LMI Economic Conditions provides a detailed assessment of economic conditions in low- and moderate-income (LMI) communities, and each issue also provides insights into a special topic relevant to the LMI population. Much of the data used in the report come from a survey administered in the Tenth District, along with comments from that survey. Survey correspondents are people who work in organizations that engage directly with the LMI population on a regular basis.1 In some areas of the report, national data are used and national conditions are considered. The Tenth District encompasses Colorado, Kansas, the western third of Missouri, Nebraska, the northern half of New Mexico, Oklahoma and Wyoming. The Tenth District accounts for roughly 5.8 percent of the U.S. population. A person, household, or community is LMI if income is below 80 percent of area median income. For urban areas, area median income is metropolitan area median income. For non-metro areas, area median income is state median income.

I. Economic Update for LMI Communities

This issue of LMI Economic Conditions emphasizes changes in the general perception of economic conditions and improving labor market conditions. Section I-A examines general perceptions of economic conditions in LMI communities and the demand for services from community organizations in the Tenth District. Section I-B focuses on labor market conditions and job availability. Sections 1-C and 1-D focus on affordable housing and access to credit, respectively. Section II focuses on this issue’s special topic, which is federal housing assistance during the federal government shutdown.

I-A. General Assessment

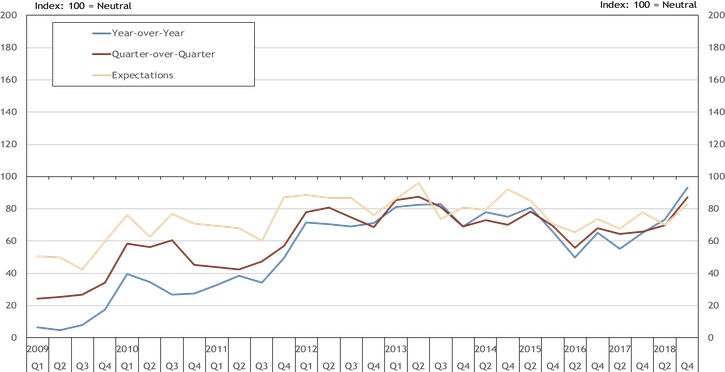

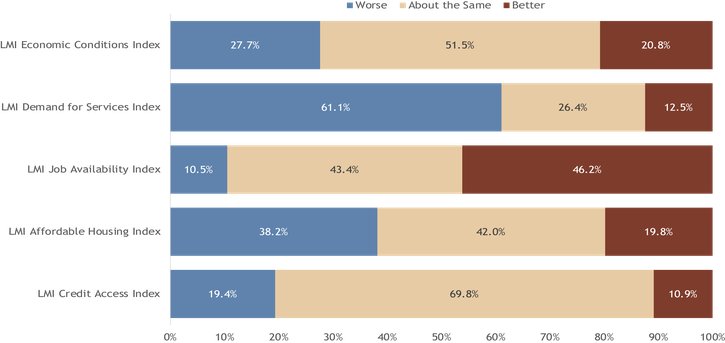

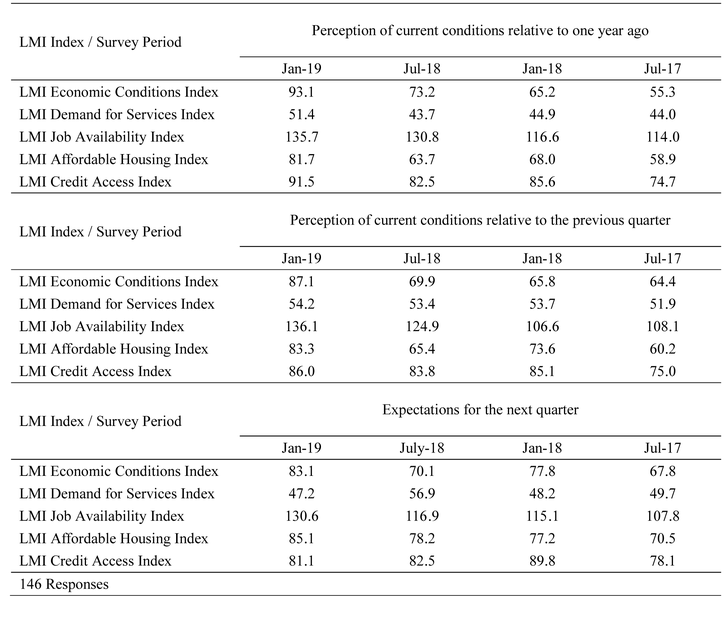

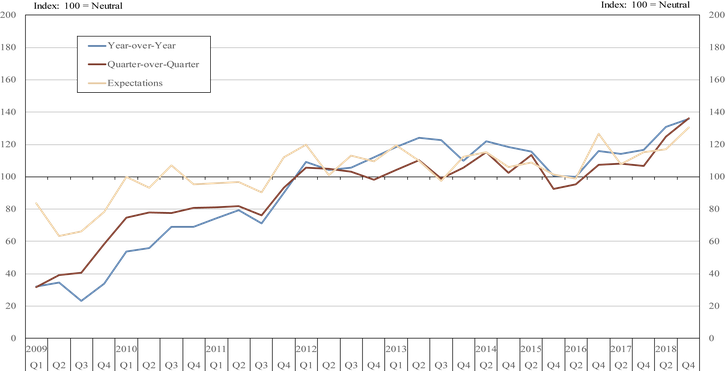

Indicators of economic and financial conditions in the LMI community suggest that they may be stabilizing after a decade of sluggishness. The LMI Economic Conditions Index, the broadest measure of economic conditions in the LMI community, surged to 93.1 in the January 2019 survey (January survey) from 73.2 in the July 2018 survey (July survey), approaching neutral for the first time since the survey began in the first quarter of 2009 (Chart 1).2 An index of 93.1 indicates the balance of opinion is that economic conditions in LMI communities are nearly the same as a year ago. The neutral value is 100, and the index ranges from 0 to 200 (see box). In the January survey, 20.8 percent of respondents reported that overall economic conditions had improved compared with the same period a year ago, and 51.5 percent reported economic conditions were about the same (Chart 2). Still, 27.7 percent reported conditions had worsened.

Chart 1. LMI Economic Conditions Index

Source: Federal Reserve Bank of Kansas City LMI Survey.

Note: The survey asks respondents to assess conditions relative to the same period in the previous year, conditions relative to the previous quarter and for their expectations for the following quarter relative to the current quarter.

