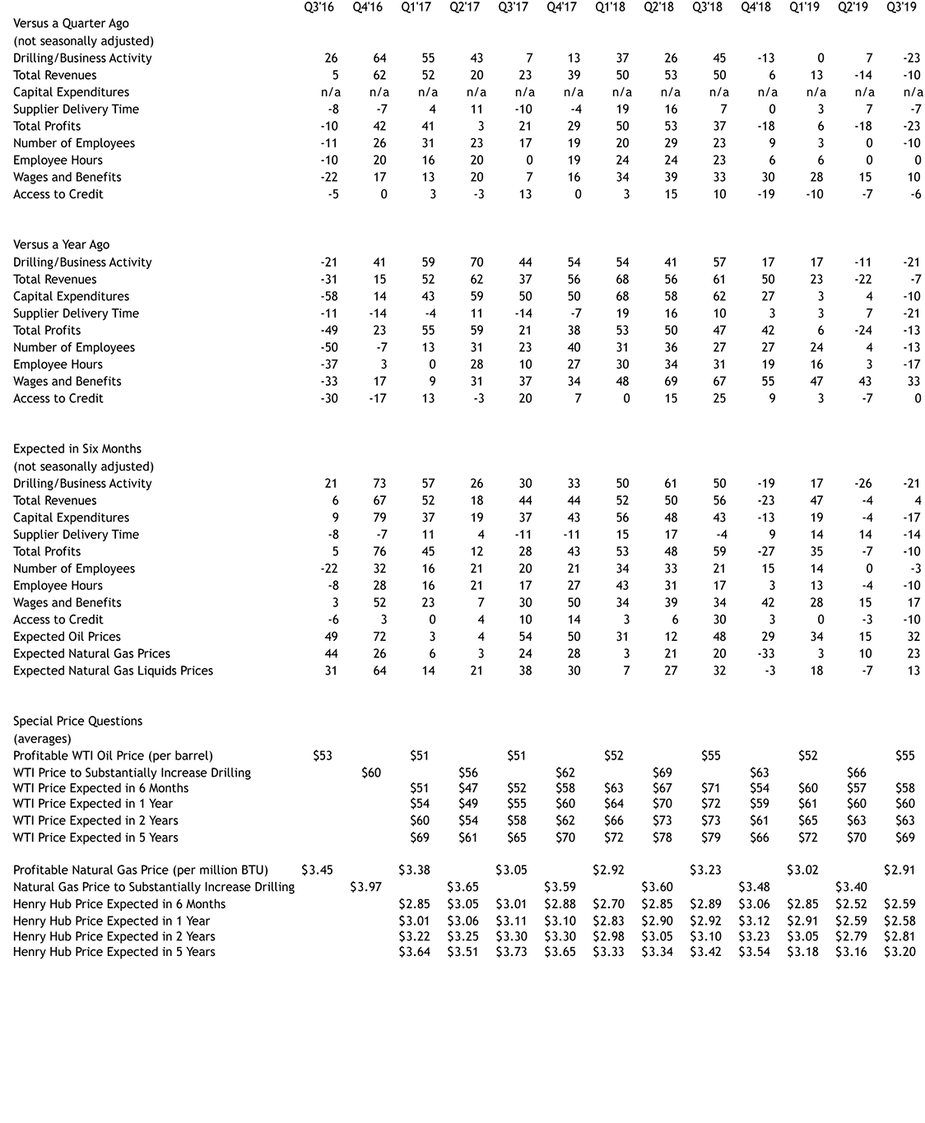

Summary of Quarterly Indicators

Tenth District energy activity decreased moderately in the third quarter of 2019, as indicated by firms contacted between September 16th and September 30th, 2019 (Tables 1 & 2). The drilling and business activity index fell from 7 to -23, indicating a significant drop in activity following a slight expansion in Q2 2019 (Chart 1). The wages and benefits index remained positive and the employee hours index remained flat. However, the revenues, supplier delivery time, profits, employment, and access to credit indexes all decreased.

