Bank account ownership provides many benefits to households, including access to safe, low-cost financial services and a safe place to store money, but many households face barriers to bank account ownership, particularly lower-income households. According to the Federal Deposit Insurance Corporation National Surveys of Unbanked and Underbanked Households (FDIC surveys), some of the most cited reasons for being unbanked are financial reasons: a lack of money to keep in an account or meet minimum balance requirements and high or unpredictable bank fees. These financial barriers suggest that improving unbanked households’ access to bank accounts that are safe (with no hidden, unexpected, or excessive fees) and low cost to use and maintain (with no monthly fees assessed based on account balances) may help boost bank account ownership.

One key effort to expand households’ access to safe, low-cost bank accounts is the Bank On initiative (FDIC 2022). The initiative comprises local coalitions of public officials, community organizations, and financial institutions in cities and states across the country that work to increase the availability of safe, low-cost accounts for households in their locales. To support the work of its local coalitions, Bank On introduced a set of national standards for safe, low-cost accounts in 2015 and began offering free certification for accounts that meet its standards. Today, over 400 financial institutions offer Bank On-certified accounts.

In this Payments System Research Briefing, I use data from the FDIC surveys and the Bank On National Data (BOND) Hub to examine whether the increase in the availability of Bank On-certified accounts has helped alleviate two financial barriers to bank account ownership and thus contributed to the recent decline in the unbanked rate in the United States. I find evidence that expanded access to Bank On-certified accounts has helped ease minimum balance requirements as barrier to bank account ownership, particularly among lower-income households, but not that it has helped address the barrier of high or unpredictable bank fees.

Bank On-certified accounts: Safer and lower-cost bank account options for unbanked households

Bank On is a nationwide initiative whose objective is to promote access to safe, low-cost bank accounts. The initiative currently comprises 99 local coalitions across the country and is led by the Cities for Financial Empowerment (CFE) fund. Most notably, the initiative established the Bank On National Account Standards in 2015._ Inspired by the FDIC’s Model Safe Accounts Template, these standards were developed to provide Bank On coalitions with a benchmark for bank accounts that could be considered safe and low-cost._ Since their introduction, local Bank On coalitions have worked to expand offerings of accounts that meet the standards. The CFE fund supports these efforts by providing free Bank On certification for accounts that comply with the standards.

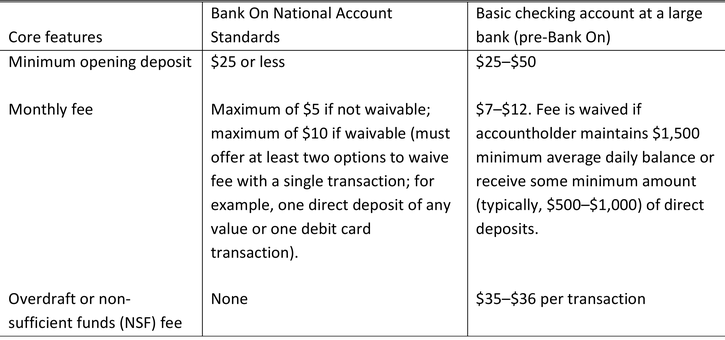

The introduction of the Bank On standards and their adoption by financial institutions—notably the largest banks—has helped expand the availability of bank accounts that are safer and less costly for many unbanked households. Table 1 outlines three core requirements of the Bank On standards that could make Bank On-certified accounts safer and less costly for unbanked households than the basic checking accounts previously offered by some of the largest banks._

Table 1. Core Features of Bank On National Account Standards

First, Bank On-certified accounts set a minimum opening deposit as high as $25, whereas basic checking accounts at the largest banks required a minimum opening deposit of $25 to $50. For unbanked households that cited lacking money to open an account, this lower minimum opening deposit may increase access to account ownership.