Diffusion Indexes

Survey participants respond to each survey question by indicating whether conditions during the current quarter were higher (better) than, lower (worse) than or about the same as in the previous quarter or year. Providers also are asked what they expect conditions to be in the next quarter. Diffusion indexes are computed by subtracting the percentage of survey participants that responded lower (worse) from the percentage that responded higher (better) and adding 100. The exception is the LMI Demand for Services Index, which is computed by subtracting the percentage of survey participants that responded higher from the percentage that responded lower and adding 100 so that higher needs translate into lower numbers for the index. A reading less than 100 indicates the overall assessment of respondents (balance of opinion) is that conditions are worsening. For example, an increase in the index from 70 to 85 would indicate conditions are still deteriorating, by consensus, but that fewer respondents are reporting worsening conditions. Any value more than 100 indicates improving conditions, even if the index has fallen from the previous quarter or year. A value of 100 is neutral.

Chart 2: LMI Survey Responses

Source: Federal Reserve Bank of Kansas City LMI Survey.

Notes: The questions ask if conditions in the category have become worse, about the same, or better than at the same time in the previous year. In some questions, the specific wording asks if some condition is down, about the same, or up.

Other indicators of economic and financial conditions in the LMI community all were higher in the January survey. The LMI Job Availability Index continued its climb well above neutral, while the LMI Credit Access Index also improved significantly to a value much closer to neutral. Finally, the LMI Affordable Housing Index, which had been trending downward since 2013, saw a noteworthy bounce upward. On the other hand, while it improved, the LMI Demand for Services Index remained consistently low, indicating that the demand for services from organizations assisting the LMI population had increased for most survey respondents.3 Values for all indexes are shown in Table 1.

Table 1. Diffusion Indexes for Low- And Moderate-Income Survey Responses

Source: Federal Reserve Bank of Kansas City LMI Survey

Notes: The diffusion indexes (see box), were computed from responses to the Federal Reserve Bank of Kansas City’s biannual LMI Survey, conducted in January 2019. The survey asks respondents about conditions relative to the previous quarter and year as well as expectations for the next quarter.

Comments from the Kansas City survey generally were upbeat compared with past LMI Surveys. Some who reported improving conditions attributed their more optimistic outlook to increased wages—both minimum and market wages. Others reported lower costs for gasoline. Transportation takes up a disproportionate share of budgets for LMI households. But while the LMI Economic Conditions Index moved closer to neutral, moderately more survey contacts still reported worsening conditions than improving conditions, and those who reported no change were in some sense comparing current conditions with a low base. That is, index values have been well below neutral for an extended time, and values below neutral indicate a balance of opinion that economic conditions are worsening. A significant period of deterioration presumably would result in poor economic conditions as a base. Indeed, even though economic conditions may be stabilizing in LMI communities, some survey comments argue that the LMI community has been left behind in the long U.S. economic recovery.

Those with more negative views of economic conditions in LMI communities stressed that although incomes are increasing, they are not keeping up with increases in rents and health-care costs. Nationally, less than 75 percent of those younger than 65 with incomes less than $25,000 have health insurance coverage, compared with about 95 percent of those with incomes greater than $50,000.4 Inflation in health-care costs and rents (especially multifamily) have far exceeded overall inflation over the past 10 years.5

Some respondents indicated political uncertainties have created a negative pall over many in the community development sector. Moreover, the survey was conducted between January 7 and January 18, during a partial shutdown of the federal government.

The approximately neutral but slightly negative view of economic conditions in LMI communities is fairly consistent with the overall view of Americans of the national economy, according to some recent polls. A January 2019 Gallup poll suggests Americans are “split on whether the economy is in overall good shape.”6 A September 2018 YouGov poll suggested a similar split.7 But these polls still may mask an underlying pessimism among the LMI population. Another recent Gallup poll shows that higher-income individuals are more likely to report a strong economy than are lower-income individuals, which supports the phenomenon of repeatedly low values of the LMI Economic Conditions Index relative to current national economic conditions.8

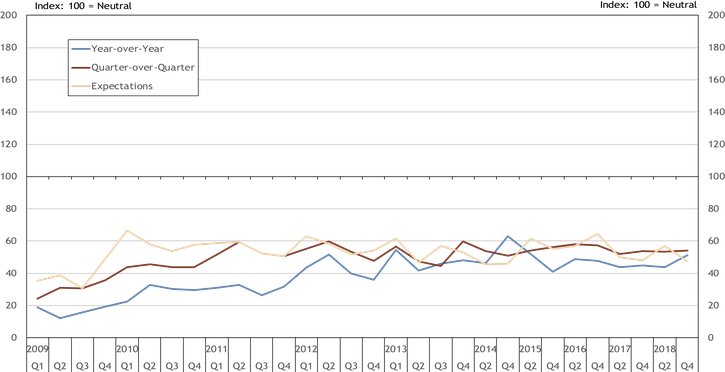

The LMI Demand for Services Index, another broad measure of economic conditions in the LMI community, rose to 51.4 from 43.7. The LMI Demand for Services Index reflects the demand for services from survey respondents, who are largely social- and community-services providers. Greater demand reflects poorer economic conditions and reduces the value of the index. The index has varied little over the survey’s history in a range well below neutral (Chart 3). The continued low value of the LMI Demand for Services Index indicates the LMI community’s ongoing need for services. As a result, it tempers some recent optimism that economic conditions may be stabilizing in the LMI community.

Chart 3: LMI Demand for Services Index

Source: Federal Reserve Bank of Kansas City LMI Survey.

Notes: The survey asks respondents to assess conditions relative to the same period in the previous year, conditions relative to the previous quarter and for their expectations for the following quarter relative to the current quarter. The LMI Demand for Services Index is calculated differently than other indexes so that an increase in the demand for services leads to a decrease in the index. See the box in the text for details.

Still, based on survey comments, the LMI Demand for Services Index arguably could have been higher in the absence of special circumstances. The most prominent of these is the partial federal government shutdown. A significant number of survey respondents reported that furloughed federal workers had sought their services, especially later in the shutdown. Also affected were contract workers who went unpaid. Going forward, repercussions of the partial shutdown could continue. While furloughed workers and working but unpaid federal government workers are authorized to receive back pay, contract workers, many of whom are low paid, may not receive compensation for lost income.9 The expectations index for the demand for services component of the LMI Survey fell sharply to 47.2 from 56.9, while both the backward-looking year-over-year and quarter-over-quarter indexes improved.

