Summary of Quarterly Indicators

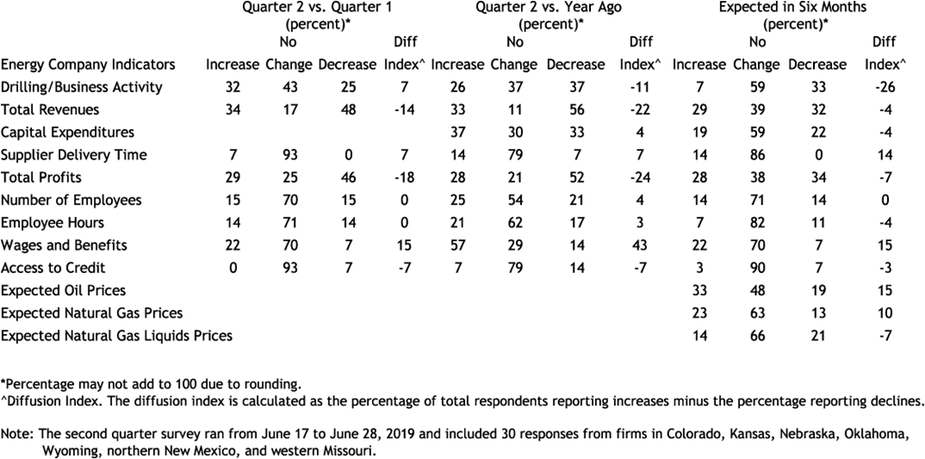

Tenth District energy activity expanded slightly in the second quarter of 2019, as indicated by firms contacted between June 17th and June 28th, 2019 (Tables 1 & 2). The drilling and business activity index increased from 0 to 7, indicating a modest expansion following flat activity in Q1 2019 (Chart 1). The delivery time index rose and the wages and benefits index also remained positive. However, the employment index was flat, and the revenues, profits, and access to credit indexes decreased.

Chart 1.

Drilling/Business Activity Index vs. a Quarter Ago

Skip to data visualization table| Date | Drilling/Business Activity |

|---|---|

| 2016Q2 | 0 |

| 2016Q3 | 26 |

| 2016Q4 | 64 |

| 2017Q1 | 55 |

| 2017Q2 | 43 |

| 2017Q3 | 7 |

| 2017Q4 | 13 |

| 2018Q1 | 37 |

| 2018Q2 | 26 |

| 2018Q3 | 45 |

| 2018Q4 | -13 |

| 2019Q1 | 0 |

| 2019Q2 | 7 |

Most year-over-year indexes decreased moderately. The year-over-year drilling and business activity index fell from 17 to -11. Indexes for revenues, profits, and access to credit also dropped into negative territory. Year-over-year indexes for capital expenditures and delivery time inched up, while the pace of expansion for the employment, employee hours, and wages and benefits indexes eased.

Expectation indexes fell, with the future drilling and business activity index dropping from 17 to -26, the lowest level since Q1 2016. The future revenues, capital expenditures, profits, employee hours, and access to credit indexes were negative. On the other hand, the future employment index was flat, while the delivery time and wages and benefits indexes remained positive. The oil price expectations index slowed from 34 to 15, and the natural gas price expectations index rose from 3 to 10.

