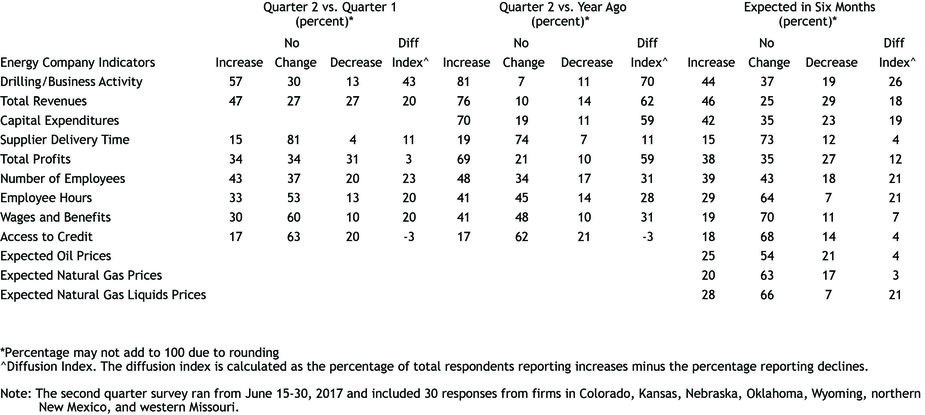

Summary of Quarterly Indicators

District energy activity expanded at a slower pace in the second quarter of 2017, as reported by firms contacted between June 15 and 30 (Tables 1 & 2). Most indexes eased but remained above zero. The total revenues and profits indexes were significantly lower, and the drilling and business activity index declined moderately (Chart 1). The employment index was modestly lower, while the access to credit index fell into negative territory for the first time since the third quarter of 2016. In contrast, the indexes for employee hours and for wages and benefits edged higher.