Survey contacts reported that a harsh early winter increased the demand for utility assistance, as well as cold-weather items such as blankets, coats and shoes. Higher utility bills can in turn affect other service providers. For example, higher utility bills may leave fewer resources available for food and health care, which could increase the demand for services provided by food banks and indigent medical providers. Further, shelters saw increased demands from the homeless, who may live outdoors in more agreeable weather conditions.

Finally, a couple of service providers reported increased efforts to market their services, which has not been common in past surveys. Examples included updated websites and special programs. Marketing efforts are important in understanding the demand for services, as an increased demand due to marketing is very different from an increased demand for services due to needs in the community. Marketing of services is important in making needy individuals and families aware of the services available to them.

Survey contacts reported heavy demand for food and gift items and consumer loans around the Thanksgiving and Christmas holidays, although comments were not clear about the level of this demand relative to previous years. In addition, many areas were reported to have inadequate capacity to support an increased demand for mental health and substance abuse disorders.

I-B. Labor Market Conditions

Labor market conditions provide significant support to improvements in the economic outlook in LMI communities, as measured by the LMI Economic Conditions Index. While jobs are available for LMI workers, there remain some significant structural issues, such as a low labor force participation rate. Additionally, wage growth, while better, only recently has emerged and remains sluggish relative to price increases for some goods making up large shares of LMI household budgets.

Basic Labor Market Metrics

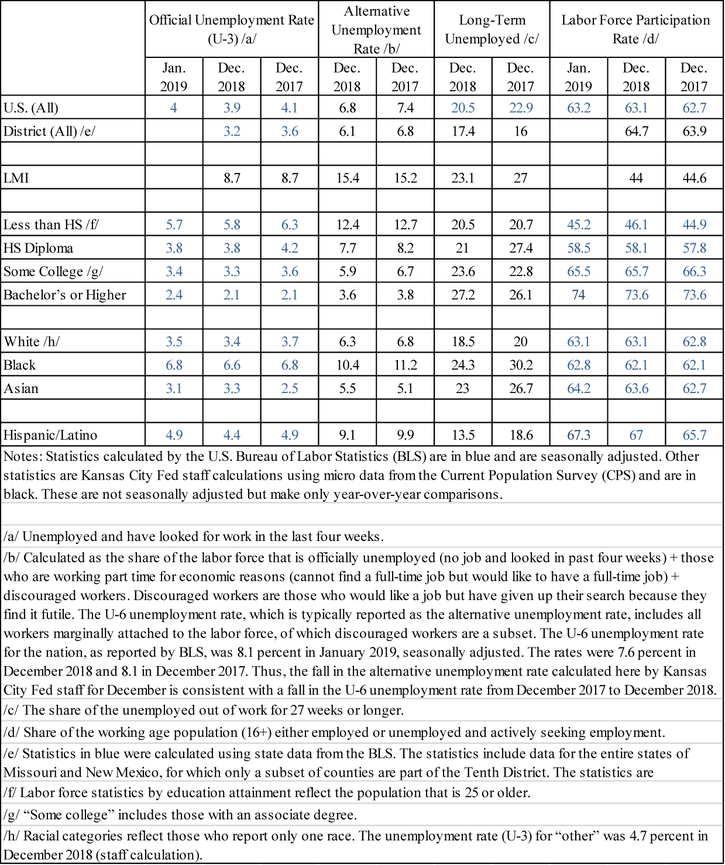

This issue contains an expanded set of labor market metrics (Table 2). In particular, the metrics include more complete statistics by education, race and ethnicity, and provide additional information for the Tenth District. The Bureau of Labor Statistics (BLS) data in the table are seasonally adjusted. Staff calculations, which compare year-over-year only, are not seasonally adjusted.

Table 2. Labor Market Metrics

Unemployment rates remained historically very low for both the nation and for the Tenth District, as well as for minorities and the less educated, who typically are more likely to be unemployed and low-income than are white non-Hispanics and the highly educated. The official U.S. unemployment rate was 3.9 percent in December, down from 4.1 percent in December 2017 (4.0 percent in January 2019). The unemployment rate was up from 3.7 percent in November, but due largely to new entrants into the labor force looking for jobs (the unemployment rate is the number of unemployed divided by the labor force). The Tenth District unemployment rate, which typically is lower than the national rate, was 3.2 percent in December, down from 3.6 percent in December 2017.

An alternative unemployment rate calculated for this report, which includes not only the officially unemployed (those who sought work in last four weeks) but also discouraged workers and reluctant part-time workers, was 6.8 percent nationally in December, down significantly from 7.4 percent in December 2017. Discouraged workers are those who would like a job but are not actively seeking employment because they find the search to be futile. This alternative unemployment rate was 6.1 percent in the Tenth District in November.

The November unemployment rate for workers in LMI households was considerably higher than for the nation as a whole at 8.7 percent, unchanged from December 2017. Consistent with these elevated unemployment rates were higher unemployment rates for the less educated and minorities, who are more likely to be low income. The higher alternative unemployment rate for the LMI, which was 15.4 percent in December, is consistent with a higher rate of reluctant part-time workers in LMI communities. Low-wage workers are about 3.5 times more likely to work part time than are high-wage workers, and low-wage workers are about three times more likely to be involuntary part time than are high-wage workers.11

The national labor force participation rate was 63.1 percent in December (63.2 in January 2019), up from 62.7 percent in December 2017. The long-run trend for the labor force participation rate is downward, and it remains well below the pre-recession level of 66 percent (December 2007) and its peak of 67.2 percent in the late 1990s. The trend is largely demographic, but the labor force participation rate of prime-age men (ages 25 to 54) is declining, which can be attributed largely to the decline in middle-skill jobs.12

The LMI labor force participation rate, at 44 percent in December, down from 44.6 percent in December 2017, was substantially lower than the participation rate for the working-age population as a whole.13 A lack of child care and adequate transportation are significant factors that keep LMI individuals from joining the labor force, as well as a lack of basic skills necessary to secure and maintain employment.14 Health issues and related disabilities also are a significant deterrent to labor force participation.15

LMI Job Availability Index

LMI Survey responses largely align with the strength in the labor market evident in labor market statistics. The LMI Job Availability Index advanced from 130.8 to 135.7 in the January survey, following a surge from 116.6 in the previous survey period (Chart 4). The index is at its highest level since the survey started in 2009 and is well above neutral. Almost half of survey respondents reported jobs were more available compared with the previous year (Chart 2). The quarter-over-quarter index also advanced, rising sharply from 124.9 to 136.1, a peak for that index. Expectations about job availability going forward also were more optimistic.