Chart 1.

Drilling/Business Activity Index vs. a Quarter Ago

Skip to data visualization table| Date | Drilling/Business Activity |

|---|---|

| 2016Q3 | 26 |

| 2016Q4 | 64 |

| 2017Q1 | 55 |

| 2017Q2 | 43 |

| 2017Q3 | 7 |

| 2017Q4 | 13 |

| 2018Q1 | 37 |

| 2018Q2 | 26 |

| 2018Q3 | 45 |

| 2018Q4 | -13 |

| 2019Q1 | 0 |

| 2019Q2 | 7 |

| 2019Q3 | -23 |

Most year-over-year indexes fell as well. The year-over-year drilling and business activity index dipped further, from -11 to -21. Indexes for capital expenditures, delivery time, employment, and employee hours dropped into negative territory. However, year-over-year indexes for revenues and profits declined at a slower rate, and the access to credit index was flat. While the growth rate of the year-over-year wages and benefits index eased from last quarter, it was still highly positive.

Expectation indexes remained mostly negative. The future drilling and business activity index was -21, following a reading of -26 in Q2. The future capital expenditures, profits, employee hours, and access to credit indexes decreased further from last quarter. The future revenues and wages and benefits indexes increased, while the future delivery time and employment indexes turned negative. Meanwhile, the price expectations indexes all increased for oil and natural gas, and the price expectations index for natural gas liquids rose back up into positive territory.

Summary of Special Questions

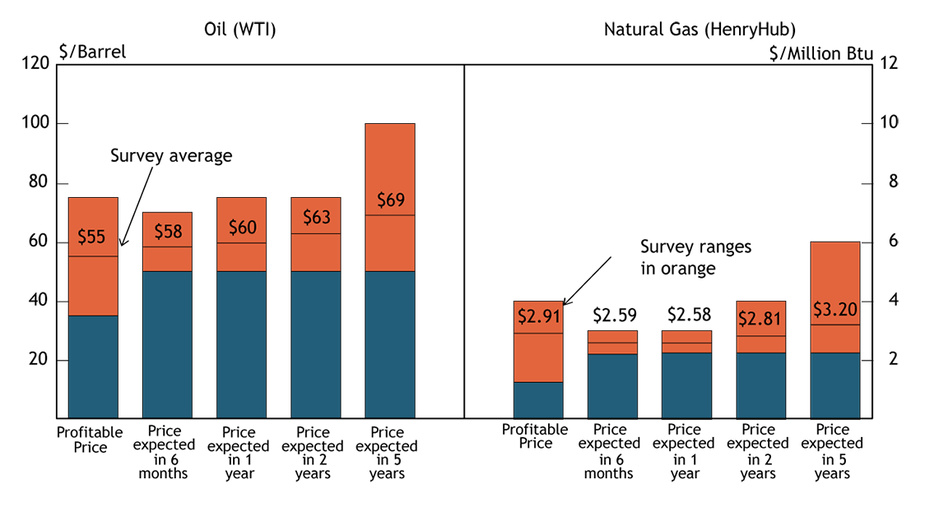

This quarter firms were asked what oil and natural gas prices were needed for drilling to be profitable on average across the fields in which they are active (in alternate quarters they are asked what price they need for a substantial increase in drilling). The average oil price needed was $55 per barrel, with a range from $35 to $75 (Chart 2). This average was up slightly from $52 in the first quarter of 2019 and matched the price reported in the third quarter of 2018. The average natural gas price needed for profitability was $2.91 per million Btu, with responses ranging from $1.25 to $4.00. For natural gas, this average was quite a bit lower than $3.02 in the first quarter of 2019 and $3.23 reported in the third quarter of 2018.

Chart 2. Special Question - What price is currently needed for drilling to be profitable for oil and natural gas, and what do you expect the WTI and Henry Hub prices to be in six months, one year, two years, and five years?

