Reduced profits in the crop sector persisted in the fourth quarter of 2014, leading to a sharp rise in farm-sector borrowing and a slight decline in cropland values. A near-record fall harvest pushed crop prices to their lowest levels in five years, eroding profit margins and prompting a rise in loan volumes to finance short-term operating expenses. Farmland markets also cooled amid prospects of lower farm income, particularly in heavy crop-production areas. Should low crop prices and high input costs persist, crop sector profit margins may weaken further and strain loan repayment capacity in the coming year.

Chart 10: Rate of Return on Assets, Third Quarter

Chart 11: Delinquency Rates on Farm Loans

Map: Value of Nonirrigated Cropland, Third Quarter 2014

Chart 12: Agricultural Credit Conditions, Third Quarter 2014

Chart 1: Non-Real Estate Farm Loan Volumes by Purpose

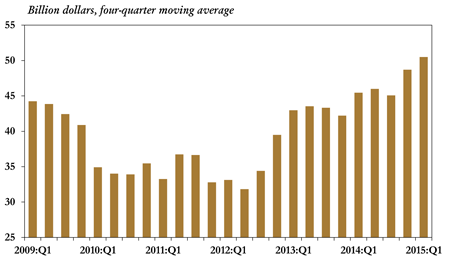

Chart 2: Current Operating Loan Volume

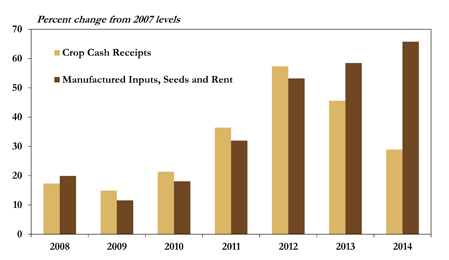

Chart 3: U.S. Crop Cash Receipts and Input Costs

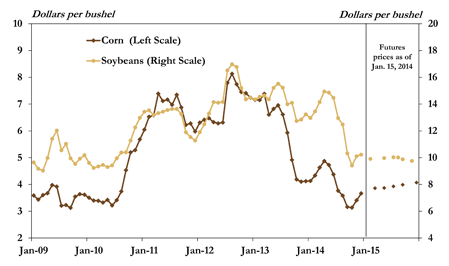

Chart 4: U.S. Corn and Soybean Prices

Chart 5: Livestock Loan Volume and Feeder Cattle Price

Chart 6: U.S. Calf Slaughter Federally Inspected, Weekly

Chart 7: Annual Farm Machinery and Equipment Loan Volume

Chart 8: U.S. Combine and Four-Wheel Drive Tractor Sales

Conclusion

Tighter profit margins for crop producers drove increased lending to the agricultural sector for production loans but trimmed farm capital spending and demand for equipment loans in 2014. Agricultural bankers reported sufficient funds were available to satisfy a rise in loan demand but also noted some deterioration in loan repayment rates and indicated collateral requirements had tightened slightly. After narrowing in 2014, the direction of farm sector profit margins in 2015 will be a key factor in determining whether agricultural credit conditions improve or worsen in the coming year.

Improved farm sector loan performance supported a slight rise in profits at agricultural banks. At the end of the third quarter, the return on assets at banks with an above-average percent of loans made to the agricultural sector edged up from year-ago levels (Chart 10). Delinquency rates on both farm real estate and non-real estate loans moved lower and net-charge offs as a share of total loans also declined (Chart 11). In addition, the average capital ratio at agricultural banks improved from last quarter and last year.

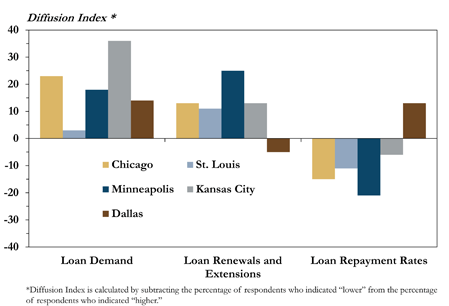

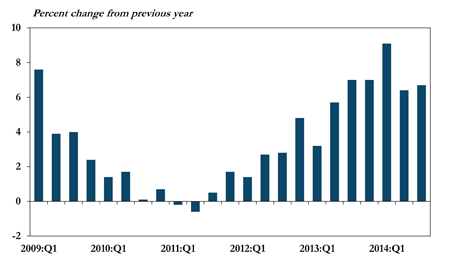

Agricultural bankers reported only a modest deterioration in credit conditions despite a drop in farm income in the third quarter of 2014. Reduced profitability for crop producers in the Chicago, St. Louis, Minneapolis, and Kansas City Districts was driving increased demand for operating loans and a decline in loan repayment rates as well as more requests for loan renewals and extensions (Chart 12). Still, survey respondents in all reporting Federal Reserve Districts indicated funds were available for farm loans but noted a slight rise in collateral requirements.

Commenting on the livestock sector, Dallas survey respondents reported initial signs of herd rebuilding but noted that current low inventories were keeping cattle prices high and boosting demand for feeder cattle loans. However, easing drought conditions and profitability in the cattle sector bolstered loan repayment rates in the Dallas District and lessened the need for loan renewals and extensions.