Second, Bank On-certified accounts charge either a non-waivable monthly fee of $5 or less or a fee of $10 or less that could be waived if the accountholder performs one qualifying transaction (of any value) each month—a relatively easy condition for most households to meet. In contrast, basic checking accounts at large banks charged monthly fees of $7 to $12, which were waivable only under conditions that most unbanked households could not easily fulfill, such as having a minimum balance over $1500 or direct deposits of at least $500 a month. Indeed, according to the 2015 Survey of Household Economics and Decisionmaking, the majority of unbanked households (88 percent) did not have $400 in cash to pay for an emergency expense. The lower monthly fees of Bank On-certified accounts may therefore help address both the lack of money and the high fees that have prevented unbanked households from opening accounts.

Third, Bank On-certified accounts do not charge overdraft or non-sufficient fund (NSF) fees, whereas large banks charged overdraft and NSF fees of $35 or $36 per transaction on basic checking accounts. Many consumers consider overdraft and NSF fees to be high and unpredictable (Consumer Financial Protection Bureau 2023, 2017). The absence of these fees may make Bank On accounts safer and less costly for unbanked households and help alleviate high or unpredictable fees as a barrier to bank account ownership.

Has greater access to Bank On-certified accounts eased financial barriers to bank account ownership?

The number of Bank On-certified accounts has grown substantially since the introduction of the Bank On National Account Standards in 2015. According to the American Bankers’ Association (ABA), the number of financial institutions offering Bank On-certified accounts grew from two in 2015 to 403 in 2023. All the large banks examined for Table 1 now offer Bank On-certified accounts, with minimum opening deposits of $25 or less and monthly fees of around $5. As of 2023, households can open a Bank On-certified account at more than 45,200 branches, and 97.4 percent of low-to-moderate income (LMI) households—who are disproportionately more likely to be unbanked—are located near a branch offering Bank On accounts (ABA 2024)._

Over this same period, the unbanked rate among U.S. households has declined considerably, from 7.0 percent in 2015 to 4.2 percent in 2023. The unbanked rate has declined especially among households in the lowest two income groups: from 25.6 percent in 2015 to 21.8 percent in 2023 for those with income below $15,000 and from 11.8 percent to 9.0 percent for those with income between $15,000 and $30,000. This finding suggests that the increase in availability of Bank On-certified accounts may have contributed to the decline in unbanked rate, particularly among lower-income households.

To investigate whether and how the increased availability of Bank On-certified accounts may have contributed to the decline in the unbanked rate, I use data from the FDIC surveys to examine the changes in the share of unbanked households that cited each of the following reasons for being unbanked over the 2015–23 period: (i) the lack of money to keep in a bank account or meet minimum balance requirements (henceforth, “lack of money”) and (ii) high or unpredictable fees. In theory, access to Bank On-certified accounts could help address these barriers to bank account ownership. Therefore, declines in the shares of unbanked households that cited each of these reasons could indicate that expanding access to Bank On-certified accounts helped reduce the unbanked rate.