Chart 4. LMI Job Availability Index

Source: Federal Reserve Bank of Kansas City, LMI Survey.

Note: The survey asks respondents to assess conditions relative to the same period in the previous year, conditions relative to the previous quarter and for their expectations for the following quarter relative to the current quarter.

Although the consensus among survey contacts is that there are plenty of jobs available and that the number is increasing, they note that many LMI individuals are unable to participate in the labor market, which is consistent with the low labor force participation rate discussed above. Among the barriers mentioned, in addition to a lack of adequate child care, transportation and basic skills, were mental health issues and substance abuse. There does appear, however, to be some success in placing hard-to-employ individuals, as workers with criminal histories increasingly have been able to secure jobs. On the other hand, multiple comments expressed difficulty placing those with disabilities into jobs.

A common challenge raised by survey contacts was that although jobs are available, and indeed, even low-skill jobs remain unfilled, LMI workers are unable to earn a “livable wage” in the jobs that are available. In many cases, the lack of good-paying jobs for LMI workers was attributed to the need for better education and additional training opportunities, as there are numerous positions that remain vacant due to an insufficient supply of high-skill workers. In addition, survey contacts mentioned the lack of benefits available to low-wage workers.

While wage growth has been sluggish overall, growing at an inflation-adjusted rate of 1.1 percent annually over the last five years, wage-growth in typically low-wage industries largely has kept pace. For example, wages in the retail and leisure and hospitality industries have increased at inflation-adjusted annual rates of 1.1 percent and 2.1 percent, respectively, over the last five years. Still, the chief concern is that the level of these wages remains low. Wage growth may not be sufficient to compensate for increases in the price of the typical LMI household market basket.

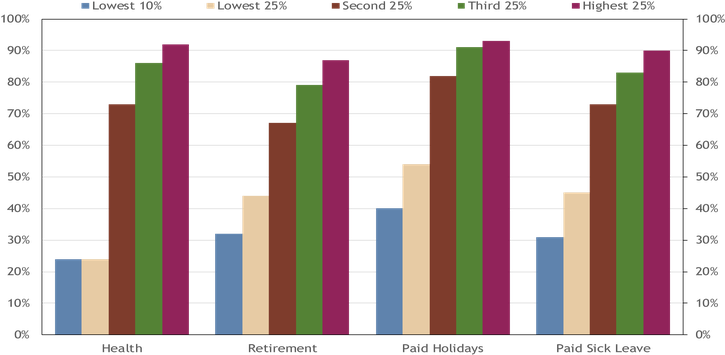

Data from the 2018 National Compensation Survey provide ample support for survey comments on the lack of benefits available for low-wage workers (Chart 5).17 Among those in the lowest 25 percent of the wage distribution, 25 percent are offered access to health benefits, 44 percent are offered access to retirement programs, 54 percent are provided with paid holidays and 45 percent receive paid sick leave. By comparison, among those in the top 25 percent of the wage distribution, 92 percent have access to health benefits, 87 percent have access to retirement plans, 93 percent receive paid holidays and 90 percent receive paid sick leave. The lack of access to fringe benefits is extremely pronounced in the bottom quartile, as access to benefits begins to rise markedly with wages in the second-lowest 25 percent of the wage distribution.

Chart 5: Access to Fringe Benefits by Wage Quantile

Source: U.S. Bureau of Labor Statistics, National Compensation Survey, 2018.

Note: “Lowest 10%” refers to access to benefits for those in the bottom 10 percent of the wage distribution, and so on.

Access to benefits also is less common in part-time jobs, which LMI workers are more likely to fill, and in industries that employ a disproportionate share of LMI workers, due largely to more limited education and training requirements. For example, 86 percent of full-time workers have access to employer-sponsored health benefits, while only 22 percent of part-time workers have access to health benefits. Retirement plans are available to 77 percent of full-time workers, but only 39 percent of part-time workers. Only 32 percent of employees in accommodations and food service occupations have access to health benefits, compared with 92 percent in manufacturing occupations. For retirement benefits, the figures are 34 percent and 84 percent, respectively.

I-C. Housing Affordability

The LMI Affordable Housing Index increased strongly from 63.7 to 81.7 in the January survey. However, more data are necessary to determine if the January 2019 increase is a meaningful upsurge or more of a blip. The index saw a similar bounce in the January 2017 survey that proved to be temporary. Further, the index remains appreciably below neutral and its 2013 peak of 90.1, and survey respondents continue to express concerns about the cost of housing.

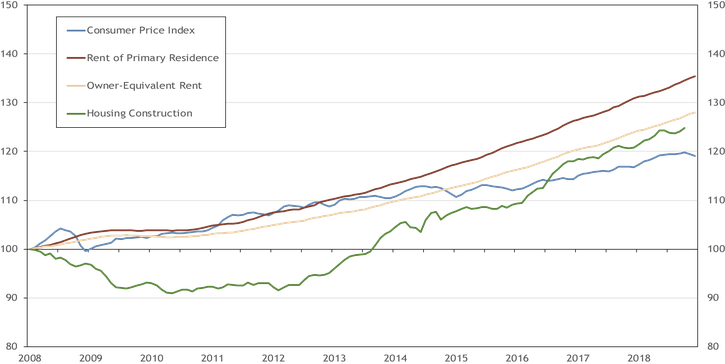

Among the most common concerns expressed by LMI Survey participants is the cost of housing, particularly compared with low wages that have not increased as quickly as the cost of housing. As a result, the LMI Affordable Housing Index consistently declined from 2013 until its January rebound. Over the same period, rents, as measured by the rent of primary residence component of the Consumer Price Index (CPI), began to increase at a much faster rate than overall inflation (Chart 6). The cost of owner-occupied housing, as measured by owner-equivalent rent (also a component of the CPI) began to outpace inflation around 2015, as house prices began to increase faster than overall inflation. Growth in housing costs has tamed in recent months, however. In 2018, rent of primary residence increased 3.2 percent, compared with an annual rate of 3.8 percent from 2015-17. In the fourth quarter of 2018, rents increased at an annual rate of only 2 percent. Owner-equivalent rents have seen a similar pattern, increasing at an annual rate of 1.7 percent in the fourth quarter, compared with 3 percent for 2018 and 3.3 percent from 2015-17. This change in housing cost inflation may explain, at least in part, the sizeable rebound in the LMI Housing Affordability Index in the January survey,

Chart 6. Selected Housing Cost Indexes

Sources: U.S. Bureau of Labor Statistics; U.S. Census Bureau (housing construction); Haver Analytics.

