The outlook for agriculture remains downbeat but is beginning to show signs of stabilization. Despite aggregate measures of farm income being significantly lower than in previous years, the farm income forecast for 2017 was relatively unchanged from the 2016 estimate. Although farm income was expected to stabilize, growing inventories and trade uncertainty remain key risks to the outlook. High yields boosted production of corn and soybeans to near-record levels for the fourth year in a row. Greater production was expected to boost inventories and hold prices at lower levels. Alongside growing domestic supplies, demand from exports and international trade have become more important, but agricultural producers and bankers have expressed concerns over increasing foreign competition and uncertainty surrounding trade deals, such as NAFTA. In the cattle sector, price variability is a primary concern, but despite larger inventories, prices and net margins are above year-ago levels.

Farm Income and the Outlook for Agriculture

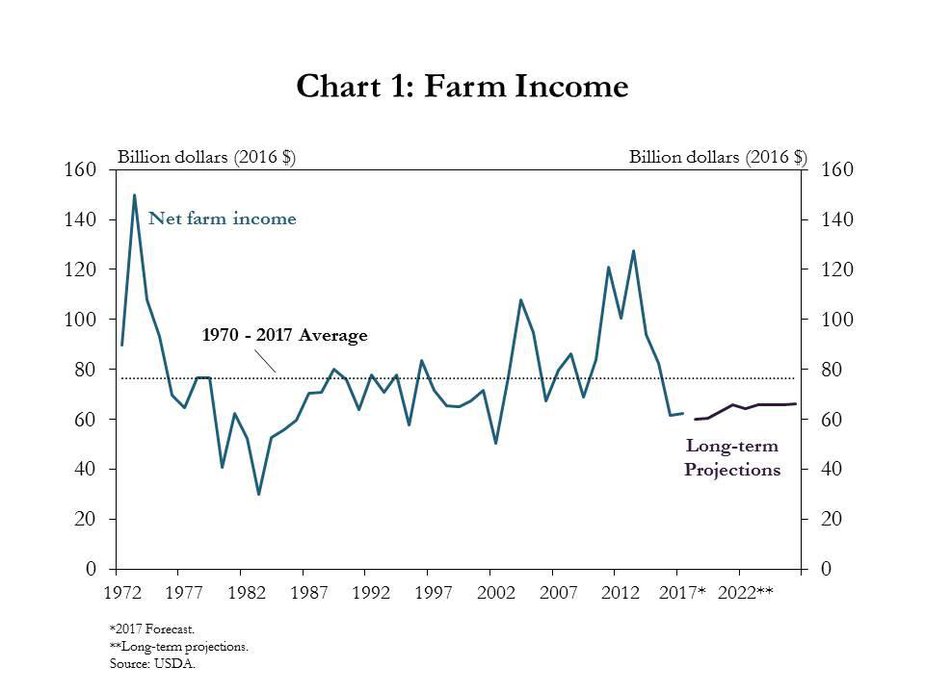

Following steep declines for three consecutive years, farm income was expected to stabilize in 2017 and beyond. In inflation-adjusted dollars, real net farm income was forecast to be relatively unchanged from 2016 (Chart 1). In nominal terms, farm income was forecast to increase about 3 percent from 2016. Forecasts for stable farm income were led by expectations that increasing revenues for livestock and livestock products would offset declining revenues in the crop sector. However, despite the forecast for stable farm income relative to 2016, levels for 2017 still were expected to be 18 percent lower than the long-run average. Longer-term projections for farm income were also expected to stabilize but at levels below the long-run average from 1970 to 2017.

