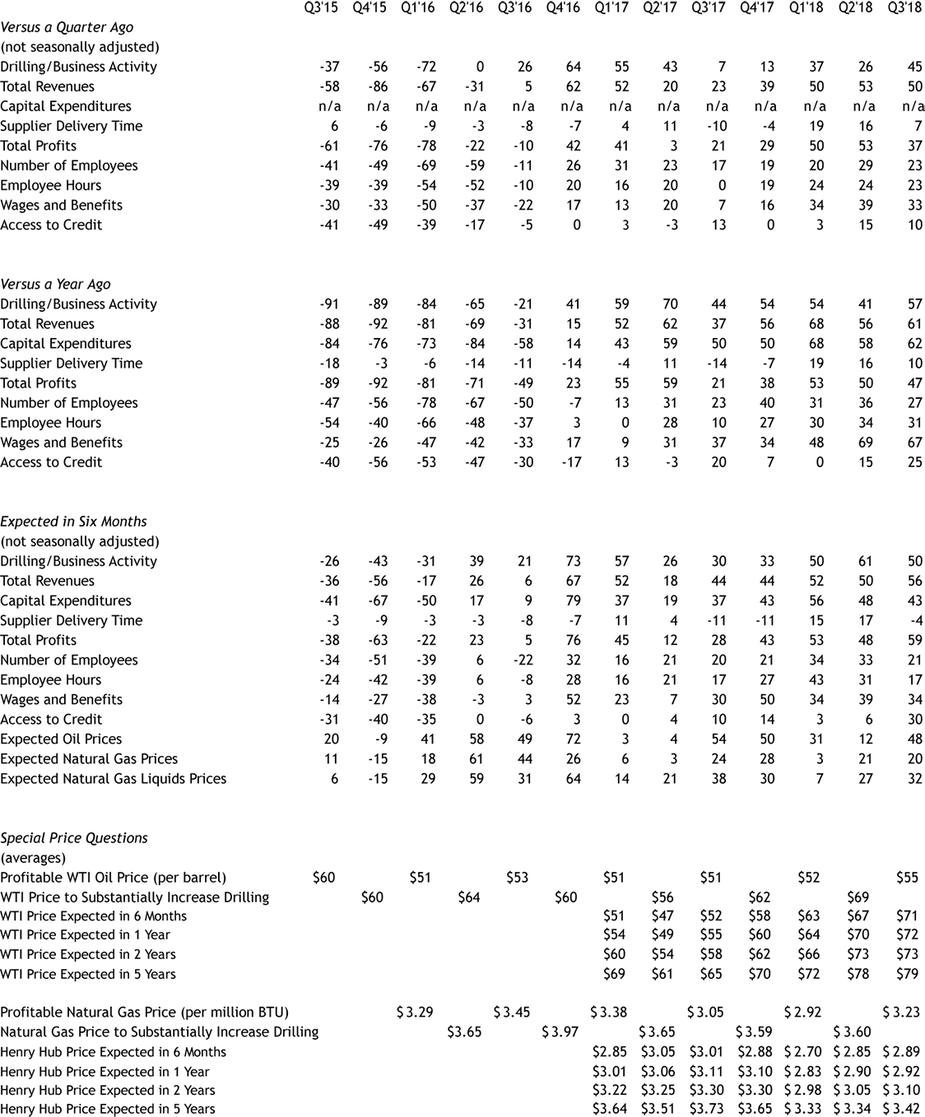

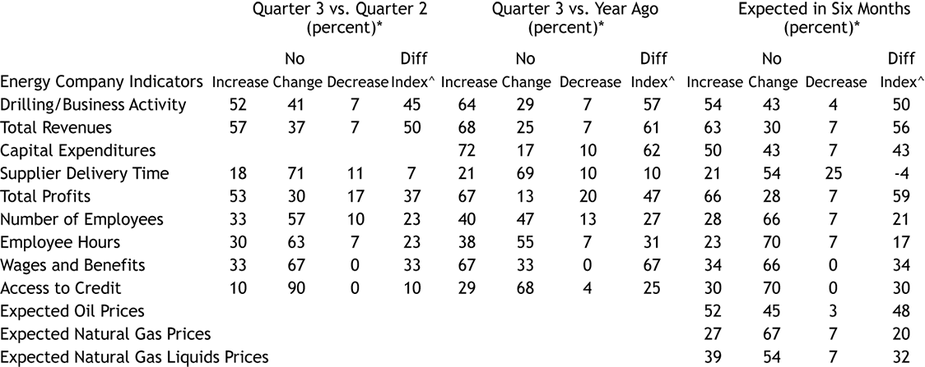

Summary of Quarterly Indicators

Growth in Tenth District energy activity accelerated in the third quarter of 2018, as indicated by firms contacted between September 14th and September 28th (Tables 1 & 2). The drilling and business activity index jumped from 26 to 45, the highest level since early 2017 (Chart 1). Other quarterly indexes were mixed, but all indexes remained positive, indicating expansion. The total revenues and employee hours indexes edged lower, and the employment, wages and benefits, and access to credit indexes also fell slightly. The supplier delivery time and total profits indexes declined.

Chart 1.

Drilling/Business Activity Index vs. a Quarter Ago

Skip to data visualization table| Date | Drilling/Business Activity |

|---|---|

| 2015Q3 | -37 |

| 2015Q4 | -56 |

| 2016Q1 | -72 |

| 2016Q2 | 0 |

| 2016Q3 | 26 |

| 2016Q4 | 64 |

| 2017Q1 | 55 |

| 2017Q2 | 43 |

| 2017Q3 | 7 |

| 2017Q4 | 13 |

| 2018Q1 | 37 |

| 2018Q2 | 26 |

| 2018Q3 | 45 |

Year-over-year indexes were also mixed. The year-over-year drilling and business activity index rose from 41 to 57, the highest posting in over a year. The year-over-year access to credit index also increased moderately to 25. The total revenues and capital expenditures indexes grew modestly, while the total profits, employee hours, and wages and benefits indexes edged lower but remained at high levels. The supplier delivery time and employment year-over-year indexes declined slightly.

Expectations for most indexes remained high. The future access to credit index increased from 6 to 30, the highest level in survey history. The future total profits index rose to the highest level since late 2016, and the total revenues index also increased modestly. Conversely, the future capital expenditures and wages and benefits indexes dipped slightly from high levels. The expected drilling and business activity index also remained high but declined from 61 to 50. The expected employment and employee hours indexes were somewhat lower, and the future supplier delivery time index fell into negative territory for the first time this year. The oil price expectations index increased considerably, from 12 to 48, while the natural gas price expectations index inched down.