In the LMI Housing Affordability Index, there was more significant variation in assessments across survey respondents than is typically seen in other survey indexes (Chart 2). While 38.2 percent stated that affordable housing had become less available, 19.8 percent indicated it had become more available.

A few comments supported an assessment that affordable housing was increasingly available. While not a positive development in most regards, one survey comment suggested that affordable housing is more available in rural areas simply because households have left the area. Some comments noted that new programs and increased housing assistance were available in their areas, but these comments were not common, and, as reported in this issue’s special topic, some federal housing assistance was limited during the government shutdown.

On the downside, multiple comments stressed that higher costs of construction and labor shortages had limited opportunities to build new affordable housing. Indeed, as reported by the Census Bureau, the cost of housing construction has increased at an annual rate of 4.7 percent over the last three years (Chart 6). Another problem is a lack of existing housing to convert to affordable units. Survey respondents also expressed concerns about gentrification and difficulties in finding affordable housing for those with disabilities or other special needs.

I-D.Access to Credit

The LMI Credit Access Index advanced to 91.5 from 82.5, approaching a neutral level and reaching a historical peak (the index was 91.1 in the July 2015 survey). But while the index is approaching neutral, only 10.9 percent of respondents stated that access to credit had improved for the LMI population (Chart 2). Almost 70 percent of respondents rated access to credit as unchanged. Comments largely focused on poor credit histories and higher borrowing costs. Survey contacts noted that credit histories, particularly credit scores, significantly limited access to credit in LMI communities and also reported a proliferation of court-appointed conservatorships. Credit scores are highly correlated with incomes. A statistical analysis of census tract median household incomes and Equifax credit scores (RiskScores) across the United States by Kansas City Fed staff revealed a correlation of about 0.67, indicating that low-income census tracts typically have lower average credit scores.18

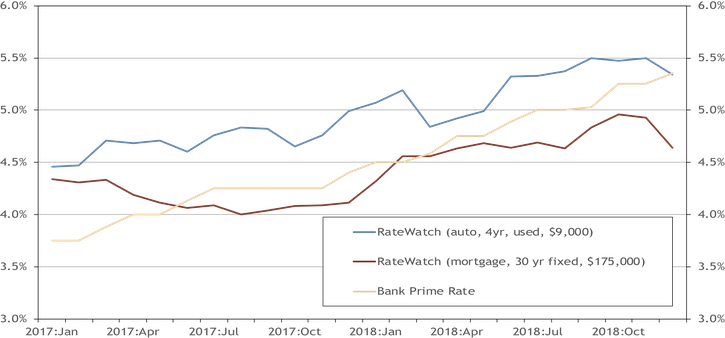

Survey contacts expressed concerns that rising interest rates would further burden LMI households with heavy debts and make loans less accessible to potential LMI borrowers. The bank prime rate has increased rather significantly over the last two years, from 3.75 percent in January 2017 to 5.35 percent in December 2018, but increases in other consumer interest rates have been more subdued (Chart 7). The average interest rate on a four-year, $9,000 loan for a used vehicle increased from 4.46 percent to 5.34 percent, while the average interest rate on a 30-year, fixed rate, $175,000 mortgage increased from 4.34 percent to 4.64 percent. But December 2018 rates were down significantly from only two months prior, when the average mortgage rate was 4.96 percent and the average rate on a used car was 5.47 percent.

Chart 7: Selected Interest Rates

Sources: RateWatch; Federal Reserve Board of Governors; Haver Analytics.

Survey contacts continued to express concerns about the use of alternative financial institutions such as payday lenders and pawnbrokers and the burden of student loan debt. News organizations reported that some furloughed federal government workers turned to these alternative financial institutions to make ends meet during the recent partial shutdown of the federal government.19 Small business lending was reported to have eased, while lending to consumers was reported to have tightened.

Summary

Results from the January 2019 LMI Survey and other data suggest that economic conditions in LMI communities may be stabilizing. The overall assessment of survey contacts is nearing neutral following 10 years of reported deterioration and stagnation. Statistics reveal a tight labor market, and continued improvement of job availability for LMI workers. But while real wages have begun to grow, they have failed to keep pace with inflation in some items that make up disproportionate shares of LMI household budgets, such as rent and health care. Further, the demand for services from community organizations continues to increase, although temporary factors may have played a significant role. The stock of affordable housing remains inadequate, especially for special populations, and although the LMI Affordable Housing Index improved, survey comments largely were downbeat. Access to credit for LMI households appears to be limited by poor credit histories and rising interest rates.

II. In This Issue: Housing Assistance During the Partial Federal Government Shutdown

The recent partial federal government shutdown was the longest in U.S. history, spanning from Dec. 22, 2018, to Jan. 25, 2019. During this time, unfunded or underfunded agencies suspended many of their programs, staffed essential employees without pay, and/or furloughed nonessential employees. The federal government’s partial shutdown had potentially significant repercussions for some low-income populations who rely on public assistance for basic necessities. Recent research shows that 40 percent of Americans cannot cover a $400 emergency expense, and the share is much higher for low-income households.20 Thus, many low-income households likely would find it difficult to weather any losses in benefits, even if temporary.

While not all public assistance programs were directly affected by the government shutdown, housing assistance programs potentially were at greater risk because the U.S. Department of Housing and Urban Development (HUD) and U.S. Department of Agriculture (USDA), which are responsible for most housing assistance programs, lost much of their funding, including all of their discretionary funding. Mandatory spending can be appropriated longer or differently, and in many cases was not directly affected by the shutdown.21 But certain low-income housing assistance programs were impacted, and some effects could have been more severe had the shutdown persisted longer. Many low-income households that rely on housing assistance likely would be unable to pay their rent if required to do so without assistance.22

HUD housing programs support about 90 percent of households receiving federal rental assistance, indicating there are relatively fewer households relying on USDA rental assistance.23 We therefore focus on HUD-administered programs. But we realize for those households in USDA programs, the consequences of the lack of, or delay in, rental subsidies likely would be the same as those for renters in HUD programs. This section highlights three of the larger low-income housing assistance programs administered by HUD and how they were affected by the government shutdown.