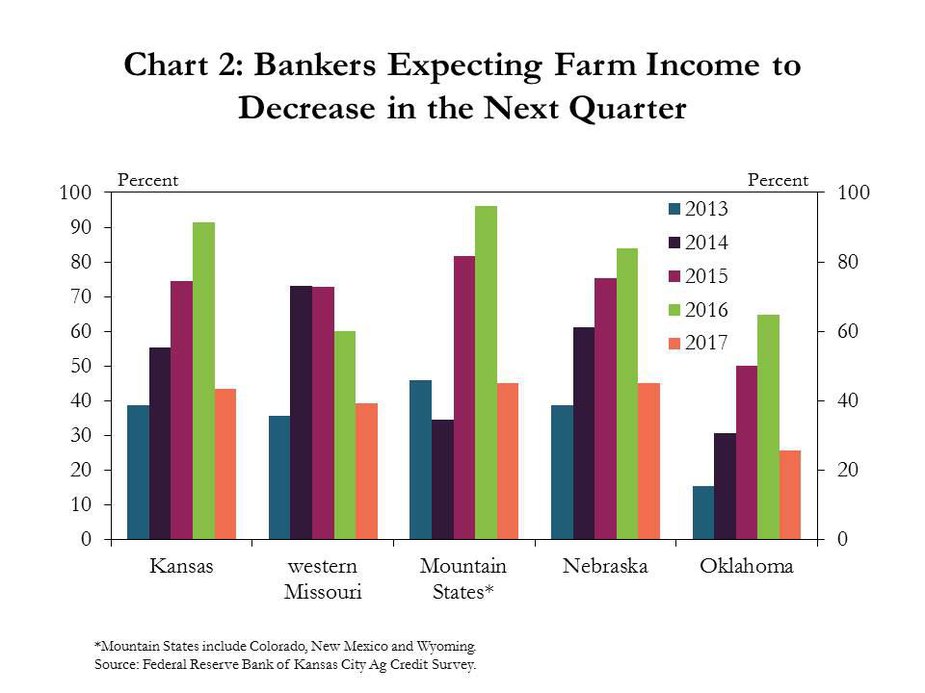

Alongside forecasts of relatively stable farm income for 2017, bankers’ expectations of future declines in farm income have moderated throughout the Tenth District. The third quarter Tenth District Survey of Agricultural Credit Conditions indicates the share of bankers expecting further declines in income in the fourth quarter of 2017 was smaller than a year ago in each state (Chart 2). From 2014 to 2016, an increasing number of bankers in Kansas, the Mountain States, Nebraska and Oklahoma expected farm income to be lower in the next quarter. This trend reversed in 2017. Whereas a majority of bankers expected lower farm income in 2016, less than half of bankers in each state had the same expectations in 2017. In western Missouri, a region where crop production has been very strong in recent years, the share of bankers expecting lower farm income decreased for a third straight year.

