impact is a specific model of collaboration that requires five conditions:

- Common agenda that collectively defines the problem and creates a shared vision to solve it;

- Shared measurement systems that allow for continuous learning and accountability;

- Separate but mutually reinforcing activities to maximize results;

- Continuous communication to build trust and strengthen relationships; and

- Strong backbone organization aligning the work._

Across the state, there are many examples of collective impact at work.

The Nebraska Children and Families Foundation supports a network of 21 community collaboratives through its Bring Up Nebraska framework._ These collaboratives address the needs of children and families. While they do not explicitly serve lower income households, they almost exclusively do. The system-level response worked, people said, because there was a coordinated entry point for families and a central point within the community that connected families to the resources they needed.

Downtown Norfolk at twilight.

Career Connections of Western Nebraska, housed at Twin Cities Development Association, Inc., is another example of collective impact at work. According to data gathered by the Nebraska Community Foundation, many young Nebraskans wanted to stay in the community where they grew up. Initiatives like Career Connections create a way for that to be possible._

In their own words:

Career Connections of Western Nebraska is a cross-agency leadership team focused on the development of strong, vibrant rural economies. The challenges facing rural workforce, and the systems that support them, are unique and require collaborative and targeted approaches that increase career pathways for rural learners. Based on work with entrepreneurial rural communities across the country, we are convinced that youth are essential to real and lasting economic revitalization._

Career Connections intentionally engages the education, workforce development, economic development, human services, and private sectors to create economic opportunities for youth to stay engaged in their local communities and drive economic growth for Western Nebraska. Through the program, high school students engage with local employers and other community partners to learn about career pathways available in their local communities.

The Gering conversation gathered thoughts about challenges and opportunities.

FINANCIAL CAPACITY

What did Nebraskans say about financial capacity?

Lower income households have fewer financial resources to cover costs, which affects their financial capacity. Many people we talked with said that lower income households struggled to meet day-to-day expenses. “You need food, healthcare, and a place to sleep. People are struggling with all three right now.” Households also struggled to deal with unexpected expenses: “One expense not anticipated comes up, throws people into chaos, and they can’t function. And it can be years before they rebound from that one situation.”

Community members also expressed concerns about access to banking services for lower-income households. While the number of unbanked households in Nebraska has declined from 6.5% in 2019 to 2.5% in 2023,_ community members said it would be helpful if financial institutions would conduct more outreach on products for lower income or “second chance” banking clients.

One participant suggested wealth building needed to be discussed differently. Historically, wealth-building narratives centered around the power of homeownership in creating generational wealth. Rising costs, though, means that younger people are delaying homeownership and its associated wealth-building opportunities. The participant said that collectively, alternative wealth-building vehicles need to be explored in greater detail as tools for disrupting generational poverty. They identified small business ownership and entrepreneurship as potential tools.

Community members also spoke to non-tangible elements of household financial capacity, such as the power of social capital and time. Lower income earners often spend their time, a limited resource, working or on activities that can improve their financial position. One of the largest challenges community members shared was the opportunity cost, or what lower income earners give up, to improve their financial capacity. For example, night classes can lead to a higher-paying job, but the opportunity cost includes a loss of wages due to fewer hours available for work.

Each participant had five votes to cast for the ideas they felt were most important.

Similarly, lower income individuals can face barriers to program participation, both structurally and because of limited personal resources. If the student works during the day and takes classes at night, they face a structural barrier. Childcare centers generally do not provide evening hours, so that student would need to use their social network to fill that gap. Without access to a social network, options for childcare become even more limited. This scenario is just one example of the various demands on time and social capital and its potential impact on lower income individuals.

Financial capacity - What is having an impact?

Small-dollar lending programs have the power to be transformative in the lives of lower income households. They can provide funds to overcome financial barriers and provide an alternative to predatory lending products. We heard about three small-dollar lending programs offered by nonprofit organizations across the state:

- Friendship Home worked with a local bank to create a small-dollar lending program, recognizing the need for additional financial services for individuals seeking safety from domestic and intimate partner violence.

- Lending Link provides small-dollar loans as an alternative to high-cost payday loans. The organization also provides clients with financial coaching.

- Nebraska Children and Families Foundation also operates a small-dollar revolving loan program for young people with previous engagement with the juvenile justice or child protective systems to help them avoid predatory lending products.

A colorful mural caught Surmick’s eye in Hastings, Nebraska.

Another bright spot was individual development accounts, or IDAs. IDAs are a form of savings that provide a percentage match for every dollar saved, dependent on program design. Frequently, these programs are used to help lower income households save for things like a car, education, or small business activity. In addition to the revolving loan fund, Nebraska Children and Families Foundation also operates an IDA for the youth in their program to help them access education, housing, reliable transportation, or to launch a small business. In 2023, 900 program participants saved more than $400,000 before the match. Community Action Partnership of Lancaster and Saunders Counties offers Free to Save – Asset Saving and Purchase, a program that combines financial coaching with a four-to-one matched savings account. Through the program, participants can contribute up to $2,000 to be matched with $8,000, providing a total of $10,000. Funds can then be applied towards a vehicle, post-secondary education, or small business start-up or expansion.

HOUSING

What did Nebraskans say about housing?