Housing Choice Voucher Program (Section 8)

HUD’s Housing Choice Voucher Program (Section 8) is the federal government’s major program for assisting low-income families with housing, as well as the elderly and disabled, and is administered by local public housing agencies.24 Since the Housing Choice Voucher Program is financed on a calendar year basis, the monthly payments under the shutdown remained funded through March 1. It is uncertain what the implications for the voucher program would have been had the government shutdown lasted sufficiently long that funds became unavailable. In addition, at least some new applications for assistance (for those coming off the waiting list) were unprocessed or delayed, perhaps due to lower staffing levels at HUD.25

Section 8 Project-Based Rental Assistance

Another critical HUD housing assistance program is Section 8 Project-Based Rental Assistance, which is a public-private partnership.26 The program relies on multiyear contracts in which private landlords commit to reserving some or all of their units for low-income households. The program supports over 2 million people in 1.2 million households.27 Under this program, low income renters pay the maximum of either 30 percent of income (adjusted for certain deductions), 10 percent of gross income, the portion of public assistance designated for housing, or the minimum rent established by HUD.28 HUD then provides a rental subsidy to cover the difference between what low income renters pay and the charge for the rental unit. This subsidy is provided directly to the private owner of the unit.

Under HUD’s contingency plan, the Department would “make payments under Section 8 (Project-Based Rental Assistance) and Project Rental Assistance Contracts (PRACs) where there was a permanent or indefinite authority or multiyear funding, or where there was budget authority available from prior year appropriations or recaptures.”29 However, HUD staff suggested that it only had sufficient resources for Section 8 Project-Based Rental Assistance through January and that funding would then be uncertain.30 HUD spokesman Jereon Brown said in an article by The Washington Post that “[HUD] budget and contract staff [were] ‘scouring for money’ to figure out how to fund the contracts on an interim basis.”31

The HUD contingency plan also excepted “processing Section 8 and PRAC renewals for expiring contracts and processing amendment funds for non-expiring Section 8 contract renewals,” and HUD recognized that these payments may have required processing renewals for expiring contracts. Nevertheless, there were over 1,000 housing contracts under the Section 8 Project-Based Rental Assistance Program that expired during the government shutdown, which is estimated to have affected 40,000 households. HUD said it could not renew most of those contracts that expired or were soon to expire due to a funding shortfall. On Jan. 4, HUD sent a letter to landlords saying owners of some properties could request releases from their reserves to cover funding shortfalls caused by non-payments of monthly rental subsidies, however, this release seemed to apply only to those with FHA-insured mortgages or Section 202/811 capital advances.34

Although the federal government is now open, the shutdown likely will cause a backlog that will further delay the processing of these contracts.35

Reports indicate there was a delay in the disbursement of some rental subsidies and contract renewals during the shutdown. Without these subsidies, private owners likely would experience a large and immediate drop in rental revenues that typically are used to cover routine costs. Specifically, some news reports suggested that some property owners resorted to using limited reserve funds for repairs and other costs, and landlords who lacked reserves asked renters to pay their full rent or face eviction.36

Though there were threats of evictions, there is no evidence of actual evictions during the shutdown. Federal law requires owners to provide a one-year written notice to tenants and HUD detailing their intention to renew or opt out of their contracts, and there are some protections in place for tenants whose landlords decide to opt out of the program.37 It is not clear, however, whether these protections are available during a government shutdown, particularly if a landlord intends to renew their contract.

Homeless Assistance Grant Program

HUD’s “Contingency Plan for Possible Lapse in Appropriations,” states that excepted “work during a lapse in appropriations includes the performance of functions … where the failure to perform those functions would result in an imminent threat to the safety of human life or the protection of property.”38 Activities have to meet a very strict legal standard for protecting life and property in order to continue.39 The Homeless Assistance Grant Program meets these strict criteria and continued to be funded.40 However, the government shutdown may have affected the program.

The Homeless Assistance Grant Program, which is funded by annual congressional appropriations, provides more than $2 billion annually to organizations that help resolve homelessness by addressing the short-term needs of homeless populations and providing longer-term solutions to reduce homelessness.41 In fiscal year 2018, the program supported more than 1 million people.42 Some supported organizations provide temporary shelter, while others provide the homeless with transitional jobs and shelter.

According to one news report, some organizations had not received January payments from HUD’s Homeless Assistance Grant Program by late January (thus, the problem, as inferred, was a delay), and used reserve funds originally intended for emergencies to cover rent, employee salaries, maintenance costs and other miscellaneous expenses that typically would have been funded by HUD grants.43 Presumably, the use of these funds for regular expenses would make fewer funds available to directly assist the homeless. Some representatives of organizations serving the homeless funded by grants were concerned that they would be required to reduce other services offered to the homeless or lay off staff members if the shutdown continued and they were to continue to deplete their reserves.44 Still, most insisted that they would not evict. Uncertainty seemed to be the chief concern, especially as the federal government reopened.45

Summary

The partial federal government shutdown in late December through most of January had the potential to impact a number of public assistance programs for low-income individuals and families. Among the most critical of public assistance programs is housing assistance. This section highlighted some housing assistance programs that were affected by the shutdown and found evidence of some disruptions or delays in housing assistance program payments.

The restoration of federal government functioning could potentially be temporary, and even if an agreement is reached to fully fund the federal government through the fiscal year, government shutdowns are a recurring problem. There have been 21 government shutdowns since the 1970s, including the 2018 shutdown.46 Should a government shutdown last longer, the problems highlighted here likely would worsen as voucher-based rent subsidies could be affected and landlords may lose confidence in federal housing assistance programs.

[1] A survey of the LMI population itself is intractable for many reasons. For details, see Kelly D. Edmiston, 2018, “Reaching the Hard to Reach with Intermediaries: The Kansas City Fed’s LMI Survey,” Federal Reserve Bank of Kansas City Research Working Paper 18-06, July. Available at https://www.kansascityfed.org/~/media/files/publicat/reswkpap/pdf/rwp18-06.pdf

[2] All references to index values reflect assessments of conditions relative to one year ago unless stated otherwise. The survey also asks respondents to assess conditions relative to the previous quarter and for their expectations for the following quarter. Results for all indexes are reported in index charts and tables. To enhance uniformity, the order of the survey questions was altered in the January survey. Specifically, the question asking for an overall assessment of economic conditions was moved to question number 5 from question number 4, switching places with the question that asks about access to credit. While theoretically question order can affect a survey’s outcome, we believe this small change was unlikely to have had a measurable impact on the outcome, as movements in survey indexes were consistent across indexes.

[3]In this issue, the index was changed from “LMI Services Needs Index” to “LMI Demand for Services Index” in an effort to better reflect what the index is measuring.