Key Risks to the Outlook

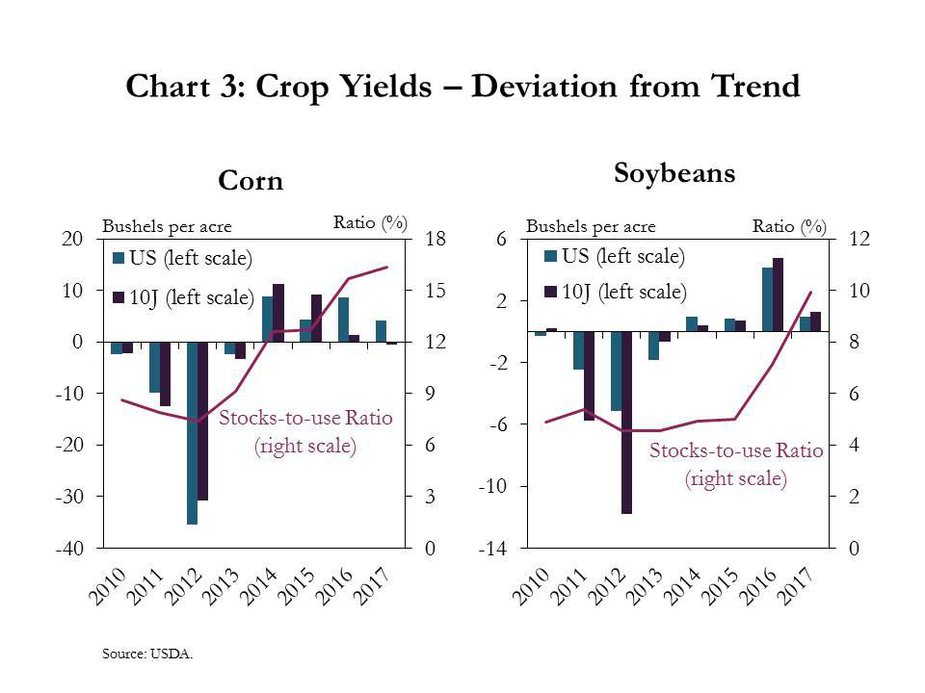

Although farm income appears to have stabilized in the short to longer term, one risk to the outlook has been growing supplies. Yields for corn and soybeans have been above 20-year trend levels since 2014 and have contributed to increasing inventories (Chart 3). In 2017, corn yields in the Tenth District were slightly below trend, likely due to reports of moderate to severe wind damage, but in the United States, higher yields have contributed to significant increases in inventories, measured as stocks-to-use ratios. In addition, soybean inventories have doubled since 2015. Growth in U.S. corn and soybean inventories is a risk to the outlook because larger inventories have been linked to lower prices.

As growth in domestic production has continued to outpace domestic use, U.S. agriculture has become increasingly reliant on exports. The USDA recently reported that exports are responsible for 20 percent of farm income. Therefore, although international demand has provided some opportunities for the agricultural sector, uncertainty surrounding trade remains a risk to the outlook.

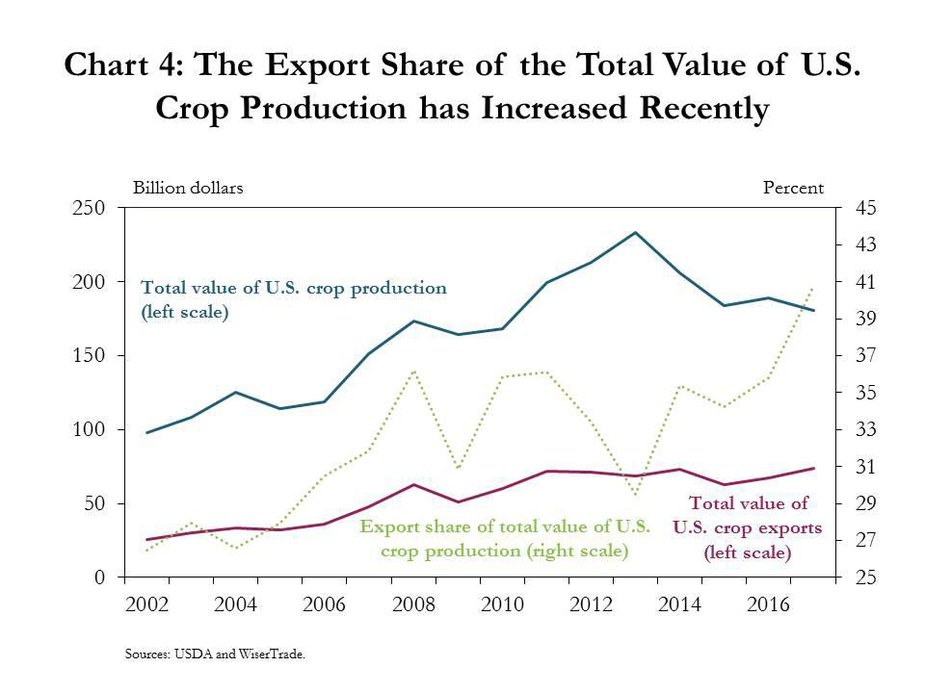

One reason trade is a risk to the outlook is because exports in recent years have contributed a larger share of the total value of U.S. crop production. The total value of crop production has declined since 2013 (Chart 4). At the same time, the total value of crop exports has increased slightly. Over the last four years, the export share of the total value of U.S. crop production increased from 29 percent in 2013 to an estimated 40 percent in 2017. This seems to indicate that demand from international markets has provided some support for the U.S. agricultural sector during the recent downturn.