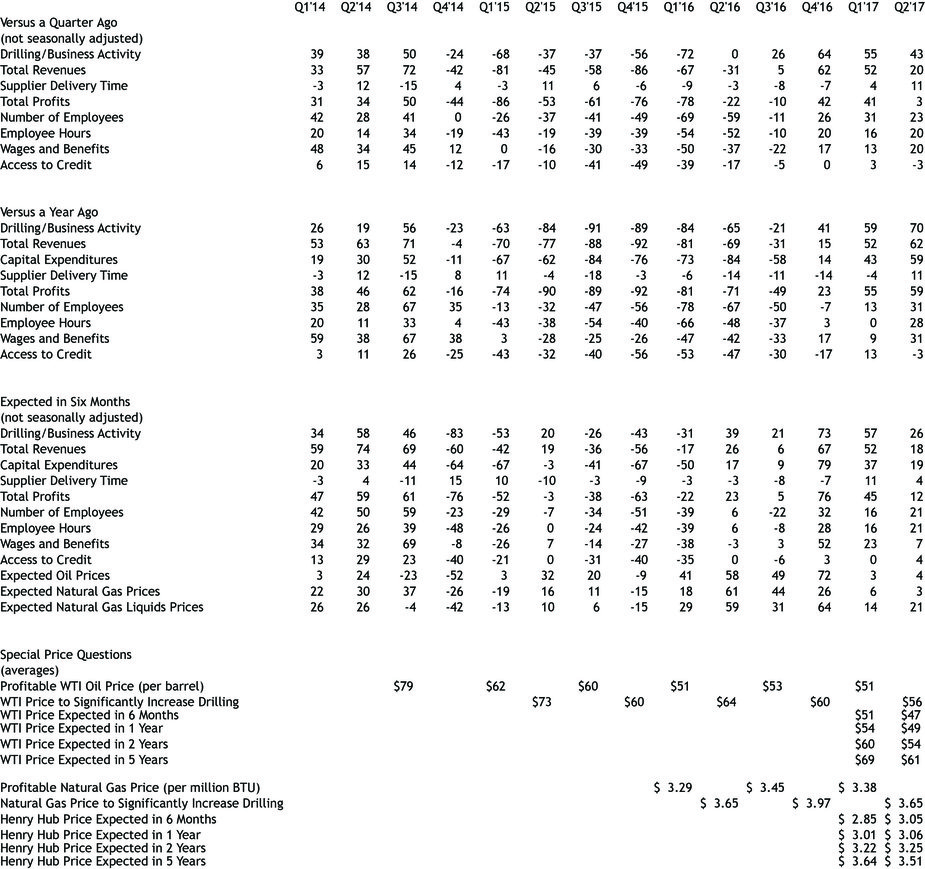

Chart 1. Drilling/Business Activity Index vs. a Quarter Ago

Skip to data visualization table| Date | Drilling/Business Activity |

|---|---|

| 2014Q1 | 39 |

| 2014Q2 | 38 |

| 2014Q3 | 50 |

| 2014Q4 | -24 |

| 2015Q1 | -68 |

| 2015Q2 | -37 |

| 2015Q3 | -37 |

| 2015Q4 | -56 |

| 2016Q1 | -72 |

| 2016Q2 | 0 |

| 2016Q3 | 26 |

| 2016Q4 | 64 |

| 2017Q1 | 55 |

| 2017Q2 | 43 |

Most year-over-year indexes increased further. The drilling and business activity and capital expenditures indexes increased to their highest readings in the survey’s history. Similarly, the employee hours and wages and benefits indexes jumped to their highest readings since 2014. The revenues and employment indexes rose somewhat, and the profits index edged higher. Furthermore, the supplier delivery time index turned positive for the first time since early 2015. However, the access to credit index fell back into negative territory.

Most future expectations indexes dropped but remained in positive territory. The future drilling and business activity index fell from 57 to 26, and the future revenues and total profits indexes also declined considerably. The future capital spending index fell moderately from 37 to 19. However, the future employment index edged higher and the access to credit index rose from 0 to four.

Price expectations for oil and gas were mixed. The expected oil prices index inched up to four, meaning most respondents expected oil prices to stay near current levels through the end of 2017. The NGL price index rose moderately, while the natural gas price index fell from six to three.

Summary of Special Questions

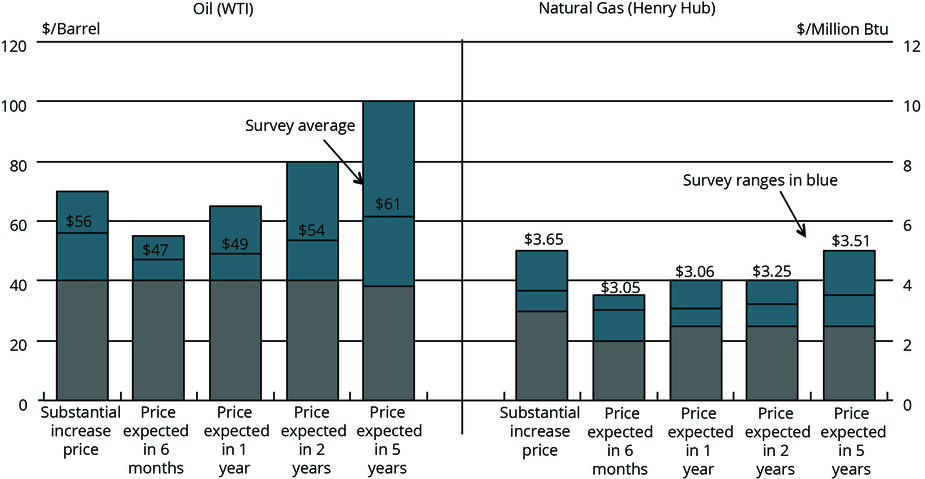

Firms were asked what oil and natural gas prices were needed for drilling to increase substantially in the areas in which they were active. The average oil price needed was $56 per barrel, with a range of $40 to $70 (Chart 2). This was modestly lower than the $60 average in the fourth quarter of 2016. The average natural gas price needed was $3.65 per million Btu, with responses ranging from $3 to $5.