[4] Centers for Disease Control and Prevention, Behavioral Risk Factor Surveillance System. See the Sept. 4, 2018, issue of LMI Economic Conditions, which discusses income and health in detail as a special topic.

[5] U.S. Bureau of Labor Statistics /Haver Analytics; Federal Reserve Bank of Kansas City staff. See also the Sept. 4, 2018, issue of LMI Economic Conditions, Chart 2.

[6] Jim Norman, 2019, “Americans Becoming More Pessimistic About the Economy,” Gallup Organization, Jan. 22. Available at https://news.gallup.com/topic/economy.aspx About 48 percent of respondents said the economy is “getting better,” while about 44 percent said the economy is “getting worse.”

[7] Kathy Frankovic, 2018, “How Good Is the Economy?” YouGov, Sept. 14. Available at External Linkhttps://today.yougov.com/topics/politics/articles-reports/2018/09/14/how-good-economy

[8] Lydia Saad, 2018, “U.S. Mood Remains Mixed at End of 2018,” Gallup Organization, Dec. 28. Available at https://news.gallup.com/poll/245639/mood-remains-mixed-end-2018.aspx

[9] See Rachel Layne, 2019, “More than 1 Million Federal Contractors Hit by Shutdown Might Never See a Paycheck,” CBS News, Jan. 29. Available at External Linkhttps://cbsn.ws/2HGpemj. The Washington Post reported that federal contract workers typically earn $450 to $650 per week (Danielle Paquette, 2019, “The Lowest-Paid Shutdown Workers Aren’t Getting Back Pay,” The Washington Post, Jan. 29, available at External Linkhttps://wapo.st/2Sqnhi4).

[10] This alternative rate should not be confused with U-6, the typically reported alternative unemployment rate by the BLS that includes all individuals marginally attached to the labor market, of which discouraged workers are a subset. The U-6 unemployment rate for the nation, as reported by BLS, was 8.1 percent in January 2019, seasonally adjusted. The rates were 7.6 percent in December 2018 and 8.1 in December 2017. Thus, the fall in the alternative unemployment rate calculated by Kansas City Fed staff for December is consistent with a fall in the U-6 unemployment rate from December 2017 to December 2018, as reported by BLS.

[11] “Who Are Low Wage Workers?” Research Brief, U.S. Department of Health & Human Services, Office of the Assistant Secretary for Planning and Evaluation, Feb. 28, 2009.

[12] See Didem Tüzemen, 2018, “Why Are Prime-Age Men Vanishing from the Labor Force,” Economic Review, Federal Reserve Bank of Kansas City, 103(1), 5-30. Available at https://www.kansascityfed.org/~/media/files/publicat/econrev/econrevarchive/2018/1q18tuzemen.pdf

[13] BLS data are seasonally adjusted, while staff calculations are not, so one must be careful in directly comparing them. Still, the labor force participation rate is clearly much lower for those in LMI households.

[14] This topic was discussed at length in the March 2018 issue of LMI Economic Conditions.

[15] This problem was discussed in the September 2018 issue of LMI Economic Conditions.

[16] Average weekly earnings adjusted by the Consumer Price Index. The “overall” rate of wage growth represents average weekly earnings across all private industries.

[17] U.S. Bureau of Labor Statistics. Data are available at External Linkhttps://www.bls.gov/ncs/

[18] Data for median household income were taken from the Census Bureau’s 2017 American Community Survey. Median Equifax RiskScores were derived from individual credit report data provided in the Federal Reserve Bank of New York Consumer Credit Panel (CCP). The CCP is a 5 percent sample of all U.S. Equifax credit reports that is cleaned of any information that could be used to identify individuals.

[19] See Nicole Bullock, 2019, “Pawnshops and Payday Lenders Surge on U.S. Government Shutdown,” Financial Times, Jan. 20. Available at External Linkhttps://www.ft.com/content/e1fa8df8-1c4a-11e9-b126-46fc3ad87c65

[20] Federal Reserve Board of Governors, 2018, “Report on the Economic Well-Being of U.S. Households in 2017,” May. Available at External Linkhttps://www.federalreserve.gov/publications/files/2017-report-economic-well-being-us-households-201805.pdf The study did not directly consider a relationship between income and ability to pay an emergency expense but did consider education and race and ethnicity, which are highly correlated with income. The less educated and minorities are more likely to be unable to finance an emergency expense with savings.

[21] For example, “core programs” of the USDA’s Food and Nutrition Service were excepted. Among these were the Supplemental Nutrition Assistance Program (SNAP), the Child Nutrition Program and the Special Supplemental Nutrition Program for Women, Infants and Children (WIC). But those programs were excepted only to the extent that funds were available to support the programs. See “FNS Contingency Plan For Shutdown Due to Lapse in Appropriations” at External Linkhttps://www.usda.gov/sites/default/files/documents/usda-fns-shutdown-plan.pdf. Funding for SNAP beyond its Jan. 20 cutoff under the Dec. 21 continuing resolution was provided by paying February SNAP benefits early. For details about early funding of SNAP benefits, see Jory Heckman, 2019, “USDA Buys Time for SNAP Under Shutdown—but for How Long?” Federal News Network, Jan. 15. Available at External Linkhttp://bit.ly/2GbCI7N

[22] See, for example, “Diane Yentel on the Government Shutdown and HUD Assistance Programs,” Washington Journal, Jan. 21, 2019, available at External Linkhttps://cs.pn/2HHcwU9

[23] Center on Budget and Policy Priorities, 2017, “Policy Basics: Federal Rental Assistance, Nov. 15. Available at External Linkhttps://www.cbpp.org/research/housing/policy-basics-federal-rental-assistance

[24] Voucher-holders may live in any private housing where the owner agrees to rent under the program and that meets HUD requirements. Once they have selected their housing, the public housing agency pays the landlord a subsidy on behalf of the family and the family pays the difference between the actual rent charged by the landlord and the amount subsidized by the program

[25] See National Low-Income Housing Coalition, 2018, “Federal Government Shuts Down. What Does It Mean for HUD Programs?” Dec. 22. Available at External Linkhttp://bit.ly/2Sdf3uc. The National Association of Home Builders noted that “there may be a few first time payments that are missed.” See “Impact of the Government Shutdown on Housing,” Jan. 9, 2019. Available at https://www.nahb.org/en/advocate/impact-of-government-shutdown.aspx. For a related news report that highlights a specific case, see Suzy Khimm, 2019, “The Shutdown Is Over, but the Pain for Low-Income Families Lingers,” Jan. 29, NBC News. Available at External Linkhttps://nbcnews.to/2RGkEnG. HUD, in their contingency plan, states that Tenant Rental Assistance Certification System (TRACS) would be available to process vouchers, provided that appropriate funds were available (see “HUD Contingency Plan for Possible Lapse in Appropriations 2018,” available at External Linkhttps://www.hud.gov/sites/documents/HUDCONTINGENCYPLANFINAL.PDF, p. 73).