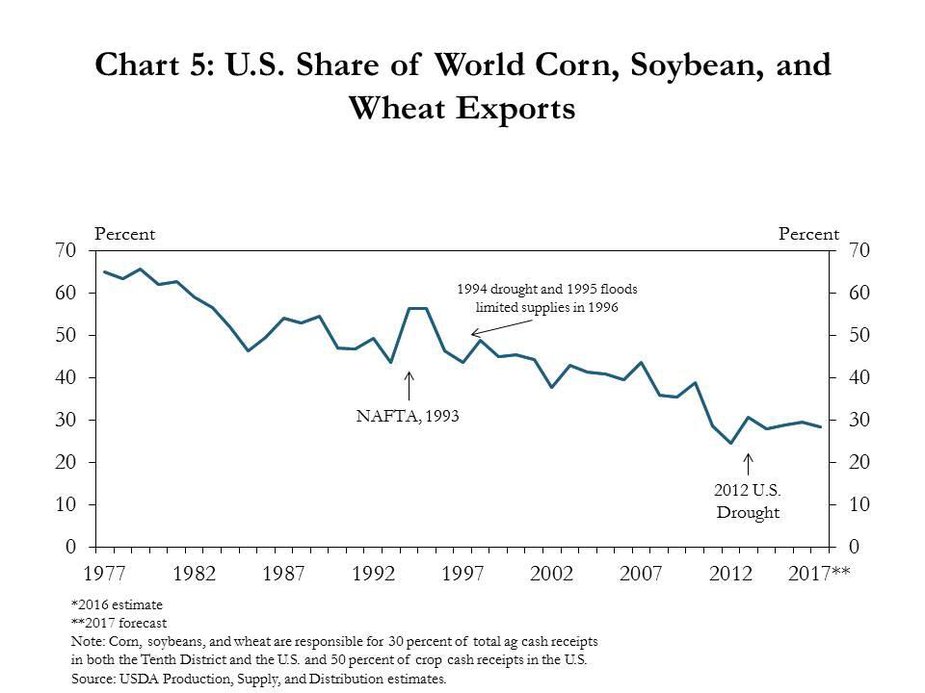

However, the U.S. share of world crop exports has fallen steadily over time. In the late 1970s, the U.S. held a 65-percent share of world crop exports (Chart 5). In 2017, the U.S. share of world crop exports was forecast to be 28 percent. The decline in the U.S. share of world crop exports suggests that the rest of the world has become more active in global export markets when the U.S. has become increasingly reliant on world trade.