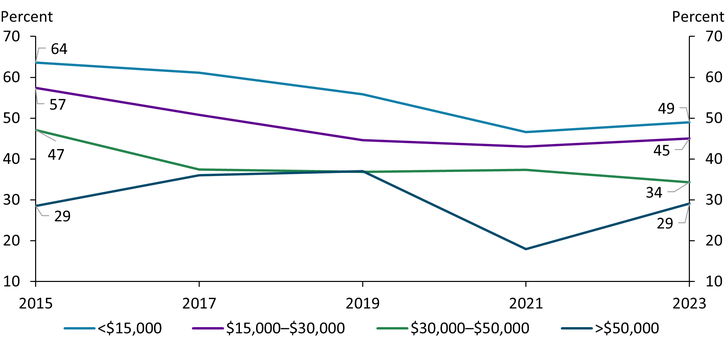

The overall share of unbanked households that cited a lack of money as a reason for being unbanked fell from 57.4 percent in 2015 to 42.3 percent in 2023. Chart 1 shows that the share of unbanked households that cited this reason fell between 2015 and 2023 across all but the highest income group, and the decline was larger for the lowest income group. For unbanked households with income below $15,000 (light blue line), the share declined by 15 percentage points (from 64 percent to 49 percent), while for households with income between $15,000 and $30,000 (purple line) and between $30,000 and $50,000 (green line), the share declined by 13 percentage points. These declines suggest that this barrier to bank account ownership has eased among lower-income households. Moreover, because a lack of money is more likely to pose a barrier to bank account ownership for unbanked households in the lowest two income groups, Bank On standards addressing this barrier may help explain why the unbanked rate in these two income groups fell more than those of the higher two income groups.

Chart 1. Share of unbanked households citing lack of money as a reason for being unbanked fell from 2015 to 2023 in the lower three income groups

Sources: FDIC and author’s calculations.

Data from Bank On-certified accounts (specifically, the BOND Hub) also suggest that access to these accounts has helped ease the barrier to bank account ownership posed by a lack of money. In 2023, the average monthly balance of Bank On-certified accounts was $1,213, and less than 40 percent of the accounts received direct deposits each month. If these account holders had held a basic checking account at a large bank (before Bank On-certified accounts were available), many would likely not have met the minimum balance or direct deposit requirements for waiving monthly fees and would have thus incurred a monthly fee of $7 to $12, potentially inhibiting them from owning a bank account. In contrast, most owners of Bank On-certified accounts incurred a monthly fee of $5 or less._

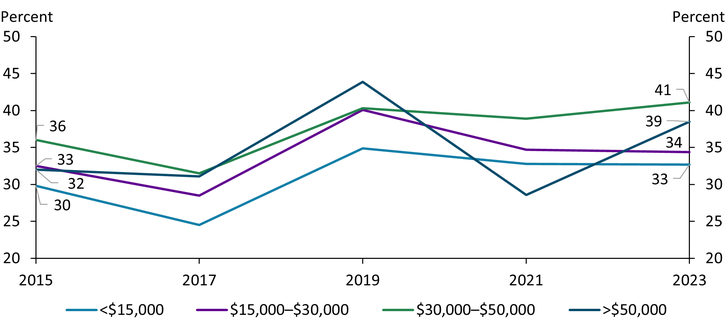

On the other hand, the share of unbanked households citing high or unpredictable fees as a reason for being unbanked did not decline with the rise in Bank On-certified accounts and in fact increased from 30.8 percent in 2015 to 35.5 percent in 2023. Chart 2 shows that the share of unbanked households citing this reason increased across all four income groups of unbanked households; the increase was particularly large among unbanked households in the two highest income groups. For unbanked households with income between $30,000 and $50,000 (green line), the share increased from 36 percent to 41 percent, and for those with income of $50,000 or more (dark blue line), the share increased from 32 percent to 39 percent. Given that the Bank On standards prohibit Bank On-certified accounts from charging most fees—notably overdraft and NSF fees, which are arguably the main sources of high and unpredictable fees for most bank accountholders—this finding could indicate that a lack awareness of Bank On-certified accounts or their features among unbanked households, particularly higher-income unbanked households.

Chart 2. Share of unbanked households citing high or unpredictable fees as a reason for being unbanked rose from 2015 to 2023, especially in the two higher income groups

Sources: FDIC and author’s calculations.