Summary of Special Questions

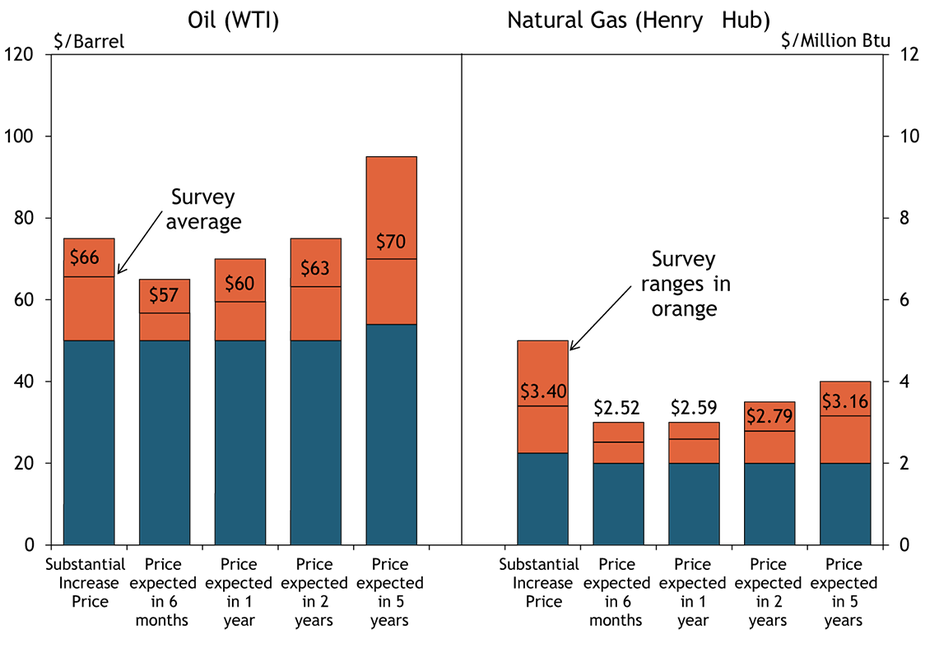

This quarter firms were asked what oil and natural gas prices were needed on average for a substantial increase in drilling to occur (in alternate quarters they are asked what price they need to be profitable on average across the fields in which they are active). The average oil price needed was $66 per barrel, with a range of $50 to $75 (Chart 2). This average was up slightly from $63 in the fourth quarter of 2018, but below the price reported in the second quarter of 2018. The average natural gas price needed was $3.40 per million Btu, with responses ranging from $2.25 to $5.00.

Chart 2. Special Question - What price is currently needed for a substantial increase in drilling to occur for oil and natural gas, and what do you expect the WTI and Henry Hub prices to be in six months, one year, two years, and five years?

Source: Federal Reserve Bank of Kansas City

Firms were again asked what they expected oil and natural gas prices to be in six months, one year, two years, and five years. Expected oil prices dipped since the last quarter, but were higher than price expectations from Q4 2018. The average expected WTI prices were $57, $60, $63, and $70 per barrel, respectively. Expectations for natural gas prices continued to decline. The average expected Henry Hub natural gas prices were $2.52, $2.59, $2.79, and $3.16 per million Btu, respectively.

Firms were also asked about any initiatives regarding water use/management (Chart 3). While 37 percent of surveyed firms reported they hadn’t undertaken any initiatives related to water management, 30 percent reported they’ve invested in water infrastructure. 30 percent of firms indicated they’ve begun initiatives to recycle/reuse water and 20 percent of contacts noted they have worked with landowners or local governments to deal with water management issues.

Finally, respondents were asked about expenditures on software, application development and related personnel. About 60 percent of firms reported they have increased these expenditures over the past two years, and 60 percent also expect to increase these expenditures over the next two years (Chart 4).

Chart 3.

Special Question - Has your company undertaken any initiatives regarding water use/management? (Check all that apply)

Skip to data visualization table| Initiative | Percent |

|---|---|

| Water recycling/reuse | 30 |

| Invested in water infrastructure | 30 |

| Instituted plans to reduce water use | 10 |

| Worked with landowners or local governments to deal with water management issues | 20 |

| Other | 0 |

| We have not undertaken any initiatives related to water management | 36.66667 |

Chart 4.

Special Question - How have your firm expenditures on software, application development and related personnel changed over the last two years, and what is your firm plan for these expenditures over the next two years?