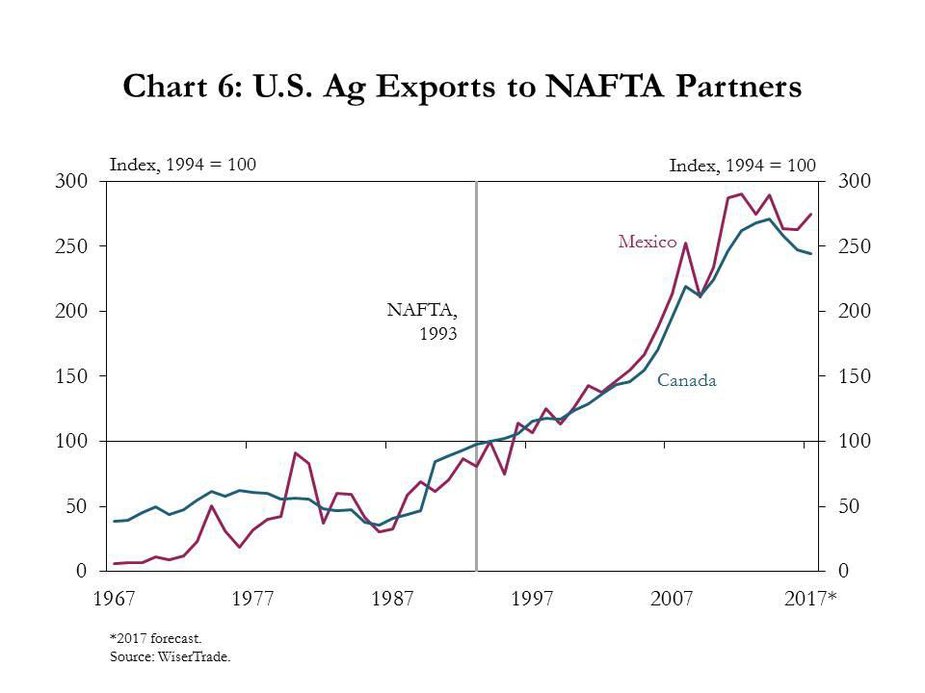

One mitigating factor of increasing global competition has been trade deals, such as the North American Free Trade Agreement (NAFTA). Agricultural exports to both Canada and Mexico dramatically increased following the implementation of NAFTA in 1993 (Chart 6). In fact, the value of agricultural exports to both NAFTA partners more than doubled following the implementation of NAFTA. It is unclear what would happen if the United States fails to renegotiate NAFTA. However, because the United States has become more reliant on international demand for agricultural products and international competition for agricultural exports has increased, uncertainty surrounding NAFTA and other trade deals is a key risk to the agricultural outlook.

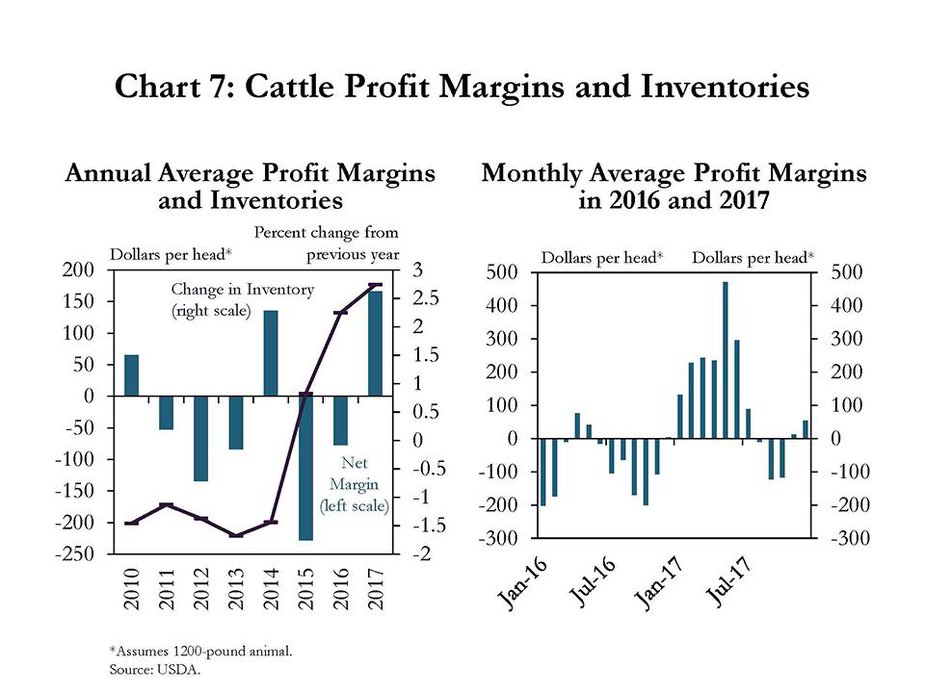

Beyond risks related to crops and trade, recent developments in the cattle sector also present risks to the outlook. The cattle sector is a key industry to the Tenth District agricultural economy, contributing more than 50 percent of the District’s total agricultural revenues. As mentioned previously, cattle profit margins have supported aggregate measures of farm income and are expected to be positive in 2017, following negative profit margins in 2015 and 2016 (Chart 7, left panel). Higher prices and positive profit margins have occurred alongside increasing inventories. However, the pace of inventory expansion has slowed; cattle slaughter weights have come down slightly and demand for beef has picked up, both domestically and internationally.