Apart from a lack of awareness of Bank On-certified accounts, some unbanked households may consider the few fees associated with owning Bank On-certified accounts to be high or unpredictable. Although the main fee associated with owning most Bank On-certified accounts is a fixed monthly fee of $5 or less, some accountholders may also incur a fee of up to $2 for requesting paper statements and fees charged by their banks and the ATM owners when using out-of-network ATMs. The Bank On standards limit the out-of-network ATM fee that Bank On-certified accounts can charge to no more than $2.50 per transaction in most cases but have no influence over how much ATM owners charge. The fee imposed by out-of-network ATM owners varies from owner to owner and the average fee charged by out-of-network ATM owners in 2024 was $3.19 per transaction (Bennett and Goldberg 2024). Avoiding these fees could be difficult for previously unbanked households, as a relatively large share of unbanked households lack the technologies (such as smartphone or home internet access) needed to receive electronic statements._ Unbanked households also tend to be more cash reliant and may continue to use cash heavily even after they become banked, which may result in frequent use of out-of-network ATMs (Greene and Shy 2020). Thus, even in the absence of most bank fees, the cost of owning Bank On-certified accounts could still be high or unpredictable for some unbanked households.

Conclusion

The Bank On initiative has helped to expand the availability of safe, low-cost bank accounts over the past decade. The increased availability of these accounts appears to have contributed to the decline in unbanked rate by alleviating the high fees for accounts that do not meet minimum balance requirements. Even so, over 40 percent of unbanked households continued to cite lack of money as a reason for being unbanked in 2023. Further, increased access to Bank On-certified accounts does not seem to have helped address high or unpredictable fees as a barrier to bank account ownership, despite these accounts only charging a few fees that are relatively low or avoidable.

One possible explanation for these results is that unbanked households may lack awareness of Bank On-certified accounts. Another is that poverty poses further challenges to bank account ownership for some unbanked households, even when they can access Bank On-certified accounts. A third explanation may be unbanked households’ heavy reliance on cash for transactions and the high cost of using out-of-network ATMs. More research is needed to identify further ways to promote bank account ownership among unbanked households.

Endnotes

-

1 The Bank On National Account Standards (2025–26) are available on External LinkBank On’s website.

-

2 The FDIC Model Safe Accounts Template is available on the External LinkFDIC’s website.

-

3 The basic checking accounts included in this comparison are Bank of America Core Checking, Chase Total Checking, Wells Fargo Everyday Checking, U.S. Bank Easy Checking, and PNC Bank Standard Checking.

-

4 The ABA defines proximity to a Bank On branch at a census tract level. Households living in a census tract are located near a Bank On branch if a Bank On branch is within a two-mile radius of the geographical center of the census tract for urban census tracts and a 10-mile radius for rural or mixed census tracts.

-

5 According to Bank On, only nine out of the 486 Bank On-certified accounts currently charge a monthly fee greater than $5.

-

6 About 28 percent of unbanked households lacked a smartphone in 2023, compared with 11 percent of banked households (FDIC 2024). Although more recent data on households’ access to home internet access by their banking status are not available, about 66 percent of unbanked households lacked home internet access in 2019, compared with 27 percent of banked households (FDIC 2020).

References

American Bankers Association (ABA). 2024. “External LinkABA Bank On Dashboard.” March 25.

Bennett, Karen, and Matthew Goldberg. 2024. “External LinkSurvey: ATM Fees Reach 26-Year High While Overdraft Fees Inch Back Up.” Bankrate, August 21.

Consumer Financial Protection Bureau (CFPB). 2023. “External LinkOverdraft and Nonsufficient Fund Fee: Insights from the Making Ends Meet Survey and Consumer Credit Panel.” CFPB Office of Research Publication no. 2023-9, December.

———. 2017. “External LinkConsumer Voices on Overdraft Programs.” November.

Federal Deposit Insurance Corporation (FDIC). 2024. “External Link2023 FDIC National Survey of Unbanked and Underbanked Households.” November.

———. 2022. “External Link2021 FDIC National Survey of Unbanked and Underbanked Households.” October.

———. 2020. “External LinkHow America Banks: Household Use of Banking and Financial Services, 2019 FDIC Survey.” October.

Greene, Claire, and Oz Shy. 2020. “External LinkResearch on Paying with Cash and Checks.” Federal Reserve Bank of Atlanta, March.

Ying Lei Toh is a senior economist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author