Affordable housing is a challenge everywhere, we heard from people in communities across the state. To learn more about the scope of housing challenges in Nebraska, there are a myriad of reports available, such as:

- External LinkNebraska Investment Finance Authority’s Strategic Housing Framework

- External LinkOmaha’s Housing Affordability Action Plan

- External LinkLincoln’s Affordable Housing Coordinated Action Plan

People consistently talked about the persistent challenges with housing affordability, both homeownership and rental, as well as the challenges facing increasing inventory through new construction. A few people also mentioned home repair as a housing challenge. In Nebraska, 60% of housing stock was constructed before 1980.

Participants, particularly those in rural communities, also reported concerns about vacant housing. Vacant housing presents multiple challenges. Deteriorating vacant housing creates blight in a community. When it goes unaddressed for a significant period, the opportunity for home rehabilitation becomes more challenging. This can result in the need to demolish property, increasing reliance on costlier new construction to fill the housing gap.

Housing – What is having an impact?

Nebraska has a variety of programs that work to address housing quality issues.

- NeighborWorks Northeast Nebraska and NeighborWorks Lincoln both operate homeownership programs that provide housing rehabilitation funds for LMI homebuyers.

- Rebuilding Together Platte Valley East offers a home repair program for lower income homeowners.

Habitat for Humanity Omaha provides education and outreach to help homeowners execute transfer-on-death deeds to prevent heirs’ property challenges for lower income households in Omaha and Bellevue.

Nebraska communities celebrate their history.

TRANSPORTATION + WORKFORCE

What did Nebraskans say about the connection between transportation + workforce?

Access to reliable transportation is a critical factor in workforce participation, particularly for lower-income residents. Lack of transportation creates significant barriers to employment and economic mobility. People we talked to shared challenges, including:

Lack of a reliable personal vehicle: Without their own transportation, people find it hard to commute to jobs, especially those located far from urban centers. Without a car, individuals often rely on public transit, which may not be sufficient or convenient.

Poor public transit: Public transit systems in many areas are inadequate or non-existent. This is particularly true in suburban and rural areas where job growth is occurring. Insufficient public transit options make it hard for lower-income workers to reach their job sites, leading to higher rates of joblessness and underemployment.

Driver’s license testing offered only in English: We heard from a handful of communities with larger immigrant populations that driver’s license tests are administered only in English. This presents a significant barrier for residents for whom English is a second language.

New job opportunities on the fringe of the metro: New job opportunities often develop on the outskirts of metropolitan areas, a phenomenon known as job sprawl. Employees must travel longer distances to reach these positions. Individuals who rely on public transportation may find this time-consuming and costly. For example, someone living in North Omaha and working in Elkhorn (western Omaha), a place of current growth and development, would have no way to get there via public transit alone. Someone commuting via public transit from central Lincoln to one of the many manufacturing plants in the northwest part of the city could spend an hour and a half on that commute, in one direction.

Omaha’s Metro launched Metro Flex, a microtransit pilot program supported by local foundations.

Transportation + workforce – What is having an impact?

Some Nebraska communities are working to create transportation solutions. Earlier this year, Omaha’s Metro announced the launch of a Metro Flex program, a microtransit pilot program supported by local foundations. The program provides transportation in three “Metro Flex Zones,” areas of the city without existing public transportation routes.

Conclusion

This report explores four challenges affecting lower income communities, but the strengths in the system also bear mentioning.

We started each roundtable discussion asking the question: “What is already working to support lower income communities in your region?” While some discussions started off slower than others, all five groups had no trouble filling up multiple pages of an easel pad with the strengths they saw in their respective communities.

We saw a variety of answers to this question, including affordable housing investments, small businesses investments, and the role specific organizations and programs play in supporting households. One theme mentioned in interviews and roundtables throughout Nebraska was different, though. It wasn’t about tactics or funding. It was about people, and how they work together. Consistently, people told us that a strength was the power of collaboration and the ability of Nebraska communities to harness that power to benefit lower income people.

If you want to continue the conversation on how you see these issues affecting communities across Nebraska, we would be happy to hear from you. Contact Rachael Surmick at Rachael.surmick@kc.frb.org.

Endnotes

-

1 American Community Survey, 2023 Act 1-Year Estimates, Table S1702

-

2 Bureau of Labor Statistics, May 2023 State Occupational Employment and Wage Estimates.

-

3 For more information about asset-based community development visit the Asset-Based Community Development Institute housed at DePaul University: www.abcdinstitute.org

-

4 See External Linkhttps://www.kansascityfed.org/research/economic-bulletin/cost-of-childcare-increasingly-weighs-on-labor-force-engagement/ and External Linkhttps://www.kansascityfed.org/ten/costs-putting-quality-affordable-childcare-out-of-reach-for-many/

-

5 Kania, John, and Mark Kramer. “Collective Impact.” Stanford Social Innovation Review 9, no. 1 (2011): 36–41. External Linkhttps://doi.org/10.48558/5900-KN19.

-

6 For more information about Bring Up Nebraska and to find a local group, visit External Linkhttps://bringupnebraska.org/.

-

7 External Linkhttps://www.nebcommfound.org/wp-content/uploads/2023/08/2023-Youth-Survey-REPORT-1.pdf

-

8 External Linkhttps://www.tcdne.org/workforce/career-connections

-

9 2023 FDIC National Survey of Unbanked and Underbanked Households

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author