Business Activity Grew at a Moderate Pace

Tenth District services activity growth continued at a moderate pace, and activity was expected to increase at a modest rate over the next six months (Chart 1 & Table 1). Indexes for input and selling prices increased to surpass the survey record highs set in recent months. Input and selling prices were also higher than a year ago for most firms and were expected to expand more over the next six months, especially input prices.

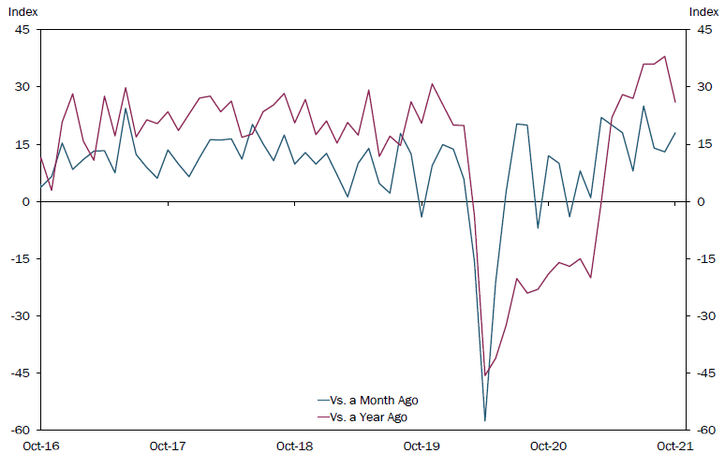

The month-over-month services composite index was 18 in October, up moderately from 13 in September and 14 in August (Tables 1 & 2). The composite index is a weighted average of the revenue/sales, employment, and inventory indexes. The increase in revenue and sales was driven by an uptick in wholesale, retail, real estate, and professional and high-tech business activity. On the other hand, auto and tourism activity declined. Most month-over-month indexes remained positive in October, indicating expansion. Sales and employment rose at a faster pace, while inventories declined slightly from a month ago. Wages and benefits and capital expenditures remained high for many firms. The year-over-year composite index eased slightly from 38 to 26 but remained positive. Compared to a year ago, sales were solid and capital expenditures increased while inventory levels continued to decrease. Future services activity was expected to increase at a modest pace with a future composite index of 22.

Chart 1. Services Composite Indexes

Special Questions

This month contacts were asked special questions about supply chain disruptions. In October, 80% of business services contacts reported facing challenges with supply chain disruptions and shortages, up from 76% in July 2021. More firms reported raising prices and turning away business in October than in July (Chart 2). Around 37% of firms reported delaying projects, increasing inventories, and diversifying suppliers, and a higher share of firms also reported making capital or technological investments in response to supply chain issues. Moving forward, 44% of firms expected rising materials prices and lack of availability/delivery times to persist for 6 to 12 months, and 43% of firms expected these issues to persist for more than 12 months (Chart 3). Only 13% of firms expected materials price increases and supply chain issues to be resolved within the next six months.

Selected Services Comments

“From what we hear from our vendors the shortages just in America will last at least 6 months. The imports from Italy we get could be up to a year.”

“The largest supply chain issues relate to international imports from Asia. The lead times have gone from 90-days to 150-days from order to receipt. This is straining our balance sheet and balance of payments since most inventory needs to be paid for when it gets on the boat.”

“We are offering rental machinery in place of purchase machinery.”

“We are having problems with construction companies sourcing materials for capital projects.”

“Semiconductor shortages for vehicles not only reduce sales now, but will impact used vehicle supplies for the next two years.”

“The labor shortage in the commercial vehicle driver, retail worker, and restaurant spaces is dire. We have increased freight rates (in addition to the fuel surcharge increases) to offset the increase in driver wages.”

“Beg, borrowing and stealing anything we can get to make food for our guests.”

“We have delayed closings on residential homes until complete [due to supply chain disruptions and shortages].”

“Increased fuel prices are passed directly to our customers through a fuel surcharge.”

“We can only pass on a small percentage of the inflationary increase in inventory, parts, labor and utility costs to the consumer without pricing ourselves out of the market.”

“Absorbing delivery cost increases right now to keep customer base until we get inventory in stock.”

“Fuel up 40% is impacting [profit] margin not price. We would move price if our contracts allowed this.”

Survey Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author