Chart 2. Special Question - What price is currently needed for a substantial increase in drilling to occur for oil and natural gas, and what do you expect the WTI and Henry Hub prices to be in six months, one year, two years, and five years?

Firms were also again asked what they expected oil and natural gas prices to be in six months, one year, two years, and five years. The average expected WTI prices for these periods were $47, $49, $54, and $61 per barrel, respectively, lower than in the previous survey. The average expected Henry Hub natural gas prices for these periods were $3.05, $3.06, $3.25, and $3.51 per million Btu.

Firms were asked if they expected the U.S. rig count growth to continue at the current pace. The majority of contacts expected a slowdown in growth, citing the recent drop in oil prices as the main factor.

Firms were also asked if financing had become more or less available in recent months. Respondents said financing has tightened at banks and in bond markets, while equity markets were mixed (Chart 3). Private equity was the most readily available source of financing for most contacts.

Chart 3. Special Question - Has financing become more available or less available from the following sources in recent months?

Skip to data visualization table| Sources | Less | More |

|---|---|---|

| Banks | 59 | 41 |

| Equity Markets | 50 | 50 |

| Bond Markets | 56 | 44 |

| Private Equity | 25 | 75 |

Firms were asked what two areas of spending were cut most significantly from 2014 to 2016, and which two areas have seen the largest increases since 2016. Exploration and development capex and labor/wages/benefits were the top two areas that firms said saw the biggest cuts from 2014 to 2016 (Chart 4). Meanwhile, spending since 2016 has picked up the most in exploration and development capex followed by equipment maintenance capex and labor/wages/benefits.

Chart 4. Special Question - Where are the top two areas your firm most significantly cut spending from 2014 to 2016, and where are the top two areas your firm has increased spending since 2016?

Skip to data visualization table| Area | Decreased spending from 2014 to 2016 | Increased spending since 2016 |

|---|---|---|

| Labor Wages and Benefits | 22 | 23 |

| SG and A | 20 | 8 |

| Research and Development | 15 | 8 |

| Expl and Develop Capex | 30 | 35 |

| Equipment Maintenance | 9 | 23 |

| Other | 4 | 5 |

Finally, firms were asked for their expected average employment levels for 2017 and 2018. Overall, year-over-year employment was expected to rise modestly in both 2017 and 2018. For 2017, the strongest employment growth was expected to come from E&P companies. However, services companies were expected to post the highest growth in 2018.

Table 1 - Summary of Tenth District Energy Conditions, Quarter 2, 2017

Table 2 - Historical Energy Survey Indexes

Selected Comments

“U.S. activity will offset OPEC cuts to keep prices down over the next several months. U.S. activity will curtail to some degree before year end due to poor returns and market balance will be achieved sometime in 2018. There is too much under-exploited oil supply for prices to rise to 2013 levels for some time.”

“The rig count pace of growth is going to slow significantly and probably flat line. The industry has a significant number of drilled but uncompleted wells and this inventory is growing every day.”

“Abundant supply of both oil and gas has the market depressed. Anticipate reduction in activity if the commodity price trend continues in this direction.”

“I believe that the rig count has gone up ahead of the price of oil. I do not believe that the current price and oversupply requires the increase in rig counts that we have seen.”

“The current rise in the rig count is a harvesting operation within the shale plays. Very little exploration seems to be occurring at the moment.”

“There are huge volumes of natural gas everywhere. Every oil well being drilled has significant associated natural gas.”

“Public companies overpaid for Permian assets and must show reserve and production growth, so drilling will continue to escalate for several months in the Permian, no matter the price. Other basins may counter that a bit when prices are uneconomic.”

Additional Resources

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author