Skip to data visualization table| Change | Last two years | Next two years |

|---|---|---|

| Large increase | 12 | 8 |

| Modest increase | 48 | 52 |

| No change | 28 | 36 |

| Modest decrease | 8 | 4 |

| Large decrease | 4 | 0 |

Table 1 - Summary of Tenth District Energy Conditions, Quarter 2, 2019

Source: Federal Reserve Bank of Kansas City

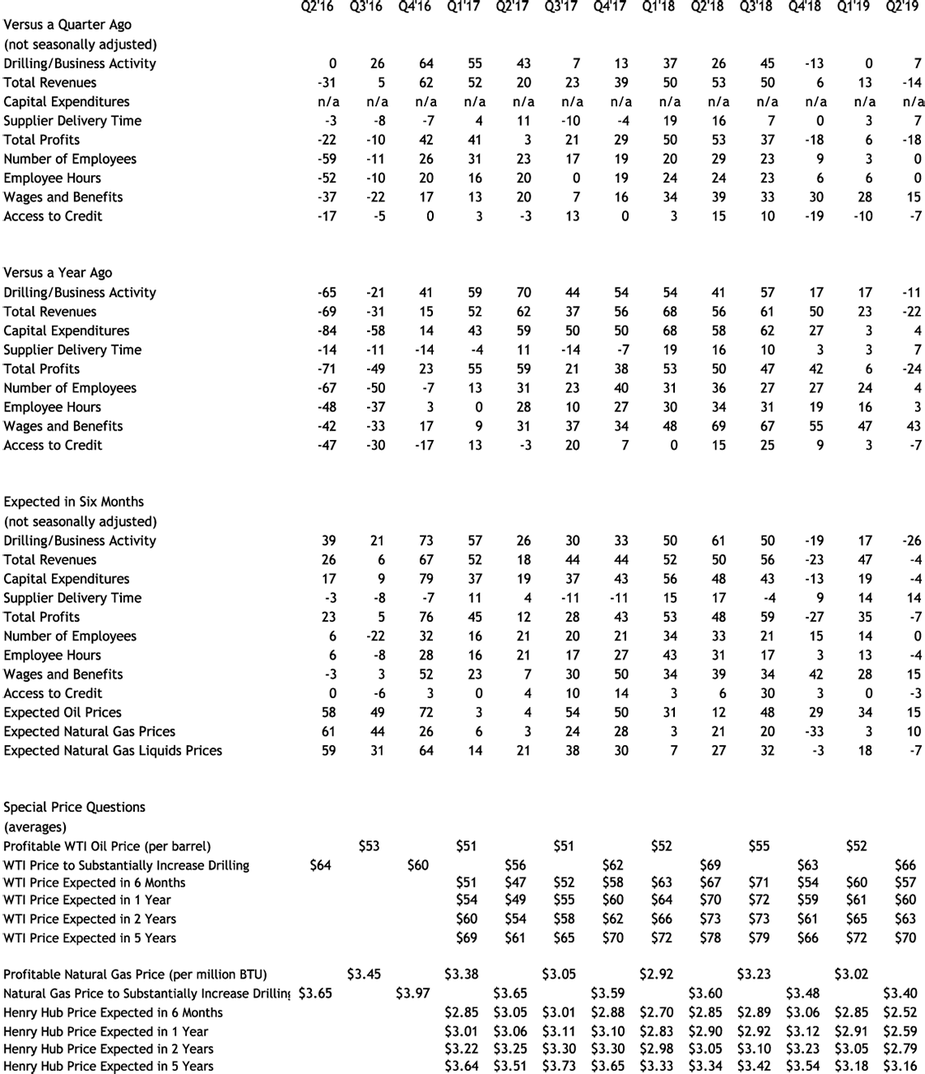

Table 2 - Historical Energy Survey Indexes

Source: Federal Reserve Bank of Kansas City

Selected Comments

“There are fewer independent oil & gas exploration companies operating in the mid-continent. The emphasis is on horizontal/lateral harvesting by the larger independents with little or no room for the E&P’s who drilled or explored for new production.”

“Natural gas is extraordinarily weak. We are likely to net less than $1.00 after transportation/marking. While gas price should rebound, any length to this recent downturn will have serious impacts on future activity.”

“There has been a drastic reduction in new well starts.”

“We continue to drive [business] costs down through engineering innovation and efficiencies.”

“I believe demand for crude oil will increase slightly each year, along with US production stabilizing in the next couple of years (i.e. likely increasing at a lower rate than we’ve seen in the past few years).”

“There is a current oversupply of natural gas, and I do not see this getting resolved in the next few years. We need additional pipelines, and other infrastructure, and to convert more vehicles, etc. to natural gas.”

“Gas is oversupplied but additional export capacity supports modest price increases.”

“Steel tariffs have caused increases in drilling costs.”

“Indirectly trade tariffs have affected us. The projected use of oil is lower and this has caused the price of oil to go down. We have had two contracts cancelled recently, which really hurt. Companies have had to revise downward their budgets for 2019 and they cut training.”

“Tariffs have not significantly affected our business.”

Additional Resources

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author