Despite higher (annual average) profit margins in 2017, risks to the cattle outlook still persist. Larger inventories have begun to weigh on prices in the second half of 2017. Although average profit margins are positive for the year, monthly-average profit margins have been negative to just over break-even since August (Chart 7, right panel).

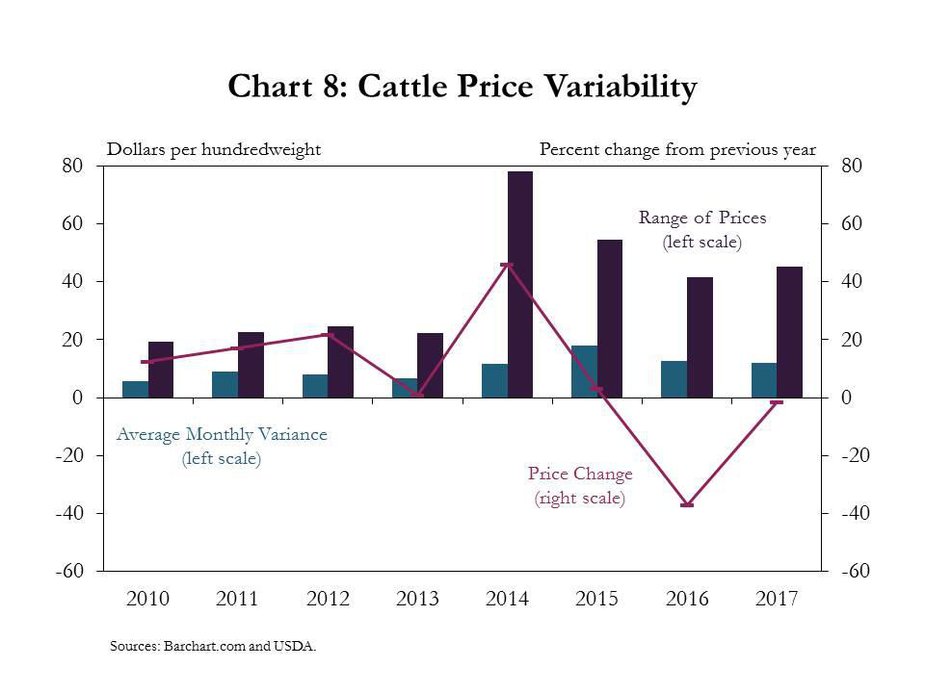

In addition to lower prices and negative profit margins in the second half of 2017, one concern for ranchers has been the increasing variability of cattle prices. Since 2014, cattle prices have become much more variable (Chart 8). From January to November, the average monthly variance and the range of prices paid increased significantly from previous levels. In 2014, the larger range was due to a steady increase in prices from January to November. However, during the last three years, increasing price variability in a period of lower prices has contributed to added concern and uncertainty in the outlook for cattle producers.

Conclusion

In conclusion, although expectations for farm income have stabilized, the stabilization has occurred at much lower levels than in previous years. Continued oversupply of agricultural products, especially crops, is a significant risk and would likely keep prices from rising to more profitable levels. International trade could help support agricultural prices and incomes, but uncertainty over trade deals has generated additional risk for the agricultural sector. In the first half of 2017, strength in the livestock sector supported U.S. farm income, but increasing cattle inventories and greater price variability suggest that the outlook could remain weak.

References

USDA Farm Income Team. 2017. 2017 Farm Sector Income Forecast. USDA Farm Sector Income & Finances Report, Nov. 29. Available at External Linkhttps://www.ers.usda.gov/topics/farm-economy/farm-sector-income-finances/farm-sector-income-forecast/.

U.S. Department of Agriculture (USDA) Office of the Chief Economist and World Agricultural Outlook Board. 2017. USDA Agricultural Projections to 2026. Prepared by the Interagency Agricultural Projections Committee. Long-term Projections Report OCE-2017-1, 106 pp. Available at: https://www.ers.usda.gov/topics/farm-economy/agricultural-baseline/