Source: Federal Reserve Bank of Kansas City

Firms were again asked what they expected oil and natural gas prices to be in six months, one year, two years, and five years. Expected oil prices were relatively similar to Q2 2019, but were still above price expectations from late 2018. The average expected WTI prices were $58, $60, $63, and $69 per barrel, respectively. Expectations for natural gas prices rebounded slightly from last quarter. The average expected Henry Hub natural gas prices were $2.59, $2.58, $2.81, and $3.20 per million Btu, respectively.

Firms were also asked about constraints limiting near-term growth in activity in the top areas where their firm is active (Chart 3). 60 percent of surveyed firms indicated that current low prices for oil and gas were the main constraints limiting near-term growth. Contacts also reported investor pressures for free cash flow, limited access to capital credit, lack of natural gas pipeline capacity, and problems finding workers as primary or secondary constraints to near-term growth.

Finally, respondents were asked about how trade tensions (tariffs) affected their business and expectations for the future. Around 70 percent of firms reported slightly or significantly negative effects from trade tensions on their business in the past year. A similar share of firms anticipated negative effects from trade policy on their business in 2020 (Chart 4).

Chart 3.

Special Question - Which of the following is the main constraint that is limiting near-term growth in activity in the top area in which your firm is active? Secondary constraint?

Skip to data visualization table| Constraint | Primary constraint | Secondary constraint |

|---|---|---|

| Current oil and or natural gas price too low | 60 | 25 |

| Investor pressure to generate free cash flow | 16 | 12.5 |

| Limited access to capital and credit | 4 | 16.66667 |

| Lack of natural gas pipeline capacity | 4 | 0 |

| Problems finding workers | 0 | 16.66667 |

| We are only constrained by the main constraint | 0 | 20.83333 |

| Other | 16 | 8.333333 |

Chart 4.

Special Question - How have trade tensions (tariffs) affected your business in the last year and how do you anticipate trade policy will affect your business in 2020?

Skip to data visualization table| Effect | How have trade tensions (tariffs) affected your business in the last year | How do you anticipate trade policy (tariffs) will affect your business in 2020 |

|---|---|---|

| Significantly negative | 3.846154 | 3.846154 |

| Slightly negative | 65.38462 | 61.53846 |

| None | 26.92308 | 34.61538 |

| Slightly positive | 3.846154 | 0 |

| Significantly positive | 0 | 0 |

Table 1 - Summary of Tenth District Energy Conditions, Quarter 3, 2019

Source: Federal Reserve Bank of Kansas City

Table 2 - Historical Energy Survey Indexes

Source: Federal Reserve Bank of Kansas City

Selected Comments

“I think the U.S. oil supply will continue to increase but at a lower rate than previous years - so prices for future supply coming online will be lower.”

“There is still an oil glut and global demand growth is tepid. We may begin to see results from the current capital restrictions sometime in late 2020. Middle East is strictly a wildcard at this point.”

“There is still much oil supply, but I anticipate a slowdown in U.S. production due to tight margins resulting in some upward movement in prices.”

“Declining shale production, fewer U.S. oil & gas companies exploring for new production, and lack of new resource plays factor into our price expectations”

“There is an overabundance of natural gas. In some regions they are having to pay people to take it. More infrastructure is needed.”

“I see an abundant supply of natural gas in the US and break-even prices for gas are very low in certain areas along with associated natural gas being produced along with oil. So overall too much supply available.”

“Prices are too low currently and will shut off more and more natural gas directed drilling. Declines are very high and once enough rigs drop, we will see HH prices start to really climb… gas that can get to Gulf Coast will sell for a premium.”

“Foreign demand for ethanol has significantly decreased from trade tensions.”

“Steel prices have gone up from tariffs which has added to our costs.”

“Costs of imported goods have increased - steel, artificial lift, etc. from trade tensions.”

“I believe oil is a couple dollars a barrel lower than it would be without trade tensions.”

“We need to finalize a trade deal with China to support global growth.”

Additional Resources

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author