[26] There are other, smaller project-based rental assistance programs that operate under similar rules. One such program is “project-based vouchers” which is a hybrid between Section 8 Project Based Rental Assistance and more traditional voucher programs. See Center on Budget and Policy Priorities (CBPP), 2017, “Policy Basics: Section 8 Project-Based Rental Assistance,” Nov. 15. Available at External Linkhttps://www.cbpp.org/research/housing/policy-basics-section-8-project-based-rental-assistance

[27] CBPP, supra note 23. See also HUD, “Renewal of Section 8 Project-Based Rental Assistance.” Available at External Linkhttps://www.hud.gov/hudprograms/rs8pbra

[28] See HUD, “Renewal of Section 8 Project-Based Rental Assistance,” supra note 27.

[29] See “HUD Contingency Plan,” supra note 25. PRACs fall under the HUD Section 202 and Section 811 programs, which provide housing for the elderly and persons with disabilities, respectively, through a capital advance program. In addition to the capital advance, project rental assistance funds are provided to cover the difference between the HUD-approved operating cost for the project and the tenants' contribution towards rent. Descriptions of these and other HUD multifamily programs are available on the HUD website at External Linkhttps://www.hud.gov/program_offices/housing/mfh/progdesc

External Link[30] National Low-Income Housing Coalition, 2019, “Government Shutdown Now into Third Week, Impacts Housing Programs and Tenants,” Jan. 7. Available at External Linkhttp://bit.ly/2Gevi3Y. The lack of certain funding beyond January could not be independently verified.

[31] Robert Costa and Nick Miroff, 2019,” As Shutdown Drags On, Trump Officials Make New Offer, Seek Novel Ways to Cope with its Impacts,” Jan. 6, The Washington Post. Available at External Linkhttps://wapo.st/2ScCunB

[32] “HUD Contingency Plan,” supra note 25.

[33] Douglas Rice, 2019, “Seniors, Families, and Others Risk Losing Housing as Shutdown Continues,” Jan. 9. Available at External Linkhttp://bit.ly/2DMRhMF. The National Low-Income Housing Coalition identified over 1,000 housing contracts under the Section 8 Project-Based Rental Assistance Program that had expired. See National Low-Income Housing Coalition, “HUD Project-Based Rental Assistance Contract Expirations (Dec. 2018 – Feb. 2019),” which provides a map of expired or soon to expire HUD Project-Based Rental Assistance contracts as well as a list of these contracts. The data are available at External Linkhttps://nlihc.org/issues/budget/shutdown-map. These expirations have not been independently verified by Kansas City Fed staff.

[34] For HUD’s Jan. 4 letter to landlords, see External Linkhttps://wapo.st/2ShQ0VV. For more on Section 202/811 capital advances, see note 29.

[35] Lisa Rein, Tracy Jan and Kimberly Kindy, 2019, “Federal Employees Return to Backlog of Work after 35-day Shutdown,” The Washington Post, Jan. 28. Available at External Linkhttps://wapo.st/2Bc0Mna

[36] Examples include Sanjana Karanth and Arthur Delaney, 2019, “Some Renters Are Already Facing Eviction, Thanks to the Shutdown,” Jan. 16, available at External Linkhttp://bit.ly/2BdmsPL; Michael Esparza, “Web Extra: Government Standoff Putting Landlord and Tenants at Odds,” Fox16.com (Little Rock, Ark.), Jan. 14, available at External Linkhttp://bit.ly/2HK9rTn; Sophie Kasakove, 2019, “The Government Shutdown Could Decimate America’s Subsidized Housing Programs,” Pacific Standard, Jan. 22, available at External Linkhttp://bit.ly/2Shjq6N; Kriston Capps, 2019, “Low-Income Renters Face Eviction, Thanks to the Government Shutdown,” CityLab, Jan. 10, available at External Linkhttp://bit.ly/2G3Z9vy

[37] External Linkhttps://www.nhlp.org/wp-content/uploads/2018/04/Saving-HUD-Homes-pt-3.pdf, External Linkhttps://www.hud.gov/sites/documents/508FIN_CONSOL_GUIDE6_8_17.PDF.

[38] See “HUD Contingency Plan for Possible Lapse in Appropriations 2018,” available at External Linkhttps://www.hud.gov/sites/documents/HUDCONTINGENCYPLANFINAL.PDF

[39] Id.

[40] Id., p. 63.

[41] For more information on this program, see Libby Pearl, 2017, “The HUD Homeless Assistance Grants: Programs Authorized by the HEARTH Act,” Aug. 30, HUD. Available at External Linkhttps://fas.org/sgp/crs/misc/RL33764.pdf

[42] “Community Planning and Development Homeless Assistance Grants: 2018 Summary Statement and Initiatives” (budget document). Available at External Linkhttps://www.hud.gov/sites/documents/22-HOMELESSAGRANTS.PDF

[43] Glenn Thrush, 2019, “Shutdown’s Pain Cuts Deep for the Homeless and Other Vulnerable Americans,” The New York Times, Jan. 21, available at External Linkhttps://nyti.ms/2UxEhQS;.

[44] See, for example, Hannah Chanatry and Sharon Brody, 2019, “With Government Open, Boston’s Pine Street Inn Plans and Prioritizes,” WBUR News (Boston), Jan. 27, available at External Linkhttps://www.wbur.org/news/2019/01/27/downie-pine-street-inn-shutdown-crisis. See also Douglas Tallman, “Montgomery Nonprofits Provide Bleak Assessments as Shutdown Continues,” Montgomery Community Media (Alabama), Jan. 24, available at External Linkhttp://bit.ly/2HGJzaQ; George Myers and Haley Cawthorn, 2019, “Government Shutdown Impacts Kokomo’s Most Vulnerable,” Kokomo Tribune (Indiana), Jan. 18, available at External Linkhttp://bit.ly/2RWELmF

[45] See, for example Hannah Chanatry and Sharon Brody, 2019, supra note 44.

[46] Committee for a Responsible Budget, 2019, “Q&A: Everything You Should Know About Government Shutdowns, Jan. 7. Available at External Linkhttp://bit.ly/2TAkArx

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.