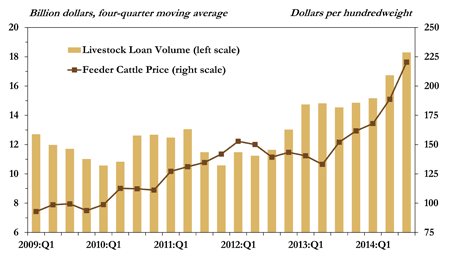

In contrast, profitability in the livestock sector improved markedly in 2014 as cattle and hog prices strengthened and producers paid lower feed costs. Low cow inventories due to several years of herd liquidations continued to push feeder cattle prices to new highs, lifting profits for cow/calf producers but increasing costs for feedlot operators. Lending to the livestock sector rose significantly in 2014, primarily due to a jump in feeder livestock loans (Chart 5). Looking ahead, the supply of feeder cattle may contract further if a reduction in calf slaughter signals that more animals are being retained to rebuild herds (Chart 6).

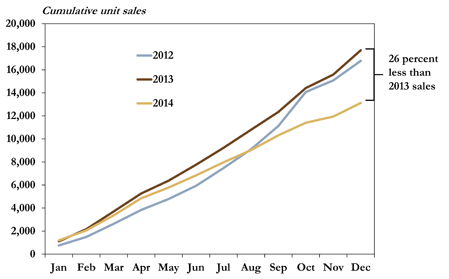

As short-term borrowing in the farm sector ramped up, intermediate-term loan volumes for farm equipment purchases fell further (Chart 7). Demand for farm equipment weakened as prospects of a record crop, and lower prices, appeared more certain heading into harvest. According to the Association of Equipment Manufacturers, 2014 combine and four-wheel drive tractor sales in the U.S. began on par with 2013 levels but slowed steadily and ended the year down 26 percent (Chart 8). Although the existing Section 179 tax incentives for the purchase of machinery and equipment were reinstated the last week of December, the reinstatement seemed too late to significantly boost 2014 sales.

Chart 9: Farm Debt Outstanding at Commercial Banks

Section A - Fourth Quarter National Farm Loan Data

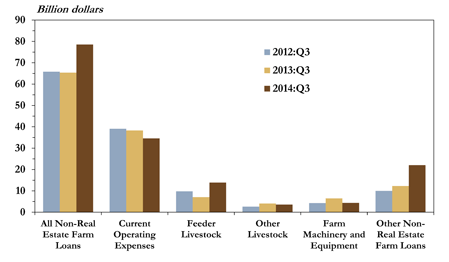

Agricultural lending escalated in the fourth quarter amid lower profits in the crop sector. According to the national Survey of Terms of Bank Lending to Farmers, conducted during the first full week of November, the total volume of non-real estate farm loans rose significantly compared with the same period in 2013 (Chart 1). Most of the gains were driven by increased borrowing for current operating expenses (Chart 2). In 2014, a large U.S. corn and soybean harvest placed downward pressure on prices and limited cash receipts for fall crop sales (Chart 3). With production expenses holding at high levels, reduced farm income increased the need for financing to pay for next year’s crop inputs. Despite a slight rebound in crop prices from the October low, corn and soybean prices have remained significantly below those of recent years (Chart 4).

Section B - Third Quarter Call Report Data

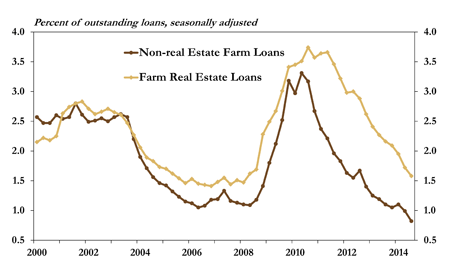

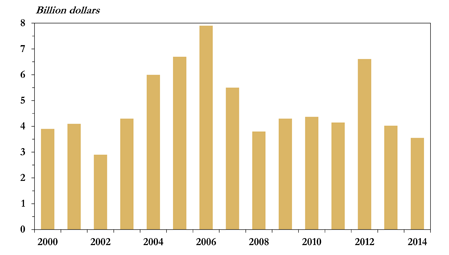

Farm lending at commercial banks remained well above year-ago levels in the third quarter and bank profits edged higher. Commercial bank call report data showed farm debt outstanding at commercial banks was 6.7 percent higher than the previous year, as of Sept. 30 (Chart 9). Loan growth was driven by a 6.9 percent annual increase in the volume of loans secured by farm real estate and a 6.6 percent annual increase in the volume of loans to finance agricultural production. Increased lending pushed loan-to-deposit ratios at agricultural banks to their highest levels since 2010.

Section C - Third Quarter Regional Agricultural Data

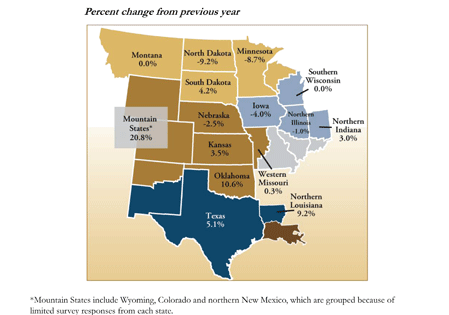

According to Federal Reserve surveys, reduced profitability in the crop sector has been accompanied by a slowdown in cropland price appreciation or even a slight reduction in values, particularly in the Corn Belt. Agricultural bankers reported that nonirrigated cropland values have edged down from recent peaks in several states while year-over-year value gains have moderated in others (Map). Ranchland values, however, continued to rise with strong demand for high-quality pasture. While the majority of survey respondents expected cropland values would stabilize, some anticipated additional declines in 2015.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author