Summary of Special Questions

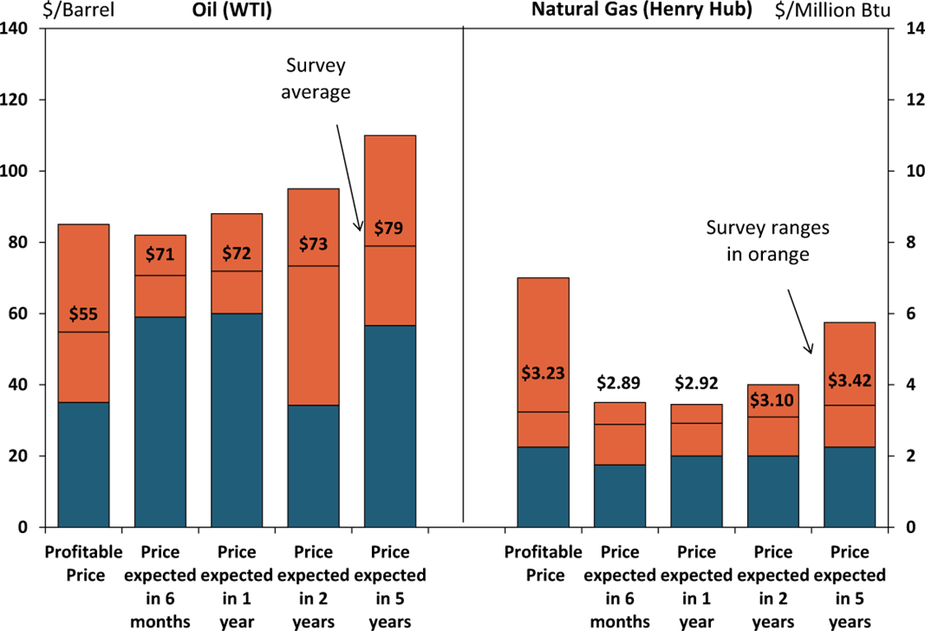

This quarter firms were asked what oil and natural gas prices were needed for drilling to be profitable on average across the fields in which they are active. The average oil price needed was $55 per barrel, with a range of $35 to $85 (Chart 2). This average was up from a range of $51 to $53 since first quarter 2016. The average natural gas price needed was $3.23 per million Btu, with responses ranging from $2.25 to $7.00. This was also an increase from the last two times the topic was surveyed.

Chart 2. Special Question - What price is currently needed for drilling to be profitable for oil and natural gas, and what do you expect the WTI and Henry Hub prices to be in six months, one year, two years, and five years?

Source: Federal Reserve Bank of Kansas City

Firms were again asked what they expected oil and natural gas prices to be in six months, one year, two years, and five years. Expected oil prices increased modestly since the last quarter. The average expected WTI prices were $71, $72, $73, and $79 per barrel, respectively. Natural gas price expectations also edged higher. The average expected Henry Hub natural gas prices were $2.89, $2.92, $3.10, and $3.42 per million Btu, respectively.

Firms were also asked how they anticipated utilizing any excess financial capital over the next 12 months, checking all options that applied. Over 60 percent of respondents reported excess financial capital would be used to expand business through capital expenditures (Chart 3). Nearly 40 percent of firms reported they would use excess financial capital to reduce debt. A quarter of firms will also prioritize paying out dividends, and more than 21 percent reported excess financial capital would be put towards wages and benefits for employees.

Chart 3.

Special Question - How does your company anticipate utilizing any excess financial capital over the next 12 months? (Please check all that apply)

Skip to data visualization table| Utilization | Percent |

|---|---|

| Capital Expenditures (expansion) | 64.28571 |

| Reduce Debt | 39.28571 |

| Payout Dividends | 25 |

| Wages and Benefits | 21.42857 |

| Other | 3.571429 |

| Buyback Shares | 0 |

Finally, firms were asked about the impact of price differentials between WTI Midland and Cushing on oil production in the Permian Basin over the next six months. Nearly 38 percent of respondents had no opinion, and almost 14 percent reported no impact (Chart 4). More than 44 percent of firms expected a slightly negative impact on oil production from the price differentials, with less than four percent of firms reporting a significantly negative impact.

Chart 4.

Special Question - Do you expect recent crude oil price differentials between WTI Midland and Cushing to have an impact on oil production growth in the Permian Basin over the next 6 months?

Skip to data visualization table| Impact | Percent |

|---|---|

| No impact | 13.7931 |

| Slightly negative | 44.82759 |

| Significantly negative | 3.448276 |

| No opinion or do not know | 37.93103 |

Table 1 - Summary of Tenth District Energy Conditions, Quarter 3, 2018

Source: Federal Reserve Bank of Kansas City

Table 2 - Historical Energy Survey Indexes

Source: Federal Reserve Bank of Kansas City

Selected Comments

“We expect high volatility in price driven by political forces. Reduced production from Iran and Venezuela is offset by U.S. growth. We expect Permian supply growth will be limited for the next couple years, and then will explode with new infrastructure.”

“Oil price expectations are driven by several factors. There is very little spare capacity worldwide. U.S. production is strong, but production increases will begin to flatten. Geopolitical risks are expected to continue and possibly increase.”

“There is a tremendous supply of natural gas in the U.S., both discovered and undiscovered. New pipelines coming out of the Permian and Anadarko Basins will help increase the received price.”

“Natural gas is plentiful in the U.S. and production companies will be able to meet any increased levels of demand.”

“We want to make capital improvements to upgrade our rigs, however the 2015 downturn is always in the back of mind. Hoarding working capital rather than major expenditures is the focus over the next 6 months.”

“Permian gas, oil, and NGL bottlenecks are having an effect on our ability to grow.”

“LNG exports are viewed positively, but as having little impact given the large amounts of natural gas deposits in the U.S.”

Additional Resources

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author