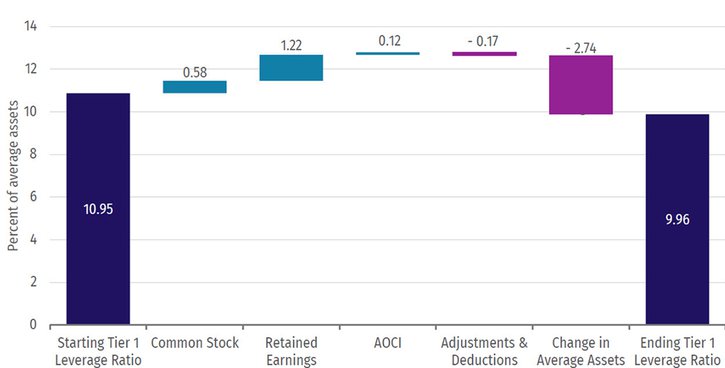

Change in Tier 1 Leverage Ratio

From Q4 2019 to Q2 2021

Note: AOCI is accumulated other comprehensive income.

Source: Bank Call Reports

- Community bank_ balance sheets have expanded considerably during the COVID-19 pandemic. Since year-end 2019, community banks have absorbed over $560 billion in deposits and increased their loan portfolios by $226 billion. In total, assets have increased 27.4 percent, with Paycheck Protection Program (PPP) loans that remain on the books accounting for nearly one-fifth of the total growth. The remaining asset growth is primarily driven by an increase in cash and securities.

- The substantial asset growth experienced by community banks has placed downward pressure on capital ratios. The aggregate tier 1 leverage ratio declined from 10.95 percent as of year-end 2019 to 9.96 percent as of Q2 2021. While banks have augmented capital through retained earnings, it has not been sufficient to fully offset the negative impact from asset growth.

- Bank balance sheets remain inflated as a deposit levels remain elevated, and it is uncertain if or when those balances will decline. Further, PPP loan forgiveness has not resulted in balance sheet contraction as payoffs for these loans are primarily being deployed into lower yielding highly liquid instruments.

Questions or comments? Please contact KC.SRM.SRA.CommunityBankingBulletin@kc.frb.org.

Endnotes

-

1 Community banking organizations are defined as having $10 billion or less in total assets as of year